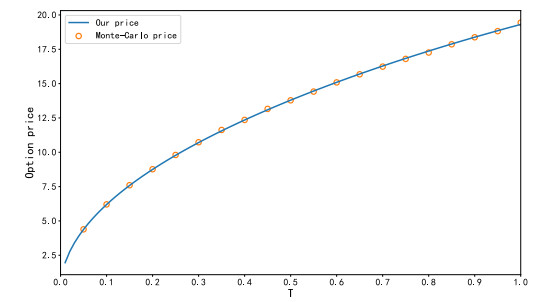

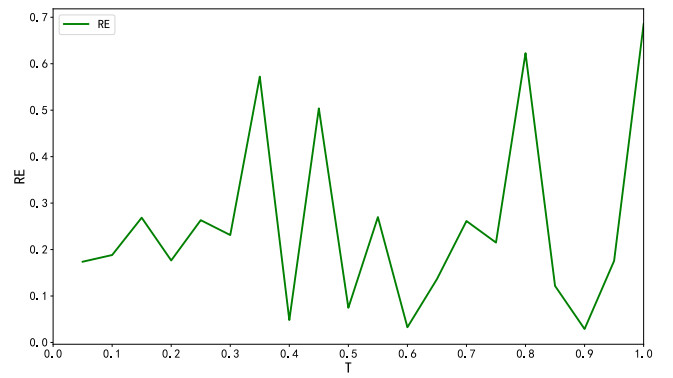

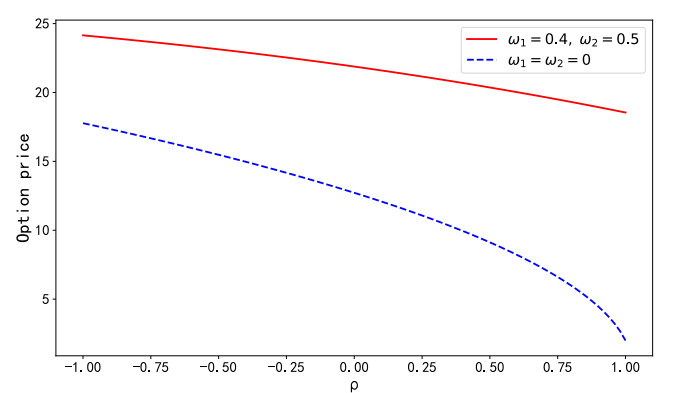

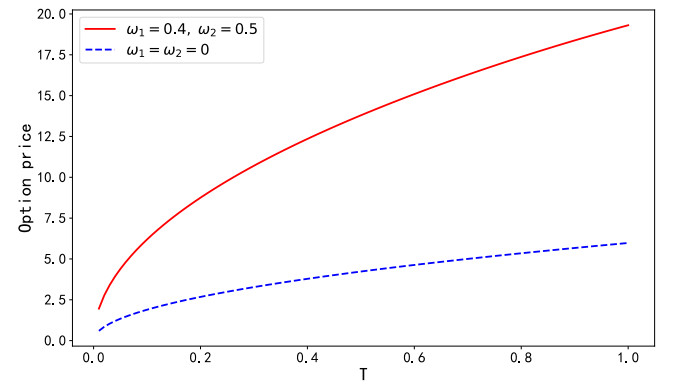

Traditional option pricing models mostly assume that the market is frictionless, ignoring the impact of liquidity on option price. In response, this paper considers a digital power generalized exchange option pricing problem when the underlying asset has liquidity risk. We obtained a closed-form digital power option pricing formula in a incomplete market by measure transformation. Finally, numerical experiments were conducted by comparing the prices computed by the new formula with those from Monte-Carlo simulations, thereby validating the accuracy of the new formula. Building on this, the impact of liquidity on option prices was further investigated.

Citation: Kaihang Zhang, Liting Gao. Digital power generalized exchange option pricing considering liquidity risk[J]. AIMS Mathematics, 2026, 11(1): 1761-1776. doi: 10.3934/math.2026073

Traditional option pricing models mostly assume that the market is frictionless, ignoring the impact of liquidity on option price. In response, this paper considers a digital power generalized exchange option pricing problem when the underlying asset has liquidity risk. We obtained a closed-form digital power option pricing formula in a incomplete market by measure transformation. Finally, numerical experiments were conducted by comparing the prices computed by the new formula with those from Monte-Carlo simulations, thereby validating the accuracy of the new formula. Building on this, the impact of liquidity on option prices was further investigated.

| [1] |

F. Black, M. Scholes, The pricing of option and corporate liabilities, J. Polit. Econ., 81 (1976), 637–654. http://doi.org/10.1086/260062 doi: 10.1086/260062

|

| [2] |

R. C. Merton, Option pricing when underlying stock returns are discontinuous, J. Financ. Econ., 3 (1976), 125–144. https://doi.org/10.1016/0304-405X(77)90016-2 doi: 10.1016/0304-405X(77)90016-2

|

| [3] |

O. Vasicek, An equilibrium characterization of the term structure, J. Financ. Econ., 5 (1977), 177–188. https://doi.org/10.1016/0304-405X(77)90016-2 doi: 10.1016/0304-405X(77)90016-2

|

| [4] |

Y. Amihud, H. Mendelson, Asset pricing and the bid-ask spread, J. Financ. Econ., 17 (1986), 223–249. https://doi.org/10.1016/0304-405X(86)90065-6 doi: 10.1016/0304-405X(86)90065-6

|

| [5] |

Y. Amihud, H. Mendelson, The effect of beta, bad-ask spread, residual risk, and size on stock returns, J. Financ. Econ., 44 (1989), 479–486. https://doi.org/10.1111/j.1540-6261.1989.tb05067.x doi: 10.1111/j.1540-6261.1989.tb05067.x

|

| [6] |

Z. Li, W. G. Zhang, Y. J. Liu, European quanto option pricing in presence of liquidity risk, N. Am. J. Econ. Financ., 45 (2018), 230–244. https://doi.org/10.1016/j.najef.2018.03.002 doi: 10.1016/j.najef.2018.03.002

|

| [7] |

Z. Li, W. G. Zhang, Y. J. Liu, Analytical valuation for geometric Asian options in illiquid markets, Physica A, 507 (2018), 175–191. https://doi.org/10.1016/j.physa.2018.05.069 doi: 10.1016/j.physa.2018.05.069

|

| [8] |

Z. Li, W. G. Zhang, Y. J. Liu, Pricing discrete barrier options under jump-diffusion model with liquidity risk, Int. Rev. Econ. Financ., 59 (2019), 347–368. https://doi.org/10.1016/j.iref.2018.10.002 doi: 10.1016/j.iref.2018.10.002

|

| [9] |

X. J. He, S. Lin, Analytically pricing exchange options with stochastic liquidity and regime switching, J. Futures Markets, 43 (2023), 662–676. https://doi.org/10.1002/fut.22403 doi: 10.1002/fut.22403

|

| [10] |

X. J. He, W. T. Wei, S. Lin, A closed-form formula for pricing exchange options with regime switching stochastic volatility and stochastic liquidity, Int. Rev. Financ. Anal., 103 (2025), 104159. https://10.1016/j.irfa.2025.104159 doi: 10.1016/j.irfa.2025.104159

|

| [11] |

X. J. He, S. D. Huang, S. Lin, A closed-form solution for pricing European-style options under the Heston model with credit and liquidity risks, Commun. Nonlinear. Sci., 143 (2025), 108595. https://10.1016/j.cnsns.2025.108595 doi: 10.1016/j.cnsns.2025.108595

|

| [12] |

P. Mittal, D. Selvamuthu, Vulnerable power exchange options with liquidity risk, Physica A, 672 (2025), 130646. https://10.1016/j.physa.2025.130646 doi: 10.1016/j.physa.2025.130646

|

| [13] |

X. J. He, S. Lin, A stochastic liquidity risk model with stochastic volatility and its applications to option pricing, Stoch. Models, 43 (2024), 273–292. https://doi.org/10.1080/15326349.2024.2332326 doi: 10.1080/15326349.2024.2332326

|

| [14] |

X. J. He, H. Chen, S. Lin, A closed-form formula for pricing European options with stochastic volatility, regime switching, and stochastic market liquidity, J. Futures Markets, 45 (2025), 429–440. https://doi.org/10.1002/fut.22573 doi: 10.1002/fut.22573

|

| [15] |

H. U. Gerber, E. W. Shiu, Option pricing by Esscher transforms, T. Soc. Actuaries, 46 (1994), 99–191. https://doi.org/10.3969/j.issn.1005-3085.2021.02.009 doi: 10.3969/j.issn.1005-3085.2021.02.009

|

| [16] |

S. P. Feng, M. W. Hung, Y. H. Wang, The importance of stock liquidity on option pricing, Int. Rev. Econ. Financ., 43 (2016), 457–467. https://doi.org/10.1016/j.iref.2016.01.008 doi: 10.1016/j.iref.2016.01.008

|

| [17] |

R. Gao, Y. Q. Li, L. S. Lin, Bayesian statistical inference for European options with stock liquidity, Physica A, 518 (2019), 312–322. https://10.1016/j.physa.2018.12.008 doi: 10.1016/j.physa.2018.12.008

|

| [18] |

R. Gao, Y. Q. Li, Y. F. Bai, Pricing quanto options with market liquidity risk, Commun. Stat.-Theor. M., 51 (2022), 3312–3333. https://10.1080/03610926.2020.1793364 doi: 10.1080/03610926.2020.1793364

|

| [19] |

R. Gao, Y. F. Bai, Pricing quanto options with market liquidity risk, PLoS One, 18 (2023), e0292324. https://10.1371/journal.pone.0292324 doi: 10.1371/journal.pone.0292324

|

| [20] |

W. H. Li, W. Zhong, G. W. Lv, Digital power exchange option pricing under jump-diffusion model, Chinese J. Eng. Math., 38 (2021), 257–270. https://doi.org/10.3969/j.issn.1005-3085.2021.02.009 doi: 10.3969/j.issn.1005-3085.2021.02.009

|

| [21] | Y. K. Kwork, Mathematical models of financial derivatives, Springer, 2008. |

| [22] | C. Brunetti, A. Caldarera, Asset prices and asset correlations in illiquid markets, C. E. F., 2006. |

Figures(6) / Tables(1)

Kaihang Zhang, Liting Gao. Digital power generalized exchange option pricing considering liquidity risk[J]. AIMS Mathematics, 2026, 11(1): 1761-1776. doi: 10.3934/math.2026073

DownLoad:

DownLoad: