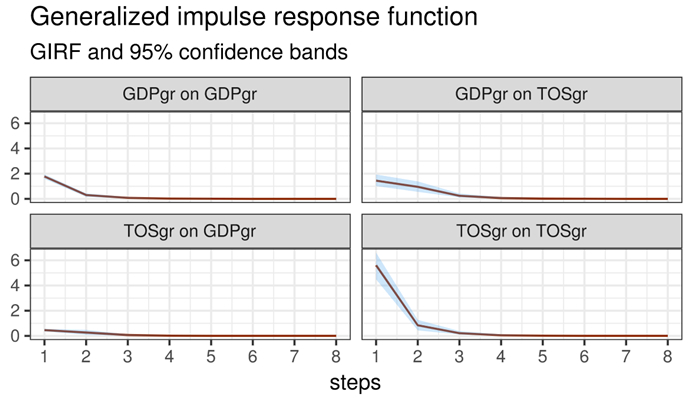

This paper focuses on the Italian economy and investigates the causal nexus between economic growth, tourism development and labor market dynamics. We performed a two-step analysis. In the first step, we evaluate whether tourism stimulates Italian economic growth or if it is the economic growth that promotes tourism expansion. To get the goal, we use panel data from 1997 to 2019 concerning the GDP and overnight stays in each Italian region. We performed the Granger causality test on the whole panel and analyzed a panelvar model. In the second step, after having established the relationship between the two variables of interest, we extended our analysis to investigate—throughout the estimate of the employment intensity of growth and the impact of GDP growth on employment, at both aggregate and disaggregate level. The main findings of our analysis are as follows: a) the existence of a unidirectional causality going from economic growth to tourism development (i.e., validation of economic-driven tourism growth hypothesis), and b) a significant estimated magnitude of the (average) employment intensity of growth.

Citation: Giorgio Colacchio, Anna Serena Vergori. GDP growth rate, tourism expansion and labor market dynamics: Applied research focused on the Italian economy[J]. National Accounting Review, 2022, 4(3): 310-328. doi: 10.3934/NAR.2022018

This paper focuses on the Italian economy and investigates the causal nexus between economic growth, tourism development and labor market dynamics. We performed a two-step analysis. In the first step, we evaluate whether tourism stimulates Italian economic growth or if it is the economic growth that promotes tourism expansion. To get the goal, we use panel data from 1997 to 2019 concerning the GDP and overnight stays in each Italian region. We performed the Granger causality test on the whole panel and analyzed a panelvar model. In the second step, after having established the relationship between the two variables of interest, we extended our analysis to investigate—throughout the estimate of the employment intensity of growth and the impact of GDP growth on employment, at both aggregate and disaggregate level. The main findings of our analysis are as follows: a) the existence of a unidirectional causality going from economic growth to tourism development (i.e., validation of economic-driven tourism growth hypothesis), and b) a significant estimated magnitude of the (average) employment intensity of growth.

| [1] | Abonazel MR (2016) Bias correction methods for dynamic panel data models with fixed effects. Available from: https://mpra.ub.uni-muenchen.de/70628/ |

| [2] | Abrigo MRM, Love I (2016) Estimation of Panel Vector Autoregression in Stata. 16: 778–804. https://doi.org/10.1177/1536867X1601600314 |

| [3] |

Antonakakis N, Dragouni M, Eeckels B (2019) The tourism and economic growth enigma: examining an ambiguous relationship through multiple prisms. J Travel Res 58: 3–24. https://doi.org/10.1177/0047287517744671 doi: 10.1177/0047287517744671

|

| [4] |

Arellano M, Bond S (1991) Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev Econ Stud 58: 277–297. https://doi.org/10.2307/2297968 doi: 10.2307/2297968

|

| [5] | Arthur BW (1994) Increasing returns and Path Dependence in the Economy. University of Michigan Press. https://doi.org/10.3998/mpub.10029 |

| [6] |

Aslan A (2013) Tourism development and economic growth in the Mediterranean countries: evidence from panel Granger causality tests. Curr Issues Tour 17: 363–372. https://doi.org/10.1080/13683500.2013.768607 doi: 10.1080/13683500.2013.768607

|

| [7] |

Balaguer J, Cantavella-Jordà M (2002) Tourism as a long-run economic growth factor: the Spanish case. Appl Econ 34: 877–884. https://doi.org/10.1080/00036840110058923 doi: 10.1080/00036840110058923

|

| [8] |

Baum CF, Schaffer ME, Stillman S (2003) Instrumental variables and GMM: Estimation and testing. Stata J 3: 1–31. https://doi.org/10.1177/1536867X0300300101 doi: 10.1177/1536867X0300300101

|

| [9] | Boltho A, Glyn A (1995) Can Macroeconomic Policies Raise Employment? Int Labour Rev 134: 451–470. |

| [10] |

Breitung J, Das S (2005) Panel unit root tests under cross-sectional dependence. Stat Neerl 59: 414–433. https://doi.org/10.1111/j.1467-9574.2005.00299.x doi: 10.1111/j.1467-9574.2005.00299.x

|

| [11] |

Brida J, Cortes-Jimenez I, Pulina M (2016) Has the tourism-led growth hypothesis been validated? A literature review. Curr Issues Tour 19: 394–430. https://doi.org/10.1080/13683500.2013.868414 doi: 10.1080/13683500.2013.868414

|

| [12] | Busetti F, Cova P (2013) L'impatto macroeconomico della crisi del debito sovrano: un'analisi controfattuale per l'economia italiana. http://dx.doi.org/10.2139/ssrn.2405442 |

| [13] |

Cardenas-Garcia PJ, Sanchez-Rivero M, Pulido-Fernandez JI (2015) Does Tourism Growth Influence Economic Development? J Travel Res 54: 206–221. https://doi.org/10.1177/0047287513514297 doi: 10.1177/0047287513514297

|

| [14] |

Centinaio A, Comerio N, Pacicco F (2022) Arrivederci! An Analysis of Tourism Impact in the Italian Provinces. Int J Hosp Tour Adm. https://doi.org/10.1080/15256480.2021.2025187 doi: 10.1080/15256480.2021.2025187

|

| [15] |

Chen CF, Chiou-Wei SZ (2009) Tourism Expansion, Tourism Uncertainty and Economic Growth: New Evidence from Taiwan and Korea. Tourism Manage 30: 812–818. https://doi.org/10.1016/j.tourman.2008.12.013 doi: 10.1016/j.tourman.2008.12.013

|

| [16] |

Chirilă V, Butnaru GI, Chirilă C (2020) Spillover Index Approach in Investigating the Linkage between International Tourism and Economic Growth in Central and Eastern European Countries. Sustainability 12: 1–36. https://doi.org/10.3390/su12187604 doi: 10.3390/su12187604

|

| [17] |

Chiu YB, Yeh LT (2017) The threshold effects of the tourism-led growth hypothesis: evidence from a cross-sectional model. J Travel Res 56: 625–637. https://doi.org/10.1177/0047287516650938 doi: 10.1177/0047287516650938

|

| [18] |

Choi I (2001) Unit root tests for panel data. J Int Money Financ 20: 249–272. https://doi.org/10.1016/S0261-5606(00)00048-6 doi: 10.1016/S0261-5606(00)00048-6

|

| [19] |

Cortés-Jiménez J (2008) Which type of tourism matters to the regional economic growth? The cases of Spain and Italy. Int J Tour Res 10: 127–139. https://doi.org/10.1002/jtr.646 doi: 10.1002/jtr.646

|

| [20] |

Cortes-Jimenez J, Pulin M (2010) Inbound tourism and long-run economic growth. Curr Issues Tour 13: 61–74. https://doi.org/10.1080/13683500802684411 doi: 10.1080/13683500802684411

|

| [21] | Crivelli E, Furceri D, Toujas-Bernaté J (2012) Can policies affect employment intensity of growth? A cross-country analysis. Available from: https://www.imf.org/external/pubs/ft/wp/2012/wp12218.pdf. |

| [22] |

Ditzen J (2018) Estimating dynamic common correlated effects in Stata. Stata J 18: 585–617. https://doi.org/10.1177/1536867X1801800306 doi: 10.1177/1536867X1801800306

|

| [23] |

Dogru T, Bulut U (2018) Is tourism an engine for economic recovery? Theory and empirical evidence. Tour Manag 67: 425–434. https://doi.org/10.1016/j.tourman.2017.06.014 doi: 10.1016/j.tourman.2017.06.014

|

| [24] |

Dumitrescu EI, Hurlin C (2012) Testing for Granger non-causality in heterogeneous panels. Econ Model 29: 1450–1460. https://doi.org/10.1016/j.econmod.2012.02.014 doi: 10.1016/j.econmod.2012.02.014

|

| [25] | ECB (2016) The employment-GDP relationship since the crisis. Available from: https://www.ecb.europa.eu/pub/pdf/other/eb201606_article01.en.pdf. |

| [26] | Eugenio-Martin JL, Morales NM, Scarpa R (2004) Tourism and Economic Growth in Latin American Countries: A Panel Data Approach. Available from: http://ssrn.com/abstract=504482. |

| [27] |

Fonseca N, Sanchez-Rivero M (2019) Publication bias and genuine effects: the case of Granger causality between tourism and income. Curr Issues Tour 23: 1084–1108 https://doi.org/10.1080/13683500.2019.1585419 doi: 10.1080/13683500.2019.1585419

|

| [28] |

Hadri K (2000) Testing for stationarity in heterogeneous panel data. Economet J 3: 148–161. https://doi.org/10.1111/1368-423X.00043 doi: 10.1111/1368-423X.00043

|

| [29] |

Hoechle D (2007) Robust standard errors for panel regressions with cross-sectional dependence. Stata J 7: 281–312. https://doi.org/10.1177/1536867X0700700301 doi: 10.1177/1536867X0700700301

|

| [30] |

Hwang J, Sun Y (2018) Should we go one-step further? An accurate comparison of one-step and two-step procedures in a generalized method of moments framework. J Econom 207: 381–405. https://doi.org/10.1016/j.jeconom.2018.07.006 doi: 10.1016/j.jeconom.2018.07.006

|

| [31] | Italian Government (2021) Recovery and resilience Plan. Available from: https://www.governo.it/sites/governo.it/files/PNRR.pdf. |

| [32] |

Ivanov SH, Webster C (2013) Tourism's contribution to economic growth: a global analysis for the first decade of the millennium. Tourism Econ 19: 477–508. doi: 10.5367/te.2013.0211

|

| [33] |

Labra R, Torrecillas C (2018) Estimating dynamic Panel data. A practicalapproach to perform long panels. Revista Colombiana de Estadística 41: 31–52. https://doi.org/10.15446/rce.v41n1.61885 doi: 10.15446/rce.v41n1.61885

|

| [34] |

Levin A, Lin CF, Chu CSJ (2002) Unit root test in panel data: asymptotic and finite sample properties. J Econom 108: 1–24. https://doi.org/10.1016/S0304-4076(01)00098-7 doi: 10.1016/S0304-4076(01)00098-7

|

| [35] |

Massidda C, Mattana P (2012) A SVECM Analysis of the relationship between international tourism arrivals, GDP and trade in Italy. J Travel Res 52: 93–105. https://doi.org/10.1177/0047287512457262 doi: 10.1177/0047287512457262

|

| [36] | Mehrhoff J (2009) A solution to the problem of too many instruments in dynamic panel data GMM. http://dx.doi.org/10.2139/ssrn.2785360 |

| [37] |

Pablo-Romero M, Molina J (2013) Tourism and economic growth: A review of empirical literature. Tour Manag Perspect 8: 28–41. https://doi.org/10.1016/j.tmp.2013.05.006 doi: 10.1016/j.tmp.2013.05.006

|

| [38] | Padalino S, Vivarelli M (1997) The Employment Intensity of Economic Growth in the G-7 Countries. Int Labour Rev 136: 191–213. |

| [39] |

Pesaran H (2003) A Simple Panel Unit Root Test in the Presence of Cross Section Dependence. J Appl Economet 22: 265–312. https://doi.org/10.1002/jae.951 doi: 10.1002/jae.951

|

| [40] |

Proença S, Soukiazis E (2008) Tourism as an economic growth factor: a case study for Southern European countries. Tourism Econ 14: 791–806. https://doi.org/10.5367/000000008786440175 doi: 10.5367/000000008786440175

|

| [41] |

Roodman D (2009) How to do xtabond2: An introduction to difference and system GMM. Stata J 9: 86–136. https://doi.org/10.1177/1536867X0900900106 doi: 10.1177/1536867X0900900106

|

| [42] |

Sharpley R (2022) Tourism and (sustainable) development: Revisiting the theoretical divide. Tourism in Development: reflective essays, 13–24. https://doi.org/10.1079/9781789242812.000 doi: 10.1079/9781789242812.000

|

| [43] |

Sigmund M, Ferstl R (2019) Panel vector Autoregression in R with the packagepanelvar. Q Rev Econ Financ 80: 693–720. https://doi.org/10.1016/j.qref.2019.01.001 doi: 10.1016/j.qref.2019.01.001

|

| [44] |

Shahbaz M, Ferrer R, Shahzad SJH, et al. (2017) Is the tourism–economic growth nexus time-varying? Bootstrap rolling-window causality analysis for the top 10 tourist destinations. Appl Econ. https://doi.org/10.1080/00036846.2017.1406655 doi: 10.1080/00036846.2017.1406655

|

| [45] |

Shahzad SJH, Shahbaz M, Ferrer R, et al. (2017) Tourism-led growth hypothesis in the top ten tourist destinations: new evidence using the quantile-on-quantile approach. Tourism Manage 60: 223–232. https://doi.org/10.1016/j.tourman.2016.12.006 doi: 10.1016/j.tourman.2016.12.006

|

| [46] | SVIMEZ (2019) Rapporto SVIMEZ 2019, Rome. |

| [47] |

Tugcu CT (2014) Tourism and economic growth nexus revisited: A panel causality analysis for the case of the Mediterranean region. Tourism Manage 42: 207–212. https://doi.org/10.1016/j.tourman.2013.12.007 doi: 10.1016/j.tourman.2013.12.007

|

| [48] |

Vergori AS (2017) Patterns of seasonality and tourism demand forecasting. Tourism Econ 23: 1011–1027. https://doi.org/10.1016/j.tourman.2020.104263 doi: 10.1177/1354816616656418

|

| [49] |

Zellner A (1962) An efficient method of estimating seemingly unrelated regressions and tests for aggregation bias. J Am Stat Assoc 57: 348–368. doi: 10.1080/01621459.1962.10480664

|

Figures(1) / Tables(7)

Giorgio Colacchio, Anna Serena Vergori. GDP growth rate, tourism expansion and labor market dynamics: Applied research focused on the Italian economy[J]. National Accounting Review, 2022, 4(3): 310-328. doi: 10.3934/NAR.2022018

DownLoad:

DownLoad: