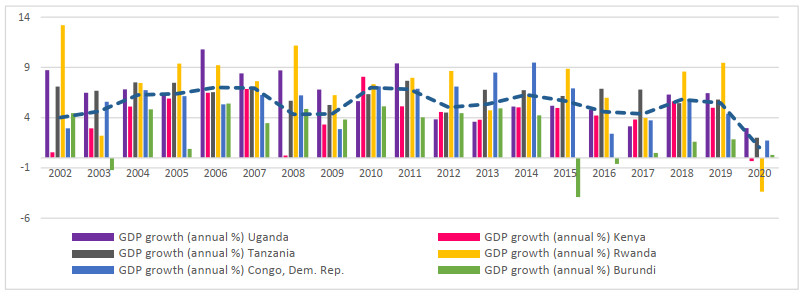

Models of crisis prediction continue to gain traction with the increased frequency of global crisis such as the ongoing COVID-19 pandemic. Moreover, the connectedness of financial markets appears to be of central importance in determining how shocks spill through asset market linkages. The study thus applies the time-frequency connectedness measures of Diebold & Yilmaz (2012) and Baruník & Křehlík (2018) to examine return and volatility connectedness dynamics in East African Community (EAC) member states. The study found a strong interdependence among the considered EAC markets as indicated by the high values of total return and volatility spillover indices. This high degree of interdependence is reflected in both static time and frequency domain return and volatility connectedness, especially at the longer term frequency bands, an indication that return and volatility shocks are persistent. This result lends further support to existing evidence on the suitability of the EAC regional economic integration, including the possible eventual establishment of a monetary union. In addition, the dynamic spillover analysis indicates that connectedness among these EAC markets is highly time-varying and appears to be amplified during global crisis events such as the European debt crisis, Kenyan elections, commodity price shocks and the COVID-19 pandemic. However, the results suggest that relative to periods of domestic turbulence, financial market connectedness in the EAC is more likely to get amplified during periods of external global shocks. The study also contributes to emergent literature on connectedness among financial markets during the COVID-19 pandemic. Importantly, the study finds that the COVID-19 pandemic had a significant effect on all the considered EAC markets although the magnitude and direction of impact varies across markets and countries. In addition, the study finds that Brent Crude oil prices are a significant source of return and volatility spillovers to EAC markets especially during crisis periods.

Citation: Lorna Katusiime. 2022: Time-Frequency connectedness between developing countries in the COVID-19 pandemic: The case of East Africa, Quantitative Finance and Economics, 6(4): 722-748. doi: 10.3934/QFE.2022032

Models of crisis prediction continue to gain traction with the increased frequency of global crisis such as the ongoing COVID-19 pandemic. Moreover, the connectedness of financial markets appears to be of central importance in determining how shocks spill through asset market linkages. The study thus applies the time-frequency connectedness measures of Diebold & Yilmaz (2012) and Baruník & Křehlík (2018) to examine return and volatility connectedness dynamics in East African Community (EAC) member states. The study found a strong interdependence among the considered EAC markets as indicated by the high values of total return and volatility spillover indices. This high degree of interdependence is reflected in both static time and frequency domain return and volatility connectedness, especially at the longer term frequency bands, an indication that return and volatility shocks are persistent. This result lends further support to existing evidence on the suitability of the EAC regional economic integration, including the possible eventual establishment of a monetary union. In addition, the dynamic spillover analysis indicates that connectedness among these EAC markets is highly time-varying and appears to be amplified during global crisis events such as the European debt crisis, Kenyan elections, commodity price shocks and the COVID-19 pandemic. However, the results suggest that relative to periods of domestic turbulence, financial market connectedness in the EAC is more likely to get amplified during periods of external global shocks. The study also contributes to emergent literature on connectedness among financial markets during the COVID-19 pandemic. Importantly, the study finds that the COVID-19 pandemic had a significant effect on all the considered EAC markets although the magnitude and direction of impact varies across markets and countries. In addition, the study finds that Brent Crude oil prices are a significant source of return and volatility spillovers to EAC markets especially during crisis periods.

| [1] | Agénor PR, Pereira da Silva LA (2018) Financial spillovers, spillbacks, and the scope for international macroprudential policy coordination. Bank for International Settlements, BIS Paper(97). |

| [2] |

Agyei SK (2022) Diversification Benefits between Stock Returns from Ghana and Jamaica: Insights from Time-Frequency and VMD-Based Asymmetric Quantile-on-Quantile Analysis. Math Probl Eng 2022: 9375170. https://doi.org/10.1155/2022/9375170 doi: 10.1155/2022/9375170

|

| [3] |

Agyei SK, Bossman A, Asafo−Adjei E, et al. (2022) Exchange Rate, COVID-19, and Stock Returns in Africa: Insights from Time-Frequency Domain. Discrete Dyn Nat Soc 2022: 4372808. https://doi.org/10.1155/2022/4372808 doi: 10.1155/2022/4372808

|

| [4] | Al Jazeera (2021) Kenya lifts longstanding COVID curfew as infections ease. Available from: https://www.aljazeera.com/news/2021/10/20/kenya-lifts-longstanding-covid-curfew-as-infections-ease. |

| [5] |

Anyanwu JC, Salami AO (2021) The impact of COVID-19 on African economies: An introduction. Afr Dev Rev 33: S1–S16. https://doi.org/10.1111/1467-8268.12531 doi: 10.1111/1467-8268.12469

|

| [6] |

Assifuah-Nunoo E, Junior PO, Adam AM, et al. (2022) Assessing the safe haven properties of oil in African stock markets amid the COVID-19 pandemic: a quantile regression analysis. Quant Financ Econ 6: 244–269. https://doi.org/10.3934/QFE.2022011 doi: 10.3934/QFE.2022011

|

| [7] |

Bagheri E, Ebrahimi SB (2020) Estimating Network Connectedness of Financial Markets and Commodities. J Syst Sci Syst Eng 29: 572–589. https://doi.org/10.1007/s11518-020-5465-1 doi: 10.1007/s11518-020-5465-1

|

| [8] | Bank of Uganda (2019) Bank of Uganda Monetary Policy Rep. Available from: https://www.bou.or.ug/bou/bouwebsite/bouwebsitecontent/MonetaryPolicy/Monetary_Policy_Reports/2019/Dec/DEC-2019-Monetary-Policy-Report.pdf. |

| [9] |

Barrot LD, Calderón C, Servén L (2018) Openness, specialization, and the external vulnerability of developing countries. J Dev Econ 134: 310–328. https://doi.org/10.1016/j.jdeveco.2018.05.015 doi: 10.1016/j.jdeveco.2018.05.015

|

| [10] | Baruník J, Kocenda E, Vácha L (2015) Volatility spillovers across petroleum markets. http://dx.doi.org/10.2139/ssrn.2600204 |

| [11] |

Baruník J, Křehlík T (2018) Measuring the Frequency Dynamics of Financial Connectedness and Systemic Risk*. J Financ Econ 16: 271–296. https://doi.org/10.1093/jjfinec/nby001 doi: 10.1093/jjfinec/nby001

|

| [12] | Daily Monitor (2022) Uganda's Museveni reopens economy amidst surge in Covid-19 — The East African. Available from: https://www.theeastafrican.co.ke/tea/news/east-africa/uganda-museveni-reopens-economy-amidst-surge-in-covid-19-3669258. |

| [13] | Degutis A, Novickytė L (2014) The efficient market hypothesis: A critical review of literature and methodology. Ekonomika 93: 7–23. |

| [14] | Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74: 427–431. |

| [15] |

Diebold FX, Yilmaz K (2009) Measuring Financial Asset Return and Volatility Spillovers, With Application To Global Equity Markets. Econ J 119: 158–171. doi: 10.1111/j.1468-0297.2008.02208.x

|

| [16] |

Diebold FX, Yilmaz K (2012) Better to give than to receive: Predictive directional measurement of volatility spillovers. Int J Forecast 28: 57–66. https://doi.org/10.1016/j.ijforecast.2011.02.006 doi: 10.1016/j.ijforecast.2011.02.006

|

| [17] | Dieppe AM, Kilic Celik S, Okou CIF (2020) Implications of Major Adverse Events on Productivity. Available from: http://documents.worldbank.org/curated/en/706191600779573582/Implications-of-Major-Adverse-Events-on-Productivit. |

| [18] | Drummond P, Aisen A, Alper CE, et al. (2015) Toward a monetary union in the East African Community: asymmetric shocks, exchange rates, and risk-sharing mechanisms. International Monetary Fund. |

| [19] |

Eberhardt M, Presbitero AF (2018) Commodity Price Movements and Banking Crises. IMF Working Papers 2018: 54. https://doi.org/10.5089/9781484366776.001.A000 doi: 10.5089/9781484366776.001.A000

|

| [20] | Gill I (2022) Developing economies must act now to dampen the shocks from the Ukraine conflict. Available from: https://blogs.worldbank.org/voices/developing-economies-must-act-now-dampen-shocks-ukraine-conflict. |

| [21] |

Hung NT, Vo XV (2021) Directional spillover effects and time-frequency nexus between oil, gold and stock markets: Evidence from pre and during COVID-19 outbreak. Int Rev Financ Anal 76: 101730. https://doi.org/10.1016/j.irfa.2021.101730 doi: 10.1016/j.irfa.2021.101730

|

| [22] | International Monetary Fund (2003) Fund Assistance for Countries Facing Exogenous Shocks. Int Monetary Fund. Available from: http://www.imf.org/external/np/pdr/sustain/2003/080803.pdf. |

| [23] | Juma C (2016) Brexit is an opportunity for Africa, World Economic Forum. World Economic Forum. Available from: https://www.weforum.org/agenda/2016/07/brexit-is-an-opportunity-for-africa/ |

| [24] | Kasekende L, Ng'eno NK (2000) Regional integration and economic integration in Eastern and Southern Africa. In: Oyejide, A., Elbadawi, I., Collier, P.(Eds.), Regional Integration and Trade Liberalization in Sub-Saharan Africa: Framework, Issues and Methodological Perspectives, 1, Macmillan Press Ltd. |

| [25] |

Katusiime L (2019) Investigating Spillover Effects between Foreign Exchange Rate Volatility and Commodity Price Volatility in Uganda. Economies 7: 1. https://doi.org/10.3390/economies7010001 doi: 10.3390/economies7010001

|

| [26] |

Katusiime L (2021) COVID 19 and Bank Profitability in Low Income Countries: The Case of Uganda. J Risk Financ Manage 14: 588. https://doi.org/10.3390/jrfm14120588 doi: 10.3390/jrfm14120588

|

| [27] |

Koop G, Pesaran MH, Potter SM (1996) Impulse response analysis in nonlinear multivariate models. J Econometrics 74: 119–147. https://doi.org/10.1016/0304-4076(95)01753-4 doi: 10.1016/0304-4076(95)01753-4

|

| [28] |

Kwiatkowski D, Phillips PCB, Schmidt P, et al. (1992) Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J Econometrics 54: 159–178. https://doi.org/10.1016/0304-4076(92)90104-Y doi: 10.1016/0304-4076(92)90104-Y

|

| [29] |

Langevoort DC (1992) Theories, assumptions, and securities regulation: Market efficiency revisited. U Penn Law Rev 140: 851–920. doi: 10.2307/3312329

|

| [30] |

Li X, Li B, Wei G, et al. (2021). Return connectedness among commodity and financial assets during the COVID-19 pandemic: Evidence from China and the US. Resour Policy 73: 102166. https://doi.org/10.1016/j.resourpol.2021.102166 doi: 10.1016/j.resourpol.2021.102166

|

| [31] |

Lin S, Chen S (2021) Dynamic connectedness of major financial markets in China and America. Int Rev Econ Financ 75: 646–656. https://doi.org/10.1016/j.iref.2021.04.033 doi: 10.1016/j.iref.2021.04.033

|

| [32] | Lo AW (2008) Efficient markets hypothesis. New Palgrave Dictionary Econ 2: 1–17. |

| [33] | López J, Perrotini I (2006) On floating exchange rates, currency depreciation and effective demand. Q Review-Banca Nazionale Del Lavoro 238: 221. |

| [34] | Mahadeva L, Sterne G (2012) Monetary policy frameworks in a global context. Routledge. |

| [35] |

Mensi W, Shafiullah M, Vo XV, et al. (2021) Volatility spillovers between strategic commodity futures and stock markets and portfolio implications: Evidence from developed and emerging economies. Resour Policy 71: 102002. https://doi.org/10.1016/j.resourpol.2021.102002 doi: 10.1016/j.resourpol.2021.102002

|

| [36] |

Minoiu C, Kang C, Subrahmanian VS, et al. (2015) Does financial connectedness predict crises? Quant Financ 15: 607–624. https://doi.org/10.1080/14697688.2014.968358 doi: 10.1080/14697688.2014.968358

|

| [37] |

Mokni K, Mansouri F (2017) Conditional dependence between international stock markets: A long memory GARCH-copula model approach. J Multinatl Financ Manage 42–43: 116–131. https://doi.org/10.1016/j.mulfin.2017.10.006 doi: 10.1016/j.mulfin.2017.10.006

|

| [38] | Moore J (2017) Uhuru Kenyatta Is Declared Winner of Kenya's Repeat Election—The New York Times. The New York Times. Available from: https://www.nytimes.com/2017/10/30/world/africa/kenya-election-kenyatta-odinga.html. |

| [39] |

N Price G, U Elu J (2014) Does regional currency integration ameliorate global macroeconomic shocks in sub-Saharan Africa? The case of the 2008–2009 global financial crisis. J Econ Stud 41: 737–750. https://doi.org/10.1108/JES-08-2011-0092 doi: 10.1108/JES-08-2011-0092

|

| [40] |

Ogbuabor JE, Anthony-Orji OI, Manasseh CO, et al. (2020) Measuring the dynamics of COMESA output connectedness with the global economy. J Econ Asymmetries 21: e00138. https://doi.org/10.1016/j.jeca.2019.e00138 doi: 10.1016/j.jeca.2019.e00138

|

| [41] |

Owusu Junior P, Agyei SK, Adam AM, et al. (2022). Time-frequency connectedness between food commodities: New implications for portfolio diversification. Environ Challenges 9: 100623. https://doi.org/10.1016/j.envc.2022.100623 doi: 10.1016/j.envc.2022.100623

|

| [42] | Palanska T (2020) Measurement of Volatility Spillovers and Asymmetric Connectedness on Commodity and Equity Markets. Czech J Econ Financ (Finance a Uver) 70: 42–69. |

| [43] | Pesaran HH, Shin Y (1998) Generalized impulse response analysis in linear multivariate models. Econ Lett 58: 17–29. https://doi.org/10.1016/S0165-1765(97)00214-0 |

| [44] | Phillips PCB, Perron P (1988) Testing for a unit root in time series regression. Biometrika 75: 335–346. |

| [45] | Prasad ES, Rogoff K, Wei SJ, et al. (2003) Effects of Financial Globalization on Developing Countries: Some Empirical Evidence. International Monetary Fund. |

| [46] |

Raddatz C (2007) Are external shocks responsible for the instability of output in low-income countries? J Dev Econ 84: 155–187. https://doi.org/10.1016/j.jdeveco.2006.11.001 doi: 10.1016/j.jdeveco.2006.11.001

|

| [47] | Stocker M, Baffes J, Vorisek D (2018) What triggered the oil price plunge of 2014–2016 and why it failed to deliver an economic impetus in eight charts. World Bank Blog. Available from: https://blogs.worldbank.org/developmenttalk/what-triggered-oil-price-plunge-2014-2016-and-why-it-failed-deliver-economic-impetus-eight-charts. |

| [48] | The EastAfrican (2012) EAC economies feel the pinch of Eurozone crisis—The East African. Available from: https://www.theeastafrican.co.ke/tea/business/eac-economies-feel-the-pinch-of-eurozone-crisis--1311184. |

| [49] | The World Bank (2017) Reviving Private Sector Credit Growth and Boosting Revenue Mobilization to Support Fiscal Consolidation POISED TO BOUNCE BACK? Available from: https://openknowledge.worldbank.org/bitstream/handle/10986/29033/121895-WP-P162368-PUBLIC-KenyaEconomicUpdateFINAL.pdf?sequence=1&isAllowed=y. |

| [50] | Tobin J, de Macedo JB (1979) The short-run macroeconomics of floating exchange rates: An exposition. |

| [51] |

Uluceviz E, Yilmaz K (2021) Measuring real–financial connectedness in the U.S. economy. The North American J Econ Financ 58: 101554. https://doi.org/10.1016/j.najef.2021.101554 doi: 10.1016/j.najef.2021.101554

|

| [52] |

Umar Z, Gubareva M (2020) A time–frequency analysis of the impact of the Covid-19 induced panic on the volatility of currency and cryptocurrency markets. J Behav Exp Financ 28: 100404. https://doi.org/10.1016/j.jbef.2020.100404 doi: 10.1016/j.jbef.2020.100404

|

| [53] | UNECA (2018) East Africa the fastest growing region in Africa, with people leading longer and healthier lives - tralac trade law centre. United Nations Economic Commission for Africa. Available from: https://www.tralac.org/news/article/13721-east-africa-the-fastest-growing-region-in-africa-with-people-leading-longer-and-healthier-lives.html. |

| [54] |

Vacha L, Barunik J (2012) Co-movement of energy commodities revisited: Evidence from wavelet coherence analysis. Energy Econ 34: 241–247. https://doi.org/10.1016/j.eneco.2011.10.007 doi: 10.1016/j.eneco.2011.10.007

|

| [55] | Varangis P, Varma S, DePlaa A, et al. (2004) Exogenous shocks in low income countries: economic policy issues and the role of the international community. In: Background Paper prepared for the Report: Managing the Debt Risk of Exogenous Shocks in Low Income Countries. |

| [56] | Wearden G, Fletcher N (2016) Brexit panic wipes $2 trillion off world markets - as it happened, Business. Available from: https://www.theguardian.com/business/live/2016/jun/24/global-markets-ftse-pound-uk-leave-eu-brexit-live-updates. |

Figures(5) / Tables(6)

Lorna Katusiime. 2022: Time-Frequency connectedness between developing countries in the COVID-19 pandemic: The case of East Africa, Quantitative Finance and Economics, 6(4): 722-748. doi: 10.3934/QFE.2022032

DownLoad:

DownLoad: