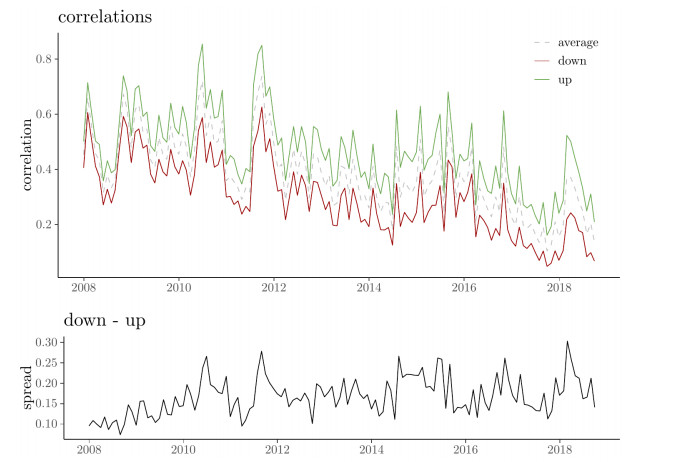

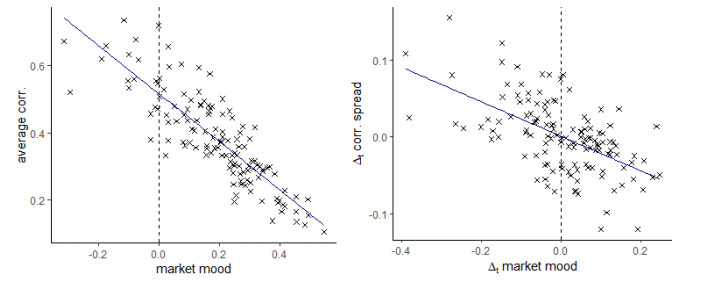

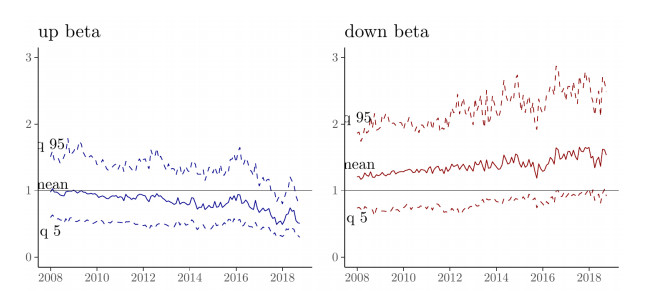

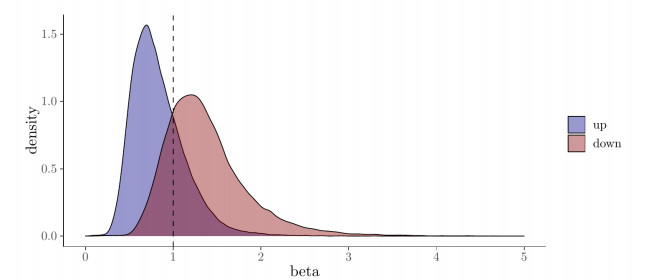

Equity returns are typically higher correlated during market downturns than during bullish times. This paper develops a novel approach how investor expectations for such correlation asymmetries can be quantified from forward-looking data. Based on option implied volatilities, it is found that the correlation asymmetry is significant, rejecting the use of the classic mono-correlation assumption. Further, the spread between expected down and up correlations is time-varying and positively dependent on the current market mood: stock diversification is more difficult when it is needed the most. Thus, the three main advantages of the proposed model are (ⅰ) the distinction between up- and down-correlations, (ⅱ) it actually captures investor expectations as traded in current market prices and (ⅲ) the immediate response to the current market outlook. Practical relevance of this paper is highlighted by the computation of expected up-/down CAPM betas.

Citation: Wolfgang Schadner. Forward looking up-/down correlations[J]. Quantitative Finance and Economics, 2021, 5(3): 471-495. doi: 10.3934/QFE.2021021

Equity returns are typically higher correlated during market downturns than during bullish times. This paper develops a novel approach how investor expectations for such correlation asymmetries can be quantified from forward-looking data. Based on option implied volatilities, it is found that the correlation asymmetry is significant, rejecting the use of the classic mono-correlation assumption. Further, the spread between expected down and up correlations is time-varying and positively dependent on the current market mood: stock diversification is more difficult when it is needed the most. Thus, the three main advantages of the proposed model are (ⅰ) the distinction between up- and down-correlations, (ⅱ) it actually captures investor expectations as traded in current market prices and (ⅲ) the immediate response to the current market outlook. Practical relevance of this paper is highlighted by the computation of expected up-/down CAPM betas.

| [1] |

Äijö J (2008) Implied volatility term structure linkages between VDAX, VSMI and VSTOXX volatility indices. Glob Fin J 18: 290-302. doi: 10.1016/j.gfj.2006.11.003

|

| [2] |

Ang A, Bekaert G (2015) International asset allocation with regime shifts. Rev Fin Stud 15: 1137-1187. doi: 10.1093/rfs/15.4.1137

|

| [3] |

Ang A, Chen J (2002) Asymmetric correlations of equity portfolios. J Fin Econ 63: 443-494. doi: 10.1016/S0304-405X(02)00068-5

|

| [4] |

Bakshi G, Kapadia N, Madan D (2003) Stock return characteristics, skew laws, and the differential pricing of individual equity options. Rev Fin Stud 16: 101-143. doi: 10.1093/rfs/16.1.0101

|

| [5] | Bali TG, Hu J, Murray S (2019) Option implied volatility, skewness, and kurtosis and the cross-section of expected stock returns. SSRN (accessed at Jul. 20, 2020). |

| [6] |

Bertero E, Mayer C (1990) Structure and performance: global interdependence of stock markets around the crash of October 1987. Eur Econ Rev 34: 1155-1180. doi: 10.1016/0014-2921(90)90073-8

|

| [7] |

Black F, Scholes M (1973) The pricing of options and corporate liabilities. J Pol Econ 81: 637-654. doi: 10.1086/260062

|

| [8] | Buss A Vilkov G (2009) Option-implied correlation and factor betas revisited. SSRN (accessed at Jun. 9, 2020). |

| [9] |

Buss A, Vilkov G (2012) Measuring equity risk with option-implied correlations. Rev Fin Stud 25: 3113- 3140. doi: 10.1093/rfs/hhs087

|

| [10] |

Campbell JY, Vuolteenaho T (2004) Bad beta, good beta. Am Econ Rev 94: 1249-1275. doi: 10.1257/0002828043052240

|

| [11] |

Cappiello L, Engle RF, Sheppard K (2006) Asymmetric dynamics in the correlations of global equity and bond returns. J Fin Econometrics 4: 537-572. doi: 10.1093/jjfinec/nbl005

|

| [12] |

Carr P, Wu L (2006) A tale of two indices. J Deriv 13: 13-29. doi: 10.3905/jod.2006.616865

|

| [13] |

Carr P, Wu L (2009) Variance risk premiums. Rev Fin Stud 22: 1311-1341. doi: 10.1093/rfs/hhn038

|

| [14] | Chong J, Pfeiffer S, Phillips MG (2011) Can dual beta filtering improve investor performance. J Pers Fin 10: 63-86. |

| [15] | Chong J, Phillips MG (2013) Measuring risk for cost of capital: the downside beta approach. J Corp Treas Man 4: 344-352. |

| [16] | Driessen J, Maenhout PJ, Vilkov G (2013) Option-implied correlations and the price of correlation risk. Adv Risk Port Man, SSRN (accessed at Jun. 8, 2020). |

| [17] |

Erb CB, Harvey CR, Viskanta TE (1994) Forecasting international equity correlations. Fin An J 50: 32- 45. doi: 10.2469/faj.v50.n6.32

|

| [18] |

Faff R (2001) A multivariate test of a dual-beta CAPM: australian evidence. Fin Rev 36: 157-174. doi: 10.1111/j.1540-6288.2001.tb00034.x

|

| [19] |

Fassas AP, Kenourgios D, Papadamou S (2020) U.S. unconventional monetary policy and risk tolerance in major currency markets. Eur J Fin, 1-15. doi: 10.1080/1351847X.2020.1775105

|

| [20] |

Fassas AP, Papadamou S (2018) Variance risk premium and equity returns. Res Int Bus Fin 46: 462-470. doi: 10.1016/j.ribaf.2018.06.003

|

| [21] |

Fassas A, Papadamou S, Philippas D (2020) Investors' risk aversion integration and quantitative easing. Rev Behav Fin 12: 170-183. doi: 10.1108/RBF-02-2019-0027

|

| [22] |

Guo G, Jacquier A, Martini C, et al. (2016) Generalized arbitrage-free SVI volatility surfaces. SIAM J Fin Math 7: 619-641. doi: 10.1137/120900320

|

| [23] |

Howton S, Peterson D (1999)A cross-sectional empirical test of a dual-state multi-factor pricing model. Fin Rev 34: 47-63. doi: 10.1111/j.1540-6288.1999.tb00462.x

|

| [24] |

Jarrow R, Rudd A (1982) Approximate option valuation for arbitrary stochastic processes. J Fin Econ 10: 347-369. doi: 10.1016/0304-405X(82)90007-1

|

| [25] |

Jeon B, Seo SW, Kim JS (2020) Uncertainty and the volatility forecasting power of option-implied volatility. J Fut Mark 40: 1109-1126. doi: 10.1002/fut.22116

|

| [26] |

Kaplanis EC (1988) Stability and forecasting of the comovement measures of international stock market returns. J Int Mon Fin 7: 63-75. doi: 10.1016/0261-5606(88)90006-X

|

| [27] |

King MA, Wadhwani S (1990) Transmission of volatility between stock markets. Rev Fin Stud 3: 5-33. doi: 10.1093/rfs/3.1.5

|

| [28] |

Kizys R, Pierdzioch C (2006) Business-cycle fluctuations and international equity correlations. Glob Fin J 17: 252-270. doi: 10.1016/j.gfj.2006.05.002

|

| [29] |

Linders D, Schoutens W (2014) A framework for robust measurement of implied correlation. J Comp App Math 271: 39-52. doi: 10.1016/j.cam.2014.03.026

|

| [30] | Longerstaey J, Spencer M (1996) Riskmetrics-technical document. Morgan Guaranty Trust Company of New York 51: 54. |

| [31] |

Longin F, Solnik B (1995) Is the correlation in international equity returns constant: 1960-1990? J Int Mon Fin 14: 3-26. doi: 10.1016/0261-5606(94)00001-H

|

| [32] |

Longin F, Solnik B (2001) Extreme correlation of international equity markets. J Fin 56: 649-676. doi: 10.1111/0022-1082.00340

|

| [33] |

Mixon S (2010) What does implied volatility skew Mmeasure? J Deriv 18: 9-25. doi: 10.3905/jod.2010.18.1.009

|

| [34] |

Numpacharoen K, Numpacharoen N (2013) Estimating realistic implied correlation matrix from option prices. J Math Fin 3: 401-406. doi: 10.4236/jmf.2013.34041

|

| [35] |

Pettengill GN, Sundaram S, Mathur I (1995) The conditional relation between beta and returns. J Fin Quant An 30: 101-116. doi: 10.2307/2331255

|

| [36] |

Pettengill G, Sundaram S, Mathur I (2002) Payment for risk: constant beta vs. dual-beta models. Fin Rev 37: 123-135. doi: 10.1111/1540-6288.00008

|

| [37] |

Ramchand L, Susmel R (1998) Volatility and cross correlation across major stock markets. J Emp Fin 5: 397-416. doi: 10.1016/S0927-5398(98)00003-6

|

| [38] |

Ratner M (1992) Portfolio diversification and the inter-temporal stability of international stock indices. Glob Fin J 3: 67-77. doi: 10.1016/1044-0283(92)90005-6

|

| [39] |

Rehman MU (2017) Dynamics of co-movements among implied volatility, policy uncertainty and market performance. Glob Bus Rev 18: 1478-1487. doi: 10.1177/0972150917713060

|

| [40] |

Sancetta A, Satchell SE (2007) Changing correlation and equity portfolio diversification failure for linear factor models during market declines. App Math Fin 14: 227-242. doi: 10.1080/13504860600858279

|

| [41] |

Schadner W (2020a) An idea of risk neutral momentum and market fear. Fin Res Let 37: 101347. doi: 10.1016/j.frl.2019.101347

|

| [42] | Schadner W (2020b) Ex-ante risk factors and required structures of the implied correlation matrix. Fin Res Let, 101855. |

| [43] |

Schmalensee R, Trippi RR (1978) Common stock volatility expectations implied by option premia. J Fin 33: 129-147. doi: 10.1111/j.1540-6261.1978.tb03394.x

|

| [44] |

Schneider P, Wagner C, Zechner J (2020) Low-risk anomalies? J Fin 75: 2673-2718. doi: 10.1111/jofi.12910

|

| [45] |

Shaikh I (2019) On the relationship between economic policy uncertainty and the implied volatility index. Sustain 11: 1628. doi: 10.3390/su11061628

|

| [46] | Sharpe WF (1964) Capital asset prices: a theory of market equilibrium under conditions of risk. J Fin 19: 425-442. |

| [47] |

Skintzi V, Refenes APN (2005) Implied correlation index: a new measure of diversification. J Fut Mark 25: 171-197. doi: 10.1002/fut.20137

|

| [48] |

Walter CA, Lopez JA (2000) Is implied correlation worth calculating? J Deriv 7: 65-81. doi: 10.3905/jod.2000.319125

|

| [49] |

Zhang JE, Xiang Y (2008) The implied volatility smirk. Quant Fin 8: 263-284. doi: 10.1080/14697680601173444

|

Figures(10) / Tables(4)

Wolfgang Schadner. Forward looking up-/down correlations[J]. Quantitative Finance and Economics, 2021, 5(3): 471-495. doi: 10.3934/QFE.2021021

DownLoad:

DownLoad: