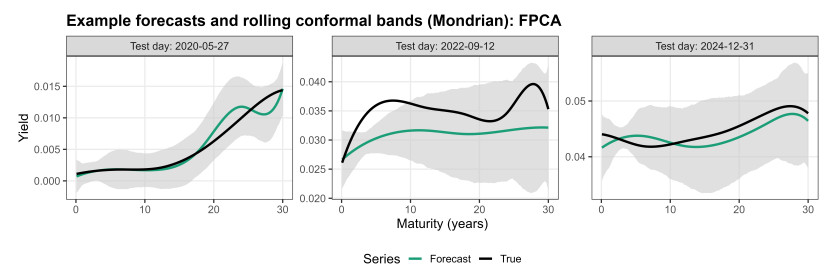

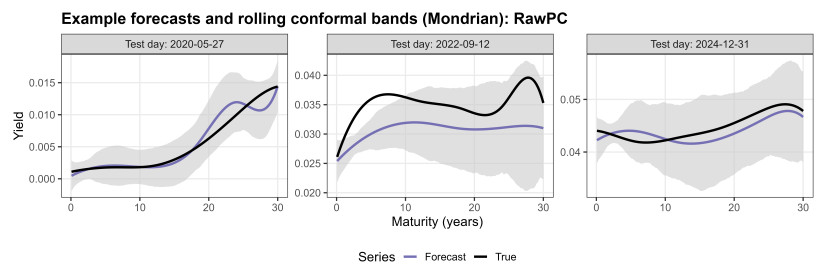

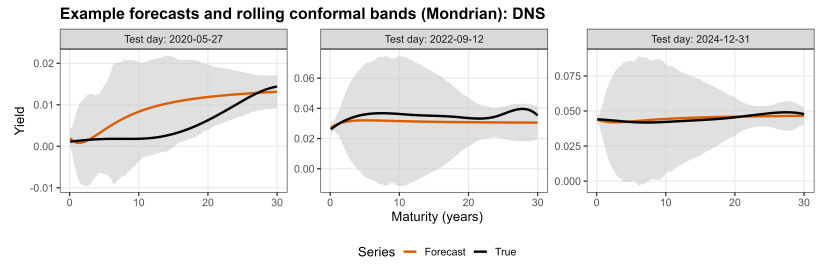

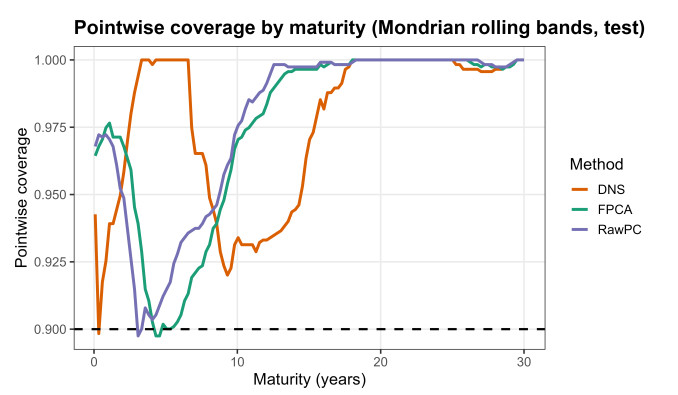

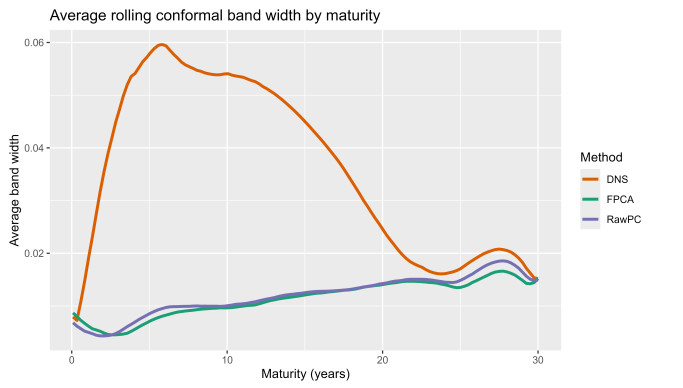

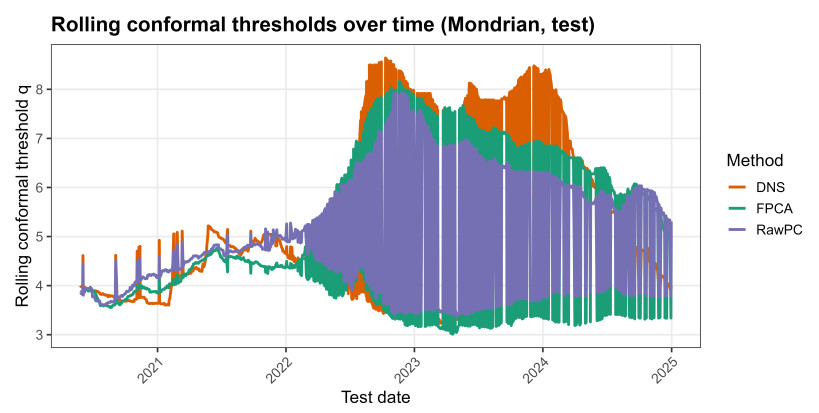

We investigated one-step-ahead daily U.S. Treasury yield-curve forecasting and provided distribution-free uncertainty quantification for the entire term structure. Using constant-maturity yields from the Federal Reserve Bank of St. Louis (FRED), we first transformed the discrete maturity panel into a dense common maturity grid through a knot-consistent ridge-regularized cubic B-spline smoother, enabling coherent curve-level evaluation. For point prediction, we modeled the yield curve as a functional time series and forecasted functional principal component (FPCA) scores with a vector autoregression (VAR). We benchmarked FPCA–VAR against two widely used alternatives: The dynamic Nelson–Siegel (DNS) model and a raw-maturity PCA–VAR (RawPC–VAR) baseline. To quantify predictive uncertainty without imposing parametric distributional assumptions, we constructed rolling studentized conformal prediction bands using a simultaneous (sup-type) nonconformity score and a moving calibration window; the associated distribution-free validity was taken in the usual conformal (exchangeable) sense and treated as an operational benchmark—rather than a literal time-series guarantee—under temporal dependence. We therefore audited calibration directly on the test block and, to probe regime heterogeneity, implemented an ex-ante Mondrian conformal variant based on a curve-shock indicator that partitioned days into HIGH and LOW regimes. Out-of-sample results showed that FPCA–VAR achieved the lowest integrated squared error and yielded substantially tighter predictive bands than DNS, while Mondrian calibration improved interpretability by revealing and partially reducing regime-dependent coverage imbalances.

Citation: Mervenur Sözen, Fikriye Kabakcı, Çağlar Sözen. Distribution-free uncertainty quantification for daily treasury yield curves with functional principal component forecasting and vector autoregression[J]. AIMS Mathematics, 2026, 11(3): 5692-5718. doi: 10.3934/math.2026234

We investigated one-step-ahead daily U.S. Treasury yield-curve forecasting and provided distribution-free uncertainty quantification for the entire term structure. Using constant-maturity yields from the Federal Reserve Bank of St. Louis (FRED), we first transformed the discrete maturity panel into a dense common maturity grid through a knot-consistent ridge-regularized cubic B-spline smoother, enabling coherent curve-level evaluation. For point prediction, we modeled the yield curve as a functional time series and forecasted functional principal component (FPCA) scores with a vector autoregression (VAR). We benchmarked FPCA–VAR against two widely used alternatives: The dynamic Nelson–Siegel (DNS) model and a raw-maturity PCA–VAR (RawPC–VAR) baseline. To quantify predictive uncertainty without imposing parametric distributional assumptions, we constructed rolling studentized conformal prediction bands using a simultaneous (sup-type) nonconformity score and a moving calibration window; the associated distribution-free validity was taken in the usual conformal (exchangeable) sense and treated as an operational benchmark—rather than a literal time-series guarantee—under temporal dependence. We therefore audited calibration directly on the test block and, to probe regime heterogeneity, implemented an ex-ante Mondrian conformal variant based on a curve-shock indicator that partitioned days into HIGH and LOW regimes. Out-of-sample results showed that FPCA–VAR achieved the lowest integrated squared error and yielded substantially tighter predictive bands than DNS, while Mondrian calibration improved interpretability by revealing and partially reducing regime-dependent coverage imbalances.

| [1] |

J. Lei, M. G'Sell, A. Rinaldo, R. J. Tibshirani, L. Wasserman, Distribution-free predictive inference for regression, J. Am. Stat. Assoc., 113 (2018), 1094–1111. https://doi.org/10.1080/01621459.2017.1307116 doi: 10.1080/01621459.2017.1307116

|

| [2] | G. Shafer, V. Vovk, A tutorial on conformal prediction, J. Mach. Learn. Res., 9 (2008), 371–421. |

| [3] | V. Vovk, A. Gammerman, G. Shafer, Algorithmic learning in a random world, Springer, 2005. |

| [4] | H. Boström, U. Johansson, T. Löfström, Mondrian conformal predictive distributions, In: Proceedings of the 11th Symposium on Conformal and Probabilistic Prediction and Applications (COPA), 152 (2021), 24–38. |

| [5] |

F. X. Diebold, R. S. Mariano, Comparing predictive accuracy, J. Bus. Econ. Stat., 13 (1995), 253–263. https://doi.org/10.1080/07350015.1995.10524599 doi: 10.1080/07350015.1995.10524599

|

| [6] | P. R. Hansen, A. Lunde, J. M. Nason, The model confidence set, Econometrica, 79 (2011), 453–495. https://doi.org/10.3982/ECTA5771 |

| [7] |

H. R. Künsch, The jackknife and the bootstrap for general stationary observations, Ann. Stat., 17 (1989), 1217–1241. https://doi.org/10.1214/aos/1176347265 doi: 10.1214/aos/1176347265

|

| [8] | S. N. Lahiri, Resampling methods for dependent data, Springer, 2003. |

| [9] |

W. K. Newey, K. D. West, A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix, Econometrica, 55 (1987), 703–708. https://doi.org/10.2307/1913610 doi: 10.2307/1913610

|

| [10] |

Ç. Sözen, Uniform one-sided conformal bands for forward realized volatility curves, AIMS Math., 10 (2025). https://doi.org/10.3934/math.20251201 doi: 10.3934/math.20251201

|

| [11] |

Ç. Sözen, F. Kabakci, Forecasting future realized variance paths with depth-weighted ridge and conformal diagnostics, AIMS Math., 10 (2025), 30246–30270. https://doi.org/10.3934/math.20251329 doi: 10.3934/math.20251329

|

| [12] |

R. Litterman, J. Scheinkman, Common factors affecting bond returns, J. Fixed Income, 1 (1991), 54–61. https://doi.org/10.3905/jfi.1991.692347 doi: 10.3905/jfi.1991.692347

|

| [13] |

C. R. Nelson, A. F. Siegel, Parsimonious modelling of yield curves, J. Bus., 60 (1987), 473–489. https://doi.org/10.1086/296409 doi: 10.1086/296409

|

| [14] | L. E. O. Svensson, Estimating and interpreting forward interest rates: Sweden 1992–1994, Sveriges Riksbank Working Paper, 1994. |

| [15] |

F. X. Diebold, C. Li, Forecasting the term structure of government bond yields, J. Econometrics, 130 (2006), 337–364. https://doi.org/10.1016/j.jeconom.2005.03.005 doi: 10.1016/j.jeconom.2005.03.005

|

| [16] |

G. R. Duffee, Term premia and interest rate forecasts in affine models, J. Finance, 57 (2002), 405–443. https://doi.org/10.1111/1540-6261.00426 doi: 10.1111/1540-6261.00426

|

| [17] |

J. H. E. Christensen, F. X. Diebold, G. D. Rudebusch, The affine arbitrage-free class of Nelson–Siegel term structure models, J. Econometrics, 164 (2022), 4–20. https://doi.org/10.1016/j.jeconom.2011.02.011 doi: 10.1016/j.jeconom.2011.02.011

|

| [18] | J. O. Ramsay, B. W. Silverman, Functional data analysis, Springer, 2 Eds., 2005. |

| [19] | L. Horváth, P. Kokoszka, Inference for functional data with applications, Springer, 2012. |

| [20] |

R. J. Hyndman, H. L. Shang, Forecasting functional time series, J. Korean Stat. Soc., 38 (2009), 199–221. https://doi.org/10.1016/j.jkss.2009.06.002 doi: 10.1016/j.jkss.2009.06.002

|

| [21] |

R. J. Hyndman, M. S. Ullah, Robust forecasting of mortality and fertility rates: A functional data approach, Comput. Stat. Data Anal., 51 (2007), 4942–4956. https://doi.org/10.1016/j.csda.2006.07.028 doi: 10.1016/j.csda.2006.07.028

|

| [22] |

S. Hays, H. Shen, J. Z. Huang, Functional dynamic factor models with application to yield curve forecasting, Ann. Appl. Stat., 6 (2012), 870–894. https://doi.org/10.1214/12-AOAS551 doi: 10.1214/12-AOAS551

|

| [23] |

L. Horváth, P. Kokoszka, J. VanderDoes, S. Wang, Inference in functional factor models with applications to yield curves, J. Time Ser. Anal., 43 (2022), 872–894. https://doi.org/10.1111/jtsa.12642 doi: 10.1111/jtsa.12642

|

| [24] |

H. L. Shang, F. Kearney, Dynamic functional time-series forecasts of foreign exchange implied volatility surfaces, Int. J. Forecasting, 38 (2022), 1025–1049. https://doi.org/10.1016/j.ijforecast.2021.07.011 doi: 10.1016/j.ijforecast.2021.07.011

|

| [25] | T. H. Khoo, I. M. Dabo, D. Pathmanathan, S. Dabo-Niang, Generalized functional dynamic principal component analysis, arXiv preprint, 2024. https://doi.org/10.48550/arXiv.2407.16024 |

| [26] |

E. Diquigiovanni, S. Fontana, S. Vantini, Conformal prediction bands for multivariate functional data, J. Multivariate Anal., 189 (2022), 104879. https://doi.org/10.1016/j.jmva.2021.104879 doi: 10.1016/j.jmva.2021.104879

|

| [27] | C. Xu, Y. Xie, Conformal prediction intervals for dynamic time-series, In: Proceedings of the 38th International Conference on Machine Learning (ICML), 139 (2021), 11559–11569. |

| [28] |

C. Xu, Y. Xie, Conformal prediction for time series, IEEE T. Pattern Anal., 45 (2023), 11575–11587. https://doi.org/10.1109/TPAMI.2023.3272339 doi: 10.1109/TPAMI.2023.3272339

|

| [29] | I. Gibbs, E. J. Candès, Adaptive conformal inference under distribution shift, In: Advances in Neural Information Processing Systems (NeurIPS), 2021. https://doi.org/10.48550/arXiv.2106.00170 |

| [30] | M. Zaffran, V. Féron, Y. Goude, J. Josse, A. Dieuleveut, Adaptive conformal predictions for time series, In: Proceedings of the 39th International Conference on Machine Learning (ICML), 162 (2022), 25834–25866. |

| [31] |

R. I. Oliveira, P. Orenstein, T. Ramos, J. V. Romano, Split conformal prediction and non-exchangeable data, J. Mach. Learn. Res., 25 (2024), 1–38. https://doi.org/10.48550/arXiv.2203.15885 doi: 10.48550/arXiv.2203.15885

|

| [32] | R. F. Barber, A. Pananjady, Predictive inference for time series: why is split conformal effective despite temporal dependence? arXiv preprint, 2026. https://doi.org/10.48550/arXiv.2510.02471 |

| [33] | Federal Reserve Bank of St. Louis, FRED: Federal Reserve Economic Data (daily U.S. Treasury constant-maturity series), accessed 2025. |

| [34] |

R. Dahlhaus, Fitting time series models to nonstationary processes, Ann. Stat., 25 (1997), 1–37. https://doi.org/10.1214/aos/1034276620 doi: 10.1214/aos/1034276620

|

| [35] |

D. N. Politis, J. P. Romano, The stationary bootstrap, J. Am. Stat. Assoc., 89 (1994), 1303–1313. https://doi.org/10.1080/01621459.1994.10476870 doi: 10.1080/01621459.1994.10476870

|

Figures(8) / Tables(11)

Mervenur Sözen, Fikriye Kabakcı, Çağlar Sözen. Distribution-free uncertainty quantification for daily treasury yield curves with functional principal component forecasting and vector autoregression[J]. AIMS Mathematics, 2026, 11(3): 5692-5718. doi: 10.3934/math.2026234

DownLoad:

DownLoad: