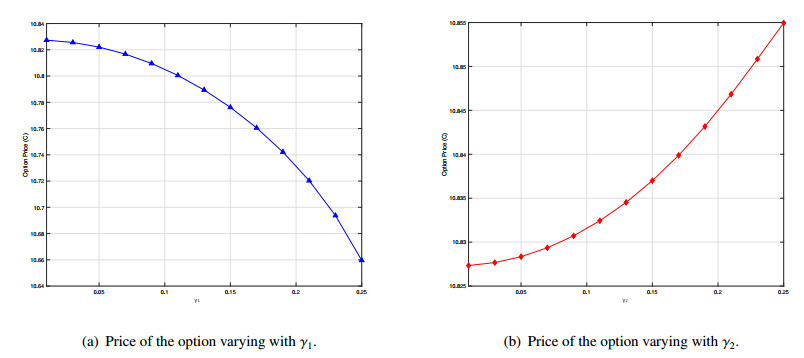

We derive the explicit pricing formulas for vulnerable options under a stochastic volatility model with stochastic long-term mean. We extend the He and Chen model to incorporate counterparty default risk and derive explicit solutions for option prices using the characteristic function of the underlying asset's log-price. The option writer defaults when their asset value falls below a predetermined boundary, reducing the option payoff. Our numerical examples show that option prices are highly sensitive to default boundaries and exhibit asymmetric responses to volatility parameters.

Citation: So-Yoon Cho, Geonwoo Kim. Analytical valuation of vulnerable options under a stochastic volatility model with a stochastic long-term mean[J]. AIMS Mathematics, 2025, 10(9): 20219-20234. doi: 10.3934/math.2025903

We derive the explicit pricing formulas for vulnerable options under a stochastic volatility model with stochastic long-term mean. We extend the He and Chen model to incorporate counterparty default risk and derive explicit solutions for option prices using the characteristic function of the underlying asset's log-price. The option writer defaults when their asset value falls below a predetermined boundary, reducing the option payoff. Our numerical examples show that option prices are highly sensitive to default boundaries and exhibit asymmetric responses to volatility parameters.

| [1] | F. Black, M. Scholes, The pricing of options and corporate liabilities, J. Polit. Econ., 81 (1973), 637–654. |

| [2] | D. Duffie, J. Pan, K. Singleton, Transform analysis and asset pricing for affine jump-diffusions, Econometrica, 68 (2000), 1343–1376. |

| [3] |

J. Gatheral, T. Jaisson, M. Rosenbaum, Volatility is rough, Quant. Finance, 18 (2018), 933–949. https://doi.org/10.1080/14697688.2017.1393551 doi: 10.1080/14697688.2017.1393551

|

| [4] |

X. J. He, W. Chen, A closed-form pricing formula for european options under a new stochastic volatility model with a stochastic long-term mean, Math. Finan. Econ., 15 (2021), 381–396. https://doi.org/10.1007/s11579-020-00281-y doi: 10.1007/s11579-020-00281-y

|

| [5] |

X. J. He, S. D. Huang, S. Lin, A closed-form solution for pricing european-style options under the heston model with credit and liquidity risks, Commun. Nonlinear Sci. Numer. Simul., 143 (2025), 108595. https://doi.org/10.1016/j.cnsns.2025.108595 doi: 10.1016/j.cnsns.2025.108595

|

| [6] |

S. Huang, X. J. He, Analytical approximation of european option prices under a new two-factor non-affine stochastic volatility model, AIMS Math., 8 (2023), 4875–4891. https://doi.org/10.3934/math.2023243 doi: 10.3934/math.2023243

|

| [7] | S. L Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Rev. Financ. Stud., 6 (1993), 327–343. |

| [8] |

J. Jeon, G. Kim, Analytically pricing a vulnerable option under a stochastic liquidity risk model with stochastic volatility, Mathematics, 12 (2024), 2642. https://doi.org/10.3390/math12172642 doi: 10.3390/math12172642

|

| [9] |

H. Johnson, R. Stulz, The pricing of options with default risk, J. Finance, 42 (1987), 267–280. https://doi.org/10.2307/2328252 doi: 10.2307/2328252

|

| [10] |

P. Klein, Pricing black-scholes options with correlated credit risk, J. Bank. Finance, 20 (1996), 1211–1229. https://doi.org/10.1016/0378-4266(95)00052-6 doi: 10.1016/0378-4266(95)00052-6

|

| [11] |

M. K. Lee, J. H. Kim, Pricing of defaultable options with multiscale generalized heston's stochastic volatility, Math. Comput. Simul., 144 (2018), 235–246. https://doi.org/10.1016/j.matcom.2017.08.005 doi: 10.1016/j.matcom.2017.08.005

|

| [12] |

G. Lv, P. Xu, Y. Zhang, Pricing of vulnerable options based on an uncertain cir interest rate model, AIMS Math., 8 (2023), 11113–11130. https://doi.org/10.3934/math.2023563 doi: 10.3934/math.2023563

|

| [13] |

G. Wang, X. Wang, K. Zhou, Pricing vulnerable options with stochastic volatility, Phys. A: Stat. Mech. Appl., 485 (2017), 91–103. https://doi.org/10.1016/j.physa.2017.04.146 doi: 10.1016/j.physa.2017.04.146

|

| [14] |

X. Wang, W. Xiao, J. Yu, Modeling and forecasting realized volatility with the fractional ornstein–uhlenbeck process, J. Econometrics, 232 (2023), 389–415. https://doi.org/10.1016/j.jeconom.2021.08.001 doi: 10.1016/j.jeconom.2021.08.001

|

| [15] |

X. Wang, Analytical valuation of asian options with counterparty risk under stochastic volatility models, J. Futures Markets, 40 (2020), 410–429. https://doi.org/10.1002/fut.22064 doi: 10.1002/fut.22064

|

| [16] | W. Xiao, J. Yu, Asymptotic theory for estimating drift parameters in the fractional vasicek model, Econometric Theory, 35 (2019), 198–231. |

| [17] |

W. Xiao, Jun Yu, Asymptotic theory for rough fractional vasicek models, Econ. Lett., 177 (2019), 26–29. https://doi.org/10.1016/j.econlet.2019.01.020 doi: 10.1016/j.econlet.2019.01.020

|

| [18] |

Y. Xie, G. Deng, Vulnerable european option pricing in a markov regime-switching heston model with stochastic interest rate, Chaos, Soliton. Fract., 156 (2022), 111896. https://doi.org/10.1016/j.chaos.2022.111896 doi: 10.1016/j.chaos.2022.111896

|

| [19] |

S. J. Yang, M. K. Lee, J. H. Kim, Pricing vulnerable options under a stochastic volatility model, Appl. Math. Lett., 34 (2014), 7–12. https://doi.org/10.1016/j.aml.2014.03.007 doi: 10.1016/j.aml.2014.03.007

|

| [20] |

A. Yun, G. Kim, Valuing options with hybrid default risk under the stochastic volatility model, Finance Res. Lett., 72 (2025), 106521. https://doi.org/10.1016/j.frl.2024.106521 doi: 10.1016/j.frl.2024.106521

|

| [21] |

Q. Zhou, Q. Wang, W. Wu, Pricing vulnerable options with variable default boundary under jump-diffusion processes, Adv. Differ. Equ., 2018 (2018), 465. https://doi.org/10.1186/s13662-018-1915-1 doi: 10.1186/s13662-018-1915-1

|

Figures(5) / Tables(2)

So-Yoon Cho, Geonwoo Kim. Analytical valuation of vulnerable options under a stochastic volatility model with a stochastic long-term mean[J]. AIMS Mathematics, 2025, 10(9): 20219-20234. doi: 10.3934/math.2025903

DownLoad:

DownLoad: