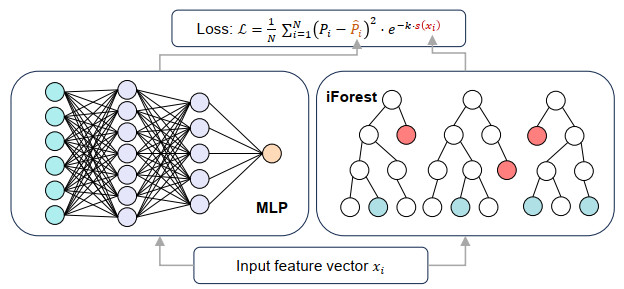

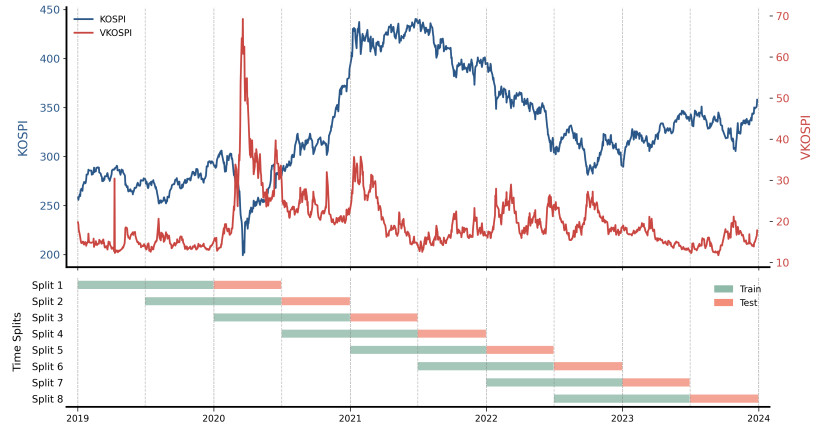

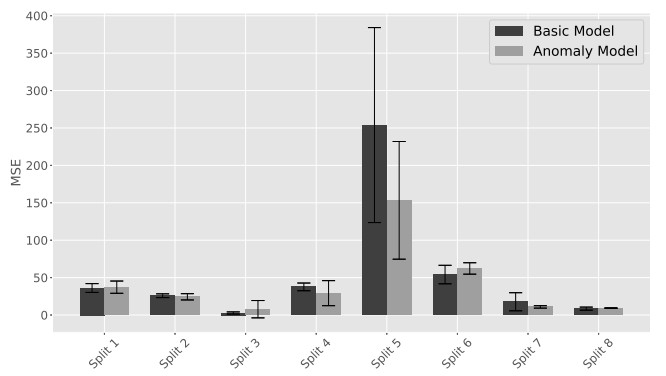

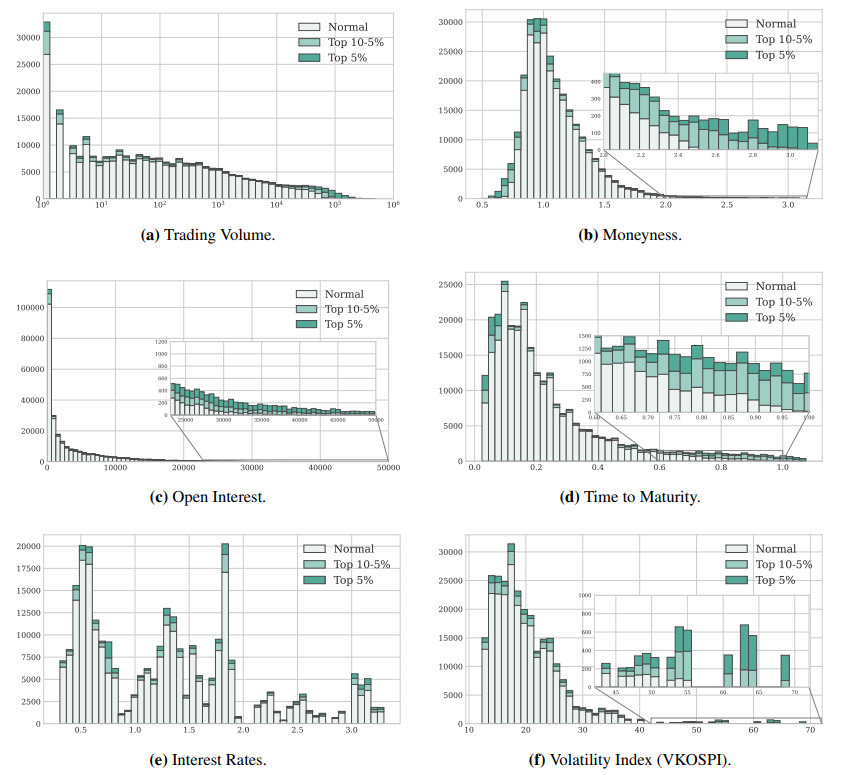

We propose a neural-network variant integrating the Isolation Forest anomaly detection algorithm into its loss function. By incorporating anomaly scores as weights—effectively treating them as inverse measures of data reliability—the model suppresses outlier impact, yielding modest but consistent accuracy gains. Using KOSPI 200 option price data from 2019 to 2023, our experiments show that this anomaly-based approach enhances predictive accuracy by an average of 4.77% on the test set compared to a baseline neural network. Moreover, performance gains are generally observed across various market conditions, including different moneyness states, trading volumes, and time to maturity. Analysis of the identified anomalies reveals that trading volume and time to maturity are key factors strongly associated with irregularities in option data. Option moneyness also contributes to these irregularity patterns, particularly with other market conditions or at extreme levels. In contrast, interest rates show a less direct impact on anomaly scores in our dataset. These findings are broadly consistent with established market regularities, suggesting the anomaly detector's effectiveness in capturing characteristics of market inefficiencies or challenging pricing conditions. Overall, the proposed methodology contributes to the development of a more robust option pricing framework by better reflecting actual market dynamics. It shows potential during periods of heightened volatility, offering useful insights for further academic and practical applications.

Citation: Jihong Park, Jeonggyu Huh, Jaegi Jeon. Reliable option pricing through deep learning: An anomaly score-based approach[J]. Networks and Heterogeneous Media, 2025, 20(3): 987-1009. doi: 10.3934/nhm.2025043

We propose a neural-network variant integrating the Isolation Forest anomaly detection algorithm into its loss function. By incorporating anomaly scores as weights—effectively treating them as inverse measures of data reliability—the model suppresses outlier impact, yielding modest but consistent accuracy gains. Using KOSPI 200 option price data from 2019 to 2023, our experiments show that this anomaly-based approach enhances predictive accuracy by an average of 4.77% on the test set compared to a baseline neural network. Moreover, performance gains are generally observed across various market conditions, including different moneyness states, trading volumes, and time to maturity. Analysis of the identified anomalies reveals that trading volume and time to maturity are key factors strongly associated with irregularities in option data. Option moneyness also contributes to these irregularity patterns, particularly with other market conditions or at extreme levels. In contrast, interest rates show a less direct impact on anomaly scores in our dataset. These findings are broadly consistent with established market regularities, suggesting the anomaly detector's effectiveness in capturing characteristics of market inefficiencies or challenging pricing conditions. Overall, the proposed methodology contributes to the development of a more robust option pricing framework by better reflecting actual market dynamics. It shows potential during periods of heightened volatility, offering useful insights for further academic and practical applications.

| [1] |

F. Black, M. Scholes, The pricing of options and corporate liabilities, J. Polit. Econ., 81 (1973), 637–654. https://doi.org/10.1086/260062 doi: 10.1086/260062

|

| [2] |

R. C. Merton, Theory of rational option pricing, Bell J. Econ. Manage. Sci., 4 (1973), 141–183. https://doi.org/10.2307/3003143 doi: 10.2307/3003143

|

| [3] |

R. Cont, Empirical properties of asset returns: Stylized facts and statistical issues, Quant. Finance, 1 (2001), 223–236. https://doi.org/10.1080/713665670 doi: 10.1080/713665670

|

| [4] | J. C. Hull, Options, futures, and other derivatives, 5th ed., Pearson Education, 2003. |

| [5] |

M. Malliaris, L. A. Salchenberger, Neural network model for estimating option prices, Appl. Intell., 3 (1993), 193–206. https://doi.org/10.1007/BF00871937 doi: 10.1007/BF00871937

|

| [6] |

J. M. Hutchinson, A. W. Lo, T. A. Poggio, Nonparametric approach to pricing and hedging derivative securities via learning networks, J. Finance, 49 (1994), 851–889. https://doi.org/10.1111/j.1540-6261.1994.tb00081.x doi: 10.1111/j.1540-6261.1994.tb00081.x

|

| [7] |

A. Sharma, C. K. Verma, P. Singh, Enhancing option pricing accuracy in the Indian market: A CNN-BiLSTM approach, Comput. Econ., 65 (2025), 3751–3778. https://doi.org/10.1007/s10614-024-10689-z doi: 10.1007/s10614-024-10689-z

|

| [8] |

C. Quek, M. Pasquier, N. Kumar, A novel recurrent neural network-based prediction system for option trading and hedging, Appl. Intell., 29 (2008), 138–151. https://doi.org/10.1007/s10489-007-0052-4 doi: 10.1007/s10489-007-0052-4

|

| [9] |

J. Ruf, W. Wang, Neural networks for option pricing and hedging: A literature review, J. Comput. Finance, 24 (2020), 1–46. https://doi.org/10.21314/JCF.2020.390 doi: 10.21314/JCF.2020.390

|

| [10] |

J. Huh, Pricing options with exponential Lévy neural network, Expert Syst. Appl., 127 (2019), 128–140. https://doi.org/10.1016/j.eswa.2019.03.008 doi: 10.1016/j.eswa.2019.03.008

|

| [11] |

Y. Aït-Sahalia, J. Yu, High frequency market microstructure noise estimates and liquidity measures, Ann. Appl. Stat., 3 (2009), 422–457. https://doi.org/10.1214/08-AOAS200 doi: 10.1214/08-AOAS200

|

| [12] |

A. Madhavan, Market microstructure: A survey, J. Financ. Mark., 3 (2000), 205–258. https://doi.org/10.1016/S1386-4181(00)00007-0 doi: 10.1016/S1386-4181(00)00007-0

|

| [13] | B. Zong, Q. Song, M. R. Min, W. Cheng, C. Lumezanu, D. Cho, et al. Deep autoencoding Gaussian mixture model for unsupervised anomaly detection, In: Proc. Int. Conf. Learn. Represent. (ICLR), (2018). Available from: https://openreview.net/forum?id=BJJLHbb0-. |

| [14] | F. T. Liu, K. M. Ting, Z. H. Zhou, Isolation forest, In: 2008 Eighth IEEE International Conference on Data Mining, Pisa, Italy, (2008), 413–422. https://doi.org/10.1109/ICDM.2008.17 |

| [15] |

K. Golmohammadi, O. R. Zaiane, Time series contextual anomaly detection for detecting market manipulation in stock market, Expert Syst. Appl., 42 (2015), 3635–3644. https://doi.org/10.1109/DSAA.2015.7344856 doi: 10.1109/DSAA.2015.7344856

|

| [16] | M. Ren, W. Zeng, B. Yang, R. Urtasun, Learning to reweight examples for robust deep learning, arXiv preprint, arXiv: 1803.09050 (2018). Available from: https://arXiv.org/abs/1803.09050. |

| [17] | B. Han, Q. Yao, X. Yu, G. Niu, M. Xu, W. H. Hu, et al. Co-teaching: Robust training of deep neural networks with extremely noisy labels, Adv. Neural Inf. Process. Syst., 31 (2018), 8527–8537. Available from: https://proceedings.neurips.cc/paper/2018/hash/a19744e268754fb0148b017647355b7b-Abstract.html. |

| [18] |

E. F. Fama, Efficient capital markets: A review of theory and empirical work, J. Finance, 25 (1970), 383–417. https://doi.org/10.2307/2325486 doi: 10.2307/2325486

|

| [19] |

G. Bakshi, N. Kapadia, D. Madan, Stock return characteristics, skew laws, and the differential pricing of individual equity options, Rev. Financ. Stud., 16 (2003), 101–143. https://doi.org/10.1093/rfs/16.1.101 doi: 10.1093/rfs/16.1.101

|

| [20] | V. Nair, G. E. Hinton, Rectified linear units improve restricted Boltzmann machines, In: ICML'10: Proceedings of the 27th International Conference on International Conference on Machine Learning, (2010), 807–814. Available from: https://dl.acm.org/doi/10.5555/3104322.3104425. |

| [21] | K. He, X. Zhang, S. Ren, J. Sun, Delving deep into rectifiers: Surpassing human-level performance on ImageNet classification, In: 2015 IEEE International Conference on Computer Vision (ICCV), Santiago, Chile, (2015), 1026–1034. https://doi.org/10.1109/ICCV.2015.123 |

| [22] | D. P. Kingma, J. Ba, Adam: A method for stochastic optimization, arXiv preprint, arXiv: 1412.6980 (2014). Available from: https://arXiv.org/abs/1412.6980. |

Figures(7) / Tables(5)

Jihong Park, Jeonggyu Huh, Jaegi Jeon. Reliable option pricing through deep learning: An anomaly score-based approach[J]. Networks and Heterogeneous Media, 2025, 20(3): 987-1009. doi: 10.3934/nhm.2025043

DownLoad:

DownLoad: