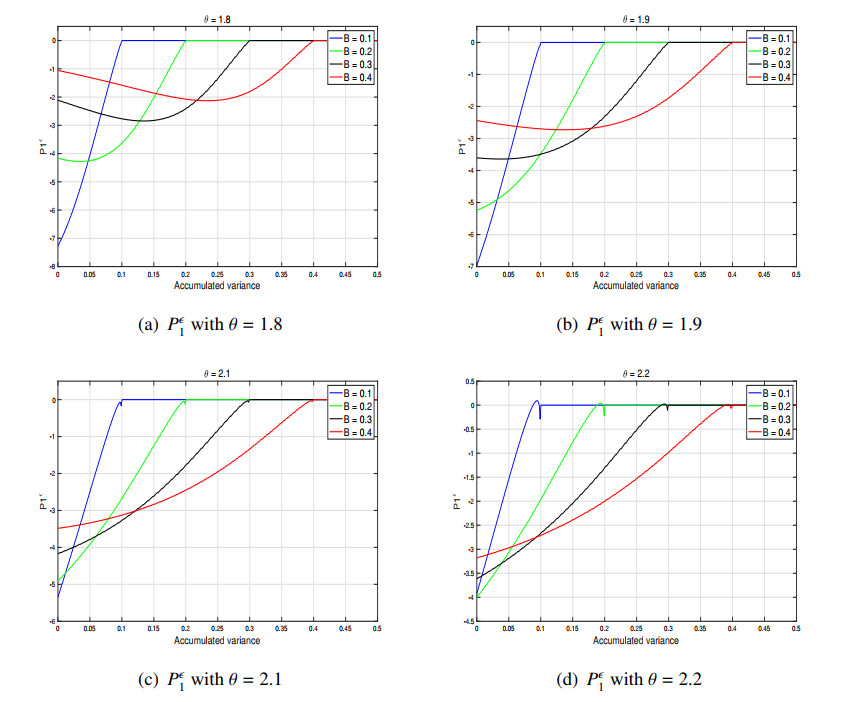

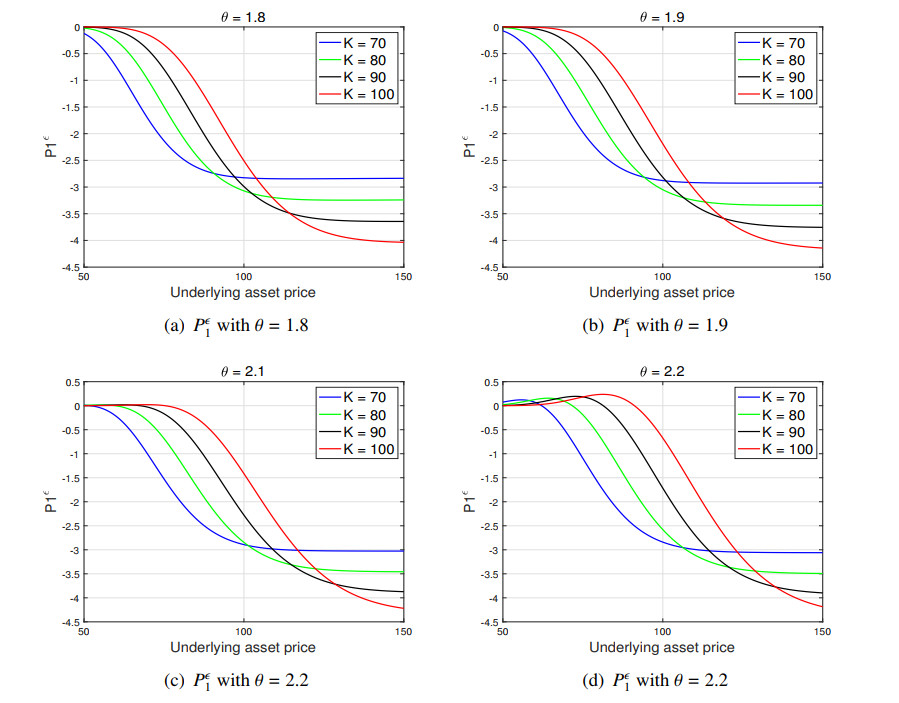

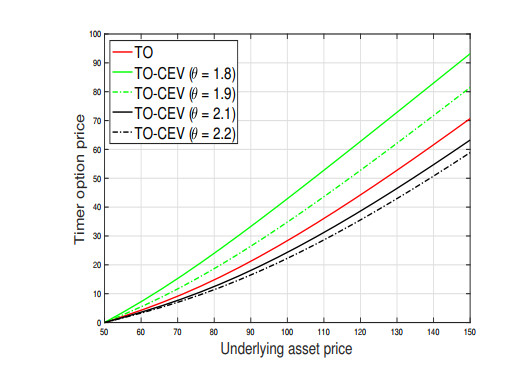

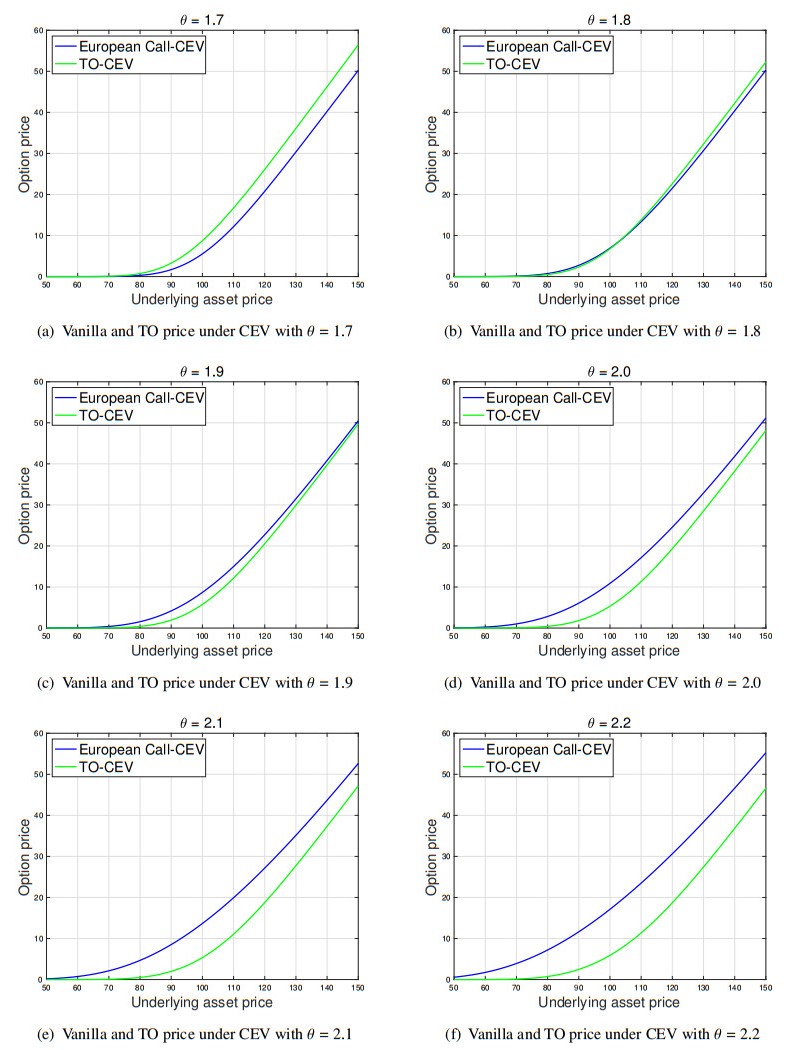

Timer options, which were first introduced by Société Générale Corporate and Investment Banking in 2007, are financial securities whose payoffs and exercise are determined by a random time associated with the accumulated realized variance of the underlying asset, unlike vanilla options exercised at the prescribed maturity date. In this paper, taking account of the correlation between the underlying asset price and volatility, we investigate the pricing of timer options under the constant elasticity of variance (CEV) model, proposed by Cox and Ross [

Citation: Sun-Yong Choi, Donghyun Kim, Ji-Hun Yoon. An analytic pricing formula for timer options under constant elasticity of variance with stochastic volatility[J]. AIMS Mathematics, 2024, 9(1): 2454-2472. doi: 10.3934/math.2024121

Timer options, which were first introduced by Société Générale Corporate and Investment Banking in 2007, are financial securities whose payoffs and exercise are determined by a random time associated with the accumulated realized variance of the underlying asset, unlike vanilla options exercised at the prescribed maturity date. In this paper, taking account of the correlation between the underlying asset price and volatility, we investigate the pricing of timer options under the constant elasticity of variance (CEV) model, proposed by Cox and Ross [

| [1] | F. Black, M. Scholes, The pricing of options and corporate liabilities, J. Polit. Econ., 81 (1973), 637–654. |

| [2] |

S. L. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Rev. Financ. Stud., 6 (1993), 327–343. https://doi.org/10.1093/rfs/6.2.327 doi: 10.1093/rfs/6.2.327

|

| [3] | J. P. Fouque, G. Papanicolaou, R. Sircar, K. Sølna, Multiscale stochastic volatility for equity, interest rate, and credit derivatives, Cambridge University Press, 2011. |

| [4] |

J. Hull, A. White, The pricing of options on assets with stochastic volatilities, J. Financ., 42 (1987), 281–300. https://doi.org/10.1111/j.1540-6261.1987.tb02568.x doi: 10.1111/j.1540-6261.1987.tb02568.x

|

| [5] |

L. O. Scott, Option pricing when the variance changes randomly: Theory, estimation, and an application, J. Financ. Quant. Anal., 22 (1987), 419–438. https://doi.org/10.2307/2330793 doi: 10.2307/2330793

|

| [6] |

M. Chesney, L. Scott, Pricing European currency options: A comparison of the modified Black-Scholes model and a random variance model, J. Financ. Quant. Anal., 24 (1989), 267–284. https://doi.org/10.2307/2330812 doi: 10.2307/2330812

|

| [7] |

R. Schöbel, J. Zhu, Stochastic volatility with an Ornstein-Uhlenbeck process: An extension, Rev. Financ., 3 (1999), 23–46. https://doi.org/10.1023/A:1009803506170 doi: 10.1023/A:1009803506170

|

| [8] | B. Dupire, Pricing with a smile, Risk, 7 (1994), 18–20. |

| [9] | E. Derman, I. Kani, Riding on a smile, Risk, 7 (1994), 32–39. |

| [10] |

J. C. Cox, S. A. Ross, The valuation of options for alternative stochastic processes, J. Financ. Econ., 3 (1976), 145–166. https://doi.org/10.1016/0304-405X(76)90023-4 doi: 10.1016/0304-405X(76)90023-4

|

| [11] |

Y. Tian, Z. Zhu, G. Lee, F. Klebaner, K. Hamza, Calibrating and pricing with a stochastic-local volatility model, J. Deriv., 22 (2015), 21–39. https://doi.org/10.3905/jod.2015.22.3.021 doi: 10.3905/jod.2015.22.3.021

|

| [12] | E. Ghysels, A. C. Harvey, E. Renault, 5 Stochastic volatility, Handb. Stat., 14 (1996), 119–191. https://doi.org/10.1016/S0169-7161(96)14007-4 |

| [13] |

A. W. V. Stoep, L. A. Grzelak, C. W. Oosterlee, The Heston stochastic-local volatility model: Efficient Monte Carlo simulation, Int. J. Theor. Appl. Fin., 17 (2014), 1450045. https://doi.org/10.1142/S0219024914500459 doi: 10.1142/S0219024914500459

|

| [14] |

Z. Cui, J. L. Kirkby, D. Nguyen, A general valuation framework for SABR and stochastic local volatility models, SIAM J. Financ. Math., 9 (2018), 520–563. https://doi.org/10.1137/16M1106572 doi: 10.1137/16M1106572

|

| [15] |

L. B. Andersen, V. V. Piterbarg, Moment explosions in stochastic volatility models, Financ. Stoch., 11 (2007), 29–50. https://doi.org/10.1007/s00780-006-0011-7 doi: 10.1007/s00780-006-0011-7

|

| [16] |

R. Lord, R. Koekkoek, D. V. Dijk, A comparison of biased simulation schemes for stochastic volatility models, Quant. Financ., 10 (2010), 177–194. https://doi.org/10.1080/14697680802392496 doi: 10.1080/14697680802392496

|

| [17] |

S. Y. Choi, J. P. Fouque, J. H. Kim, Option pricing under hybrid stochastic and local volatility, Quant. Financ., 13 (2013), 1157–1165. https://doi.org/10.1080/14697688.2013.780209 doi: 10.1080/14697688.2013.780209

|

| [18] |

Z. Cui, J. L. Kirkby, D. Nguyen, Efficient simulation of generalized SABR and stochastic local volatility models based on Markov chain approximations, Eur. J. Oper. Res., 290 (2021), 1046–1062. https://doi.org/10.1016/j.ejor.2020.09.008 doi: 10.1016/j.ejor.2020.09.008

|

| [19] |

P. Carr, D. Madan, Towards a theory of volatility trading, Volat. New Estim. Tech. Pric. Deriv., 29 (1998), 417–427. https://doi.org/10.1017/CBO9780511569708.013 doi: 10.1017/CBO9780511569708.013

|

| [20] |

A. Badescu, Z. Cui, J. P. Ortega, Closed-form variance swap prices under general affine GARCH models and their continuous-time limits, Ann. Oper. Res., 282 (2019), 27–57. https://doi.org/10.1007/s10479-018-2941-9 doi: 10.1007/s10479-018-2941-9

|

| [21] |

K. Demeterfi, E. Derman, M. Kamal, A guide to volatility and variance swaps, J. Deriv., 6 (1999), 9–32. https://doi.org/10.3905/jod.1999.319129 doi: 10.3905/jod.1999.319129

|

| [22] |

S. P. Zhu, G. H. Lian, A closed-form exact solution for pricing variance swaps with stochastic volatility, Math. Financ., 21 (2011), 233–256. https://doi.org/10.1111/j.1467-9965.2010.00436.x doi: 10.1111/j.1467-9965.2010.00436.x

|

| [23] |

W. Zheng, Y. K. Kwok, Closed form pricing formulas for discretely sampled generalized variance swaps, Math. Financ., 24 (2014), 855–881. https://doi.org/10.1111/mafi.12016 doi: 10.1111/mafi.12016

|

| [24] |

A. Issaka, Variance swaps, volatility swaps, hedging and bounds under multi-factor Heston stochastic volatility model, Stoch. Anal. Appl., 38 (2020), 856–874. https://doi.org/10.1080/07362994.2020.1730903 doi: 10.1080/07362994.2020.1730903

|

| [25] |

Y. Xi, H. Y. Wong, Discrete variance swap in a rough volatility economy, J. Futures Markets, 41 (2021), 1640–1654. https://doi.org/10.1002/fut.22242 doi: 10.1002/fut.22242

|

| [26] |

O. E. Euch, M. Rosenbaum, The characteristic function of rough Heston models, Math. Financ., 29 (2019), 3–38. https://doi.org/10.1111/mafi.12173 doi: 10.1111/mafi.12173

|

| [27] | A Neuberger, Volatility trading, Institute of Finance and Accounting: London Business School, Working Paper, 1990. |

| [28] | N. Sawyer, SG CIB launches timer options, Risk, 20 (2007), 6. |

| [29] |

A. Bick, Quadratic-variation-based dynamic strategies, Manag. Sci., 41 (1995), 722–732. https://doi.org/10.1287/mnsc.41.4.722 doi: 10.1287/mnsc.41.4.722

|

| [30] | C. Li, Managing volatility risk innovation of financial derivatives, stochastic models and their analytical implementation, Doctoral dissertation, Columbia University, 2010. |

| [31] | D. Saunders, Pricing timer options under fast mean-reverting stochastic volatility, Can. Appl. Math. Q., 17 (2009), 737–753. |

| [32] |

L. Z. J. Liang, D. Lemmens, J. Tempere, Path integral approach to the pricing of timer options with the Duru-Kleinert time transformation, Phys. Rev. E, 83 (2011), 056112. https://doi.org/10.1103/PhysRevE.83.056112 doi: 10.1103/PhysRevE.83.056112

|

| [33] | C. Bernard, Z. Cui, Pricing timer options, J. Comput. Financ., 15 (2011), 1–37. https://doi.org/10.21314/JCF.2011.228 |

| [34] |

M. Li, F. Mercurio, Closed-form approximation of perpetual timer option prices, Int. J. Theor. Appl. Fin., 17 (2014), 1450026. https://doi.org/10.1142/S0219024914500265 doi: 10.1142/S0219024914500265

|

| [35] |

J. Ma, D. Deng, Y. Lai, Explicit approximate analytic formulas for timer option pricing with stochastic interest rates, North Am. J. Econ. Financ., 34 (2015), 1–21. https://doi.org/10.1016/j.najef.2015.07.002 doi: 10.1016/j.najef.2015.07.002

|

| [36] | C. Li, Bessel processes, stochastic volatility, and timer options, Math. Financ., 26 (2016), 122–148. https://doi.org/10.1111/mafi.12041 |

| [37] |

J. Zhang, X. Lu, Y. Han, Pricing perpetual timer option under the stochastic volatility model of Hull-White, ANZIAM J., 58 (2017), 406–416. https://doi.org/10.21914/anziamj.v58i0.11281 doi: 10.21914/anziamj.v58i0.11281

|

| [38] |

Z. Cui, J. L. Kirkby, G. Lian, D. Nguyen, Integral representation of probability density of stochastic volatility models and timer options, Int. J. Theor. Appl. Fin., 20 (2017), 1750055. https://doi.org/10.1142/S0219024917500558 doi: 10.1142/S0219024917500558

|

| [39] |

X. Wang, S. J. Wu, X. Yue, Pricing timer options: Second-order multiscale stochastic volatility asymptotics, ANZIAM J., 63 (2021), 249–267. https://doi.org/10.21914/anziamj.v63.15291 doi: 10.21914/anziamj.v63.15291

|

| [40] |

J. L. Kirkby, J. P. Aguilar, The return barrier and return timer option with pricing under Levy processes, Expert Syst. Appl., 233 (2023), 120920. https://doi.org/10.1016/j.eswa.2023.120920 doi: 10.1016/j.eswa.2023.120920

|

| [41] |

B. Bock, S. Y. Choi, J. H. Kim, The pricing of European options under the constant elasticity of variance with stochastic volatility, Fluct. Noise Lett., 12 (2013), 1350004. https://doi.org/10.1142/S0219477513500041 doi: 10.1142/S0219477513500041

|

| [42] |

J. H. Kim, M. K. Lee, S. Y. Sohn, Investment timing under hybrid stochastic and local volatility, Chaos Soliton. Fract., 67 (2014), 58–72. https://doi.org/10.1016/j.chaos.2014.06.007 doi: 10.1016/j.chaos.2014.06.007

|

| [43] |

S. Y. Choi, J. H. Kim, Equity-linked annuities with multiscale hybrid stochastic and local volatility, Scand. Actuar. J., 2016 (2016), 466–487. https://doi.org/10.1080/03461238.2014.955048 doi: 10.1080/03461238.2014.955048

|

| [44] |

S. Y. Choi, J. H. Kim, J. H. Yoon, Foreign exchange rate volatility smiles and smirks, Appl. Stoch. Model. Bus., 37 (2021), 628–660. https://doi.org/10.1002/asmb.2602 doi: 10.1002/asmb.2602

|

| [45] |

J. P. Fouque, G. Papanicolaou, K. R. Sircar, Mean-reverting stochastic volatility, Int. J. Theor. Appl. Fin., 3 (2000), 101–142. https://doi.org/10.1142/S0219024900000061 doi: 10.1142/S0219024900000061

|

| [46] |

H. Geman, Y. F. Shih, Modeling commodity prices under the CEV model, J. Altern. Invest., 11 (2009), 65–84. https://doi.org/10.3905/JAI.2009.11.3.065 doi: 10.3905/JAI.2009.11.3.065

|

| [47] | B. Øksendal, Stochastic differential equations: An introduction with applications, 6 Eds., Springer, 2010. |

| [48] |

M. Ha, D. Kim, J. H. Yoon, Valuing of timer path-dependent options, Math. Comput. Simul., 215 (2024), 208–227. https://doi.org/10.1016/j.matcom.2023.08.010 doi: 10.1016/j.matcom.2023.08.010

|

| [49] | A. Lipton, Mathematical methods for foreign exchange: A financial engineer's approach, World Scientific, 2001. https://doi.org/10.1142/4694 |

| [50] |

J. P. Fouque, M. J. Lorig, A fast mean-reverting correction to Heston's stochastic volatility model, SIAM J. Financ. Math., 2 (2011), 221–254. https://doi.org/10.1137/090761458 doi: 10.1137/090761458

|

Figures(4) / Tables(1)

Sun-Yong Choi, Donghyun Kim, Ji-Hun Yoon. An analytic pricing formula for timer options under constant elasticity of variance with stochastic volatility[J]. AIMS Mathematics, 2024, 9(1): 2454-2472. doi: 10.3934/math.2024121

DownLoad:

DownLoad: