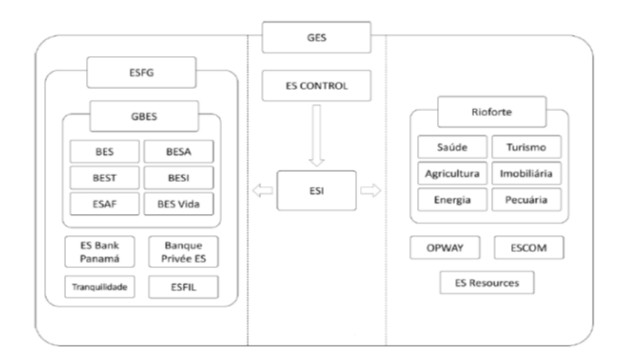

We examined the external ability of the loan loss provision (LLP) model to detect extreme cases of earnings management (EM). According to the literature, the LLP model is the most useful in examining EM in banking institutions. We used it herein to explore the time-series behaviour of a fraudulent business group in the Portuguese banking sector between 1992 and 2013 − the Banco Espírito Santo Group (GBES). We conclude that GBES did not make discretionary use of LLP (i.e., DLLP) in the fraud period (2008 to 2013) when compared with the pre-fraud years (1992 to 2007). However, the level of LLP was significantly higher in the latter period; this was consistent with the procyclical nature of GBES's LLP. The results of a difference-in-difference approach did not reveal any significant differences between GBES's DLLP and non-fraudulent banks in the fraud period. Interestingly, the full bank sample (including GBES) provided evidence of the procyclical nature of LLP. Additional tests did not support the hypothesis of income smoothing via LLP, either amongst the bank sample as a whole or by GBES. The proven facts of the fraud indicated a significant undervaluation of loans and financial instruments and an underestimation of LLP. Thus, we expected to find negative DLLP in the fraud period and significantly different DLLP between the pre-fraud period and the fraud period itself. The DLLP of GBES should also have been significantly different from non-fraudulent banks in the fraud period. The LLP model proved ineffective in detecting GBES fraud and assessing the decisions of the bank's leader and his team, while the use of DLLP was effective. The evidence collected in our study will be of benefit to scholars and banking regulators.

Citation: Tânia Menezes Montenegro, Filomena Antunes Brás. Scandal in the Portuguese banking sector – how a banking specific earnings management model predicted the fall of a family business group[J]. Green Finance, 2022, 4(3): 364-386. doi: 10.3934/GF.2022018

We examined the external ability of the loan loss provision (LLP) model to detect extreme cases of earnings management (EM). According to the literature, the LLP model is the most useful in examining EM in banking institutions. We used it herein to explore the time-series behaviour of a fraudulent business group in the Portuguese banking sector between 1992 and 2013 − the Banco Espírito Santo Group (GBES). We conclude that GBES did not make discretionary use of LLP (i.e., DLLP) in the fraud period (2008 to 2013) when compared with the pre-fraud years (1992 to 2007). However, the level of LLP was significantly higher in the latter period; this was consistent with the procyclical nature of GBES's LLP. The results of a difference-in-difference approach did not reveal any significant differences between GBES's DLLP and non-fraudulent banks in the fraud period. Interestingly, the full bank sample (including GBES) provided evidence of the procyclical nature of LLP. Additional tests did not support the hypothesis of income smoothing via LLP, either amongst the bank sample as a whole or by GBES. The proven facts of the fraud indicated a significant undervaluation of loans and financial instruments and an underestimation of LLP. Thus, we expected to find negative DLLP in the fraud period and significantly different DLLP between the pre-fraud period and the fraud period itself. The DLLP of GBES should also have been significantly different from non-fraudulent banks in the fraud period. The LLP model proved ineffective in detecting GBES fraud and assessing the decisions of the bank's leader and his team, while the use of DLLP was effective. The evidence collected in our study will be of benefit to scholars and banking regulators.

| [1] |

Ab-Hamid MF, Asid R, Sulaiman NF, et al. (2018) The effect of earnings management on bank efficiency. Asian J Account Gov 10: 73–82. https:/doi.org/10.17576/AJAG-2018-10-07 doi: 10.17576/AJAG-2018-10-07

|

| [2] |

Ahmed AS, Takeda C, Thomas S (1999) Bank loan loss provisions: A reexamination of capital management, earnings management and signalling effects. J Account Econ 28: 1–25. https://doi.org/10.1016/S0165-4101(99)00017-8 doi: 10.1016/S0165-4101(99)00017-8

|

| [3] |

Alali F, Jaggi B (2011) Earnings versus capital ratios management: Role of bank types and SFAS 114. Rev Quant Financ Account 36: 105–132. https://doi.org/10.1007/s11156-010-0173-4 doi: 10.1007/s11156-010-0173-4

|

| [4] | Amaral L (2015) Em Nome do Pai e do Filho… O Grupo Espírito Santo, da privatização à queda, Lisboa: Edições D. Quixote. |

| [5] |

Anandarajan A, Hasan I, Lozano-Vivas A (2003) The role of loan loss provisions in earnings management, capital management, and signaling: the Spanish experience. Adv Int Account 16: 45–66. https://doi.org/10.1016/S0897-3660(03)16003-5 doi: 10.1016/S0897-3660(03)16003-5

|

| [6] |

Anandarajan A, Hasan I, McCarthy C (2007) Use of loan loss provisions for capital, earnings management and signalling by Australian banks. Account Financ 47: 357–379. https://doi.org/10.1111/j.1467-629X.2007.00220.x. doi: 10.1111/j.1467-629X.2007.00220.x

|

| [7] |

Andries K, Gallemore J, Jacob M (2017) The effect of corporate taxation on bank transparency: Evidence from loan loss provisions. J Account Econ 63: 307–328. https://doi.org/10.1016/j.jacceco.2017.03.004 doi: 10.1016/j.jacceco.2017.03.004

|

| [8] | Antunes JE (2018) Banco Espírito Santo - The Anatomy of a Banking Scandal in Portugal. In G. DB Ferrarini & GG Van Solingue (Eds.). Corporate Governance of Financ Inst 2–4. Oxford University Press. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3225343 |

| [9] |

Beatty AL, Chamberlain SL, Magliolo J (1995) Managing financial reports of commercial banks: the influence of taxes, regulatory capital, and earnings. J Account Res 333: 231–262. https://doi.org/10.2307/2491487 doi: 10.2307/2491487

|

| [10] |

Beatty AL, Ke B, Petroni KR (2002) Earnings management to avoid earnings declines across publicly and privately held banks. Account Rev 77: 547–570. Https://doi.org/10.2308/accr.2002.77.3.547 doi: 10.2308/accr.2002.77.3.547

|

| [11] | BES Parliamentary Commission Report (2015) Available from: https://www.parlamento.pt/sites/COM/XⅡLEG//CPIBES/Paginas/RelatoriosActividade.aspx |

| [12] |

Bouvatier V, Lepetit L, Strobel F (2014) Bank income smoothing, ownership concentration and the regulatory environment. J Bank Financ 41: 253–270. Https://doi.org/10.1016/j.jbankfin.2013.12.001 doi: 10.1016/j.jbankfin.2013.12.001

|

| [13] |

Bryce C, Dadoukis A, Hall M, et al. (2015) An analysis of loan loss provisioning behaviour in Vietnamese banking. Financ Res Lett 14: 69–75. Https://doi.org/10.1016/j.frl.2015.05.014 doi: 10.1016/j.frl.2015.05.014

|

| [14] | Cavaleiro D, Vicente I (2022) Mais recente condenação de Ricardo Salgado prescreve em novembro. Express, Available from: https://expresso.pt/economia/2022-04-22-Mais-recente-condenacao-de-Ricardo-Salgado-prescreve-em-novembro-b6948959 |

| [15] |

Chaity NS, Islam KMZ (2022) Bank efficiency and practice of earnings management: a study on listed commercial banks of Bangladesh. Asian J Account Res 7: 114–128. Https://doi.org/10.1108/AJAR-09-2020-0080 doi: 10.1108/AJAR-09-2020-0080

|

| [16] |

Chang RD, Shen WH, Fang CJ (2008) Discretionary loan loss provision and earnings management for the banking industry. Int Bus Econ Res J 7: 9–20. Https://doi.org/10.19030/iber.v7i3.3230 doi: 10.19030/iber.v7i3.3230

|

| [17] |

Cohen LJ, Cornett MM, Marcus AJ, et al. (2014) Bank Earnings Management and Tail Risk during the Financial Crisis. J Money Credit Bank 46: 171–197. Https://doi.org/10.1111/jmcb.12101 doi: 10.1111/jmcb.12101

|

| [18] |

Cornett MM, Marcus AJ, Saunders A, et al. (2009) Corporate governance and earnings management at large US bank holding companies. J Corp Financ 15: 412–430. Https://doi.org/10.1016/j.jcorpfin.2009.04.003 doi: 10.1016/j.jcorpfin.2009.04.003

|

| [19] |

Curcio D, Hasan I (2015) Earnings and capital management and signaling: The use of loan-loss provisions by European banks. Eur J Financ 21: 26–50. Https://doi.org/10.1080/1351847X.2012.762408 doi: 10.1080/1351847X.2012.762408

|

| [20] |

Curcio E, Simone AD, Gallo A (2016) Financial crisis and international supervision: new evidence on the discretionary use of loan loss provisions at Euro Area commercial banks. British Account Rev 49: 181–193. Https://doi.org/10.1016/j.bar.2016.09.001 doi: 10.1016/j.bar.2016.09.001

|

| [21] |

Dahl D (2013) Bank audit practices and loan loss provisioning. J Bank Financ 37: 3577–3584. Https://doi.org/10.1016/j.jbankfin.2013.05.007 doi: 10.1016/j.jbankfin.2013.05.007

|

| [22] |

Dechow PM, Dichev ID (2002) The Quality of Accruals and Earnings: The Role of Accrual Estimation Errors. Account Rev 77: 35–59. Https://doi.org/10.2308/accr.2002.77.s-1.35 doi: 10.2308/accr.2002.77.s-1.35

|

| [23] |

Dechow PM, Ge W, Schrand C (2010) Understanding Earnings Quality: A Review of the Proxies, their Determinants and their Consequences. J Account Econ 50: 344–401. Https://doi.org/10.1016/j.jacceco.2010.09.001 doi: 10.1016/j.jacceco.2010.09.001

|

| [24] | Dechow PM, Sloan RG, Sweeney AP (1995) Detecting Earnings Management. Account Rev 70: 193–225. |

| [25] |

DeFond ML (2010) Earnings quality research: Advances, challenges and future research. Account Econ 50: 402–409. Https://doi.org/10.1016/j.jacceco.2010.10.004. doi: 10.1016/j.jacceco.2010.10.004

|

| [26] |

El SH (2012) Loan loss provisioning and income smoothing in US banks pre and post the financial crisis. Int Rev Financ Anal 25: 64–72. Https://doi.org/10.1016/j.irfa.2012.06.007 doi: 10.1016/j.irfa.2012.06.007

|

| [27] | Ferreira A (2016) BES: Os dias do fim revelados, 2 Eds., Lisboa: CHIADO Editora. |

| [28] |

Fonseca AR, Gonzalez F (2008) Cross-country determinants of bank income smoothing by managing loan-loss provisions. J Bank Financ 32: 217–228. Https://doi.org/10.1016/j.jbankfin.2007.02.012 doi: 10.1016/j.jbankfin.2007.02.012

|

| [29] | Guerreiro PS (2018) A batalha de Titãs: como Pedro Queiroz Pereira destruiu Ricardo Salgado. Express. Available from: https://expresso.pt/economia/2018-08-21-A-batalha-de-Titas-como-Pedro-Queiroz-Pereira-destruiu-Ricardo-Salgado |

| [30] |

Hamadi M, Heinen A, Linder S, et al. (2016) Does Basel Ⅱ affect the market valuation of discretionary loan loss provisions? J Bank Financ 70: 177–192. Https://doi.org/10.1016/j.jbankfin.2016.06.002 doi: 10.1016/j.jbankfin.2016.06.002

|

| [31] |

Jackson AB (2018) Discretionary Accruals: Earnings Management... or Not? Abacus 54: 136–153. Https://doi.org/10.1111/abac.12117 doi: 10.1111/abac.12117

|

| [32] |

Jones J (1991) Earnings management during import relief investigations. J Account Res 29: 193–228. Https://doi.org/10.2307/2491047 doi: 10.2307/2491047

|

| [33] |

Kanagaretnam K, Lim CY, Lobo GJ (2014) Effects of International Institutional Factors on Earnings Quality of Banks. J Bank Financ 39: 87–106. Https://doi.org/10.1016/j.jbankfin.2013.11.005. doi: 10.1016/j.jbankfin.2013.11.005

|

| [34] |

Kanagaretnam K, Lobo GJ, Mathieu R (2003) Managerial incentives for income smoothing through bank loan loss provisions. Rev Quant Financ Account 20: 63–80. Https://doi.org/10.1023/A:1022187622780 doi: 10.1023/A:1022187622780

|

| [35] |

Kanagaretnam K, Lobo GJ, Yang DH (2004) Joint tests of signaling and incomes smoothing through bank loan loss provisions. Contemp Account Res 21: 843–884. Https://doi.org/10.1506/UDWQ-R7B1-A684-9ECR doi: 10.1506/UDWQ-R7B1-A684-9ECR

|

| [36] |

Kanagaretnam K, Lobo GJ, Yang DH (2005) Determinants of signalling by banks through loan loss provisions. J Bus Res 58: 312–320. Https://doi.org/10.1016/j.jbusres.2003.06.002 doi: 10.1016/j.jbusres.2003.06.002

|

| [37] |

Kanagaretnam K, Lim CY, Lobo GJ (2010) Auditor reputation and earnings management: International evidence from the banking industry. J Bank Financ 34: 2318–2327. Https://doi.org/10.1016/j.jbankfin.2010.02.020 doi: 10.1016/j.jbankfin.2010.02.020

|

| [38] |

Kilic E, Lobo GJ, Ranasinghe T, et al. (2012) The impact of SFAS 133 on income smoothing by banks through loan loss provisions. Account Rev 88: 233–260. Https://doi.org/10.2308/accr-50264 doi: 10.2308/accr-50264

|

| [39] |

Kothari SP, Leone AJ, Wasley CE (2005) Performance matched discretionary accrual measures. J Account Econ 39: 163–197. Https://doi.org/10.1016/j.jacceco.2004.11.002 doi: 10.1016/j.jacceco.2004.11.002

|

| [40] |

Leventis S, Dimitropoulos P, Anandarajan A (2011) Loan loss provisions, earnings management and capital management under IFRS: the case of EU commercial banks. J Financ Serv Res 40: 103–122. Https://doi.org/10.1007/s10693-010-0096-1 doi: 10.1007/s10693-010-0096-1

|

| [41] | Lima AP (2000) Is blood thicker than economic interest in familial enterprises? In: Schweitzer P.P. Author, Dividends of Kinship: Meanings and Uses of Social Relatedness, London: Routledge, 151–176. |

| [42] |

Lobo GJ, Yang DH (2001) Bank managers' heterogeneous decisions on discretionary loan loss provisions. Rev Quant Financ Account 16: 223–250. Https://doi.org/10.1023/A:1011284303517 doi: 10.1023/A:1011284303517

|

| [43] |

Marton J, Runesson E (2017) The predictive ability of loan loss provisions in banks e Effects of accounting standards, enforcement and incentives. British Account Rev 49: 162–180. Https://doi.org/10.1016/j.bar.2016.09.003 doi: 10.1016/j.bar.2016.09.003

|

| [44] |

McNichols M, Wilson GP (1988) Evidence of earnings management from the provision for bad debts. J Account Res 26: 1–31. Https://doi.org/10.2307/2491176 doi: 10.2307/2491176

|

| [45] |

Olszak M, Pipien´ M, Kowalska I, et al. (2017) What drives heterogeneity of cyclicality of loan loss provisions in the EU? J Financ Serv Res 51: 55–96. Https://doi.org/10.1007/S10693-015-0238-6 doi: 10.1007/S10693-015-0238-6

|

| [46] |

Owens E, Wu JS, Zimmerman J (2017) Idiosyncratic Shocks to Firm Underlying Economics and Abnormal Accruals. Account Rev 92: 183–219. Https://doi.org/10.2308/accr-51523 doi: 10.2308/accr-51523

|

| [47] |

Ozili PK (2015) Loan loss provisioning, income smoothing, signalling, capital management and procyclicality: Does IFRS matter? Empirical evidence from Nigeria. Mediterr J Soc Sci 6: 224–232. Https://doi.org/10.5901/mjss.2015.v6n2p224 doi: 10.5901/mjss.2015.v6n2p224

|

| [48] |

Ozili PK (2017a) Bank earnings smoothing, audit quality and procyclicality in Africa. The case of loan loss provisions. Rev Account Financ 16: 142–161. Https://doi.org/10.1108/RAF-12-2015-0188 doi: 10.1108/RAF-12-2015-0188

|

| [49] |

Ozili PK (2017b) Discretionary provisioning practices among Western European banks. J Financ Econ Policy 9: 109–118. Https://doi.org/10.1108/JFEP-07-2016-0049 doi: 10.1108/JFEP-07-2016-0049

|

| [50] |

Ozili PK, Outa E (2017) Bank loan loss provisions research: A review. Borsa Istanbul Rev 17: 144–163. Https://doi.org/10.1016/j.bir.2017.05.001 doi: 10.1016/j.bir.2017.05.001

|

| [51] |

Perez D, Salas-Fumas V, Saurina J (2008) Earnings and capital management in alternative loan loss provision regulatory regimes. Eur Account Rev 17: 423–445. Https://doi.org/10.1080/09638180802016742 doi: 10.1080/09638180802016742

|

| [52] | Santos BS (1984) A Crise e a Reconstituição do Estado em Portugal (1974–1984). Revista Crítica de Ciências Sociais 14: 9–29. |

| [53] |

Silva AF, Amaral L, Neves P (2016) Business groups in Portugal in the Estado Novo period (1930–1974): family, power and structural change. Bus Hist 58: 49–68. Https://doi.org/10.1080/00076791.2015.1044520 doi: 10.1080/00076791.2015.1044520

|

| [54] |

Skała D (2015) Saving on a rainy day? Income smoothing and procyclicality of loan loss provisions in Central European Banks. Int Financ 18: 25–46. Https://doi.org/10.1111/1468-2362.12058 doi: 10.1111/1468-2362.12058

|

| [55] | Wahlen JM (1994) The nature of information in commercial bank loan loss disclosures. Account Rev 69: 455–478. |

Figures(5) / Tables(6)

Tânia Menezes Montenegro, Filomena Antunes Brás. Scandal in the Portuguese banking sector – how a banking specific earnings management model predicted the fall of a family business group[J]. Green Finance, 2022, 4(3): 364-386. doi: 10.3934/GF.2022018

DownLoad:

DownLoad: