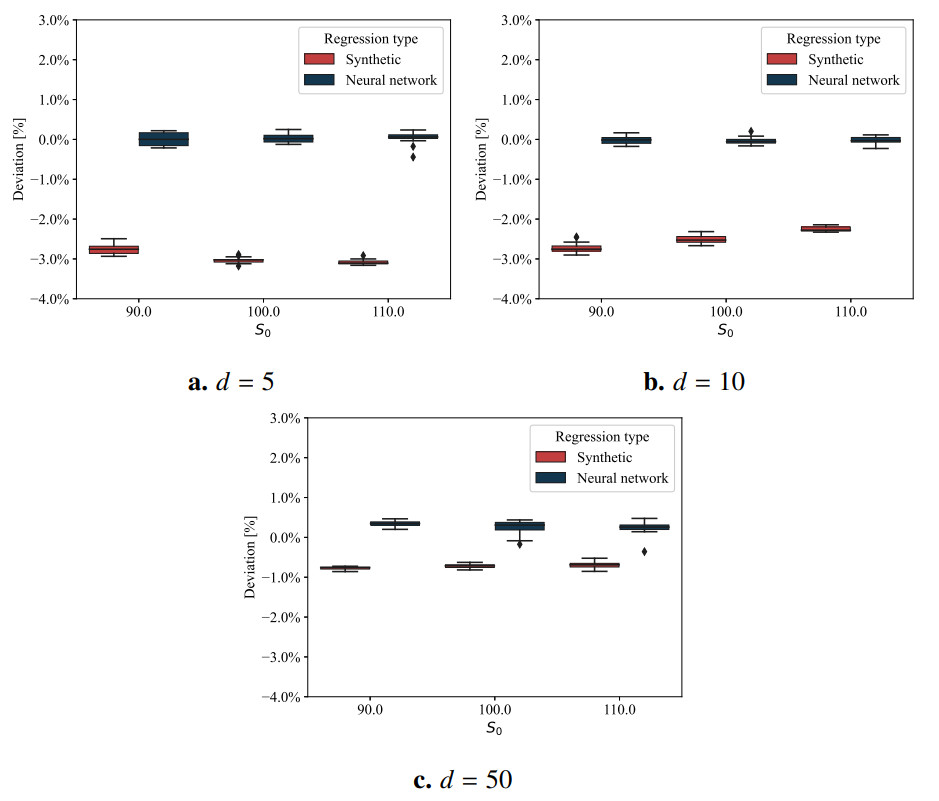

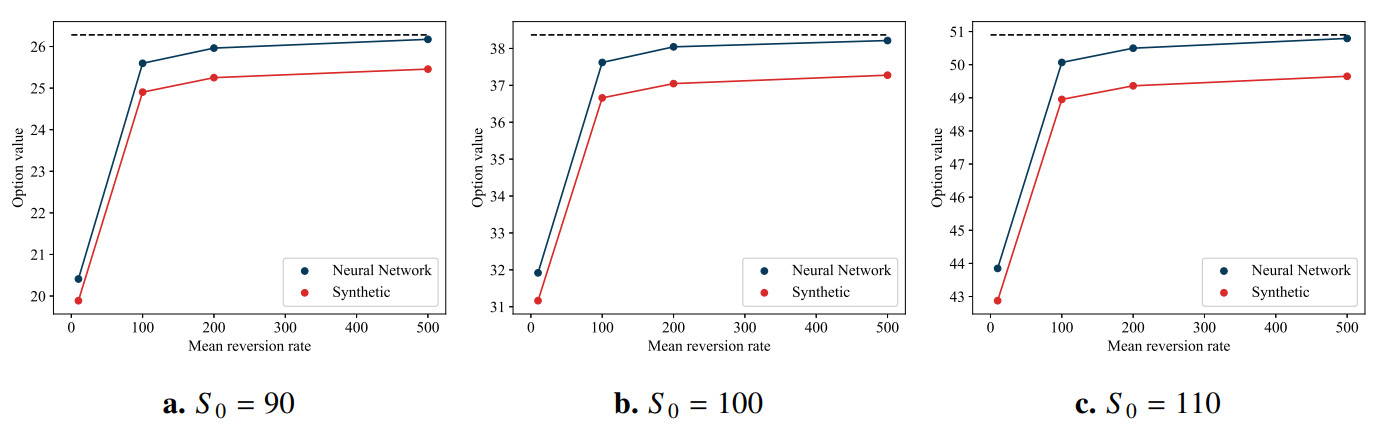

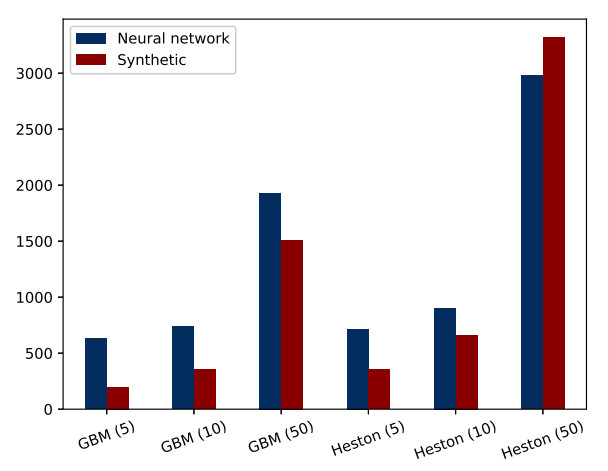

Pricing high-dimensional basket options poses significant challenges, especially when dealing with nonlinear payoffs. Previous research has demonstrated the effectiveness of neural networks in pricing Bermudan basket call options, particularly under the assumption that the underlying assets follow geometric Brownian motion (GBM). Building on these, the contribution of this study is twofold. First, we extended the scope of options to include both call and put options, as well as payoffs based on the maximum and minimum of the underlying assets. Second, and more importantly, we addressed the practical relevance of market conditions by modeling the underlying assets using a high-dimensional Heston stochastic volatility model with a full correlation structure. Using a least-squares Monte Carlo approach, we approximated the continuation value of the options across a large number of underlying assets using a shallow neural network. We demonstrated that our model yields accurate results in low-dimensional Heston settings and high-dimensional GBM settings, aligning with existing literature and providing confidence in its validity. While high-dimensional pricing has been explored under GBM, our contribution lies in extending this capability to the Heston model, for which we presented numerical experiments involving up to 50 assets, a setting that, to the best of our knowledge, has not been previously studied.

Citation: Bjørn André Aaslund, Johannes Berge, Ying Ni, Rita Pimentel. Neural network-based pricing of high-dimensional Bermudan basket options under stochastic volatility[J]. Networks and Heterogeneous Media, 2025, 20(3): 759-781. doi: 10.3934/nhm.2025032

Pricing high-dimensional basket options poses significant challenges, especially when dealing with nonlinear payoffs. Previous research has demonstrated the effectiveness of neural networks in pricing Bermudan basket call options, particularly under the assumption that the underlying assets follow geometric Brownian motion (GBM). Building on these, the contribution of this study is twofold. First, we extended the scope of options to include both call and put options, as well as payoffs based on the maximum and minimum of the underlying assets. Second, and more importantly, we addressed the practical relevance of market conditions by modeling the underlying assets using a high-dimensional Heston stochastic volatility model with a full correlation structure. Using a least-squares Monte Carlo approach, we approximated the continuation value of the options across a large number of underlying assets using a shallow neural network. We demonstrated that our model yields accurate results in low-dimensional Heston settings and high-dimensional GBM settings, aligning with existing literature and providing confidence in its validity. While high-dimensional pricing has been explored under GBM, our contribution lies in extending this capability to the Heston model, for which we presented numerical experiments involving up to 50 assets, a setting that, to the best of our knowledge, has not been previously studied.

| [1] | J. C. Hull, Options, Futures and Other Derivatives, Pearson Education Limited, 2021. |

| [2] | J. A. Tilley, Valuing American options in a path simulation model, Trans. Soc. Actuaries, 45 (1993), 499–519. |

| [3] |

M. Broadie, P. Glasserman, Pricing American-style securities using simulation, J. Econ. Dyn. Control, 21 (1997), 1323–1352. https://doi.org/10.1016/S0165-1889(97)00029-8 doi: 10.1016/S0165-1889(97)00029-8

|

| [4] |

J. F. Carriere, Valuation of the early-exercise price for options using simulations and nonparametric regression, Insur. Math. Econ., 19 (1996), 19–30. https://doi.org/10.1016/S0167-6687(96)00004-2 doi: 10.1016/S0167-6687(96)00004-2

|

| [5] |

J. N. Tsitsiklis, B. V. Roy, Optimal stopping of Markov processes: Hilbert space theory, approximation algorithms, and an application to pricing high-dimensional financial derivatives, IEEE Trans. Autom. Control, 44 (1999), 1840–1851. https://doi.org/10.1109/9.793723 doi: 10.1109/9.793723

|

| [6] |

F. Longstaff, E. Schwartz, Valuing American options by simulation: A simple least-squares approach, Rev. Financ. Stud., 14 (2001), 113–147. https://doi.org/10.1093/rfs/14.1.113 doi: 10.1093/rfs/14.1.113

|

| [7] | K. Judd, Numerical Methods in Economics, 1st edition, The MIT Press, 1 (1998). |

| [8] | J. A. Picazo, American Option Pricing: A Classification–Monte Carlo (CMC) Approach, in Monte Carlo and Quasi-Monte Carlo Methods 2000, (eds., K. T. Fang, H. Niederreiter, and F. J. Hickernell), Springer Berlin Heidelberg, Berlin, Heidelberg, 2002,422–433. |

| [9] |

A. Ibanez, F. Zapatero, Monte Carlo valuation of American options through computation of the optimal exercise frontier, J. Financ. Quant. Anal., 39 (2004), 253–275. https://doi.org/10.1017/S0022109000003069 doi: 10.1017/S0022109000003069

|

| [10] | L. Stentoft, Assessing the least squares Monte-Carlo approach to American option valuation, Rev. Deriv. Res., 7 (2004), 129–168. |

| [11] |

X. Jin, H. H. Tan, J. Sun, A state-space partitioning method for pricing high-dimensional American-style options, Math. Finance, 17 (2007), 399–426. https://doi.org/10.1111/j.1467-9965.2007.00309.x doi: 10.1111/j.1467-9965.2007.00309.x

|

| [12] |

C. F. Ivașcu, Option pricing using machine learning, Expert Syst. Appl., 163 (2021), 113799. https://doi.org/10.1016/j.eswa.2020.113799 doi: 10.1016/j.eswa.2020.113799

|

| [13] | J. Ruf, W. Wang, Neural networks for option pricing and hedging: A literature review, preprint, arXiv: 1911.05620. |

| [14] |

M. Kohler, A. Krzyżak, N. Todorovic, Pricing of high-dimensional American options by neural networks, Math. Finance, 20 (2010), 383–410. https://doi.org/10.1111/j.1467-9965.2010.00404.x doi: 10.1111/j.1467-9965.2010.00404.x

|

| [15] | M. B. Haugh, L. Kogan, Pricing American options: A duality approach, Oper. Res., 52 (2004), 258–270. https://doi.org/10.1287/opre.1030.0070 |

| [16] | S. Becker, P. Cheridito, A. Jentzen, Deep optimal stopping, J. Mach. Learn. Res., 20 (2019), 1–25. |

| [17] |

S. Becker, P. Cheridito, A. Jentzen, Pricing and hedging American-style options with deep learning, J. Risk Financ. Manage., 13 (2020), 158. https://doi.org/10.3390/jrfm13070158 doi: 10.3390/jrfm13070158

|

| [18] |

B. Lapeyre, J. Lelong, Neural network regression for Bermudan option pricing, Monte Carlo Method. Appl., 27 (2021), 227–247. https://doi.org/10.1515/mcma-2021-2091 doi: 10.1515/mcma-2021-2091

|

| [19] |

J. Liang, Z. Xu, P. Li, Deep learning-based least squares forward-backward stochastic differential equation solver for high-dimensional derivative pricing, Quant. Finance, 21 (2021), 1309–1323. https://doi.org/10.1080/14697688.2021.1881149 doi: 10.1080/14697688.2021.1881149

|

| [20] |

Y. Chen, J. W. Wan, Deep neural network framework based on backward stochastic differential equations for pricing and hedging American options in high dimensions, Quant. Finance, 21 (2021), 45–67. https://doi.org/10.1080/14697688.2020.1788219 doi: 10.1080/14697688.2020.1788219

|

| [21] |

H. G. Kim, J. Huh, Deep learning of optimal exercise boundaries for American options, Int. J. Comput. Math., 102 (2025), 595–622. https://doi.org/10.1080/00207160.2024.2442585 doi: 10.1080/00207160.2024.2442585

|

| [22] | R. Rebonato, Volatility and Correlation: The Perfect Hedger and the Fox, John Wiley & Sons, 2005. |

| [23] |

S. L. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Rev. Financ. Stud., 6 (1993), 327–343. https://doi.org/10.1093/rfs/6.2.327 doi: 10.1093/rfs/6.2.327

|

| [24] |

M. Broadie, M. Cao, Improved lower and upper bound algorithms for pricing American options by simulation, Quant. Finance, 8 (2008), 845–861. https://doi.org/10.1080/14697680701763086 doi: 10.1080/14697680701763086

|

| [25] |

D. Farahany, K. R. Jackson, S. Jaimungal, Mixing LSMC and PDE methods to price Bermudan options, SIAM J. Financ. Math., 11 (2020), 201–239. https://doi.org/10.1137/19M1249035 doi: 10.1137/19M1249035

|

| [26] | Y. Hilpisch, Python for Finance: Master Data-Driven Finance, 2nd edition, O'Reilly Media, 2018. |

| [27] |

R. Lord, R. Koekkoek, D. V. Dijk, A comparison of biased simulation schemes for stochastic volatility models, Quant. Finance, 10 (2010), 177–194. https://doi.org/10.1080/14697680802392496 doi: 10.1080/14697680802392496

|

| [28] | P. Glasserman, Monte Carlo Methods in Financial Engineering, Springer, 53 (2004). |

| [29] |

X. J. He, S. D. Huang, S. Lin, A closed-form solution for pricing European-style options under the Heston model with credit and liquidity risks, Commun. Nonlinear Sci. Numer. Simul., 143 (2025), 108595. https://doi.org/10.1016/j.cnsns.2025.108595 doi: 10.1016/j.cnsns.2025.108595

|

| [30] |

X. J. He, S. Lin, Analytically pricing foreign exchange options under a three-factor stochastic volatility and interest rate model: A full correlation structure, Expert Syst. Appl., 246 (2024), 123203. https://doi.org/10.1016/j.eswa.2024.123203 doi: 10.1016/j.eswa.2024.123203

|

| [31] |

X. J. He, S. Lin, Analytical formulae for variance and volatility swaps with stochastic volatility, stochastic equilibrium level and regime switching, AIMS Math., 9 (2024), 22225–22238. https://doi.org/10.3934/math.20241081 doi: 10.3934/math.20241081

|

| [32] |

D. S. Bates, Jumps and stochastic volatility: Exchange rate processes implicit in deutsche mark options, Rev. Financ. Stud., 9 (1996), 69–107. https://doi.org/10.1093/rfs/9.1.69 doi: 10.1093/rfs/9.1.69

|

| [33] | A. Sepp, Pricing options on realized variance in the Heston model with jumps in returns and volatility, J. Comput. Finance, 11 (2008), 33–70. |

Figures(8) / Tables(13)

Bjørn André Aaslund, Johannes Berge, Ying Ni, Rita Pimentel. Neural network-based pricing of high-dimensional Bermudan basket options under stochastic volatility[J]. Networks and Heterogeneous Media, 2025, 20(3): 759-781. doi: 10.3934/nhm.2025032

DownLoad:

DownLoad: