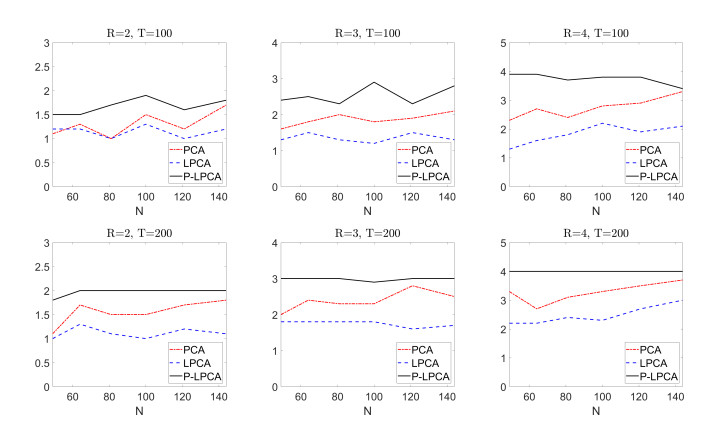

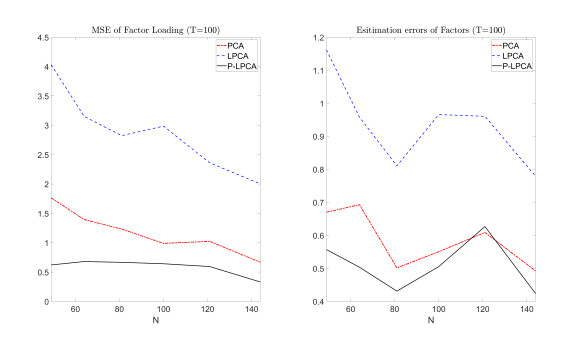

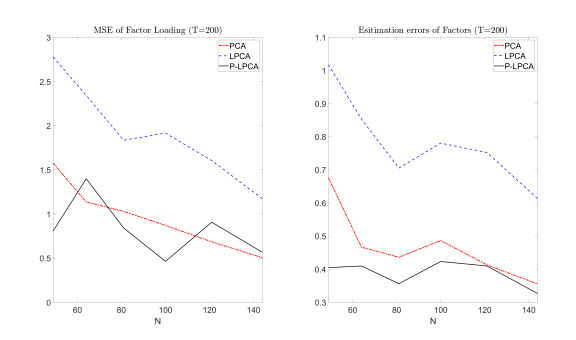

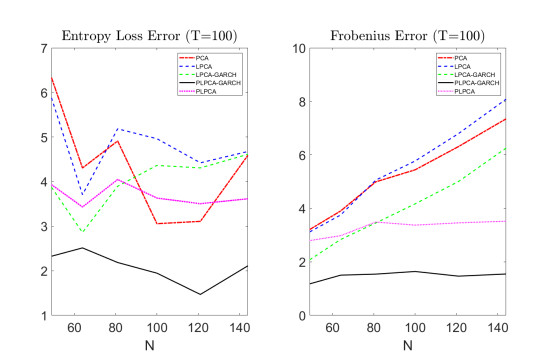

In this paper, we established a time-varying latent factor model with GARCH (generalized autoregressive conditional heteroskedasticity) noise to study volatilities (conditional covariance matrix) under the high-dimensional framework, when factors are unobservable, factor loadings are time-varying, and the idiosyncratic error term shows heteroskedasticity. A projection method was proposed for more-precise estimation of the conditional covariance matrix. We demonstrated that our model is robust when the dimensionality and sample size are large. Asymptotic theories were developed for the proposed estimation. A simulation study was conducted to evaluate the performance of the proposed model, and a real example was provided to illustrate this approach.

Citation: Yuwen Ruan, Xingfa Zhang, Yujiao Liu, Yan Wang, Tianli Lei. A time-varying latent factor model with GARCH noise for high-dimensional covariance matrix estimation[J]. AIMS Mathematics, 2026, 11(3): 5575-5599. doi: 10.3934/math.2026230

In this paper, we established a time-varying latent factor model with GARCH (generalized autoregressive conditional heteroskedasticity) noise to study volatilities (conditional covariance matrix) under the high-dimensional framework, when factors are unobservable, factor loadings are time-varying, and the idiosyncratic error term shows heteroskedasticity. A projection method was proposed for more-precise estimation of the conditional covariance matrix. We demonstrated that our model is robust when the dimensionality and sample size are large. Asymptotic theories were developed for the proposed estimation. A simulation study was conducted to evaluate the performance of the proposed model, and a real example was provided to illustrate this approach.

| [1] |

G. Connor, O. Linton, Semiparametric estimation of a characteristic-based factor model of common stock returns, J. Empir. Finance, 14 (2007), 694–717. https://doi.org/10.1016/j.jempfin.2006.10.001 doi: 10.1016/j.jempfin.2006.10.001

|

| [2] |

C. M. Hafner, A. Preminger, Asymptotic theory for a factor GARCH model, Econ. Theory, 25 (2009), 336–363. https://doi.org/10.1017/S0266466608090117 doi: 10.1017/S0266466608090117

|

| [3] |

A. Onatski, Asymptotics of the principal components estimator of large factor models with weakly influential factors, J. Econ., 168 (2012), 244–258. https://doi.org/10.1016/j.jeconom.2012.01.034 doi: 10.1016/j.jeconom.2012.01.034

|

| [4] |

G. Motta, C. M. Hafner, R. von Sachs, Locally stationary factor models: Identification and nonparametric estimation, Econ. Theory, 27 (2011), 1279–1319. https://doi.org/10.1017/S0266466611000053 doi: 10.1017/S0266466611000053

|

| [5] |

L. Su, X. Wang, On time-varying factor models: Estimation and testing, J. Econ., 198 (2017), 84–101. https://doi.org/10.1016/j.jeconom.2016.12.004 doi: 10.1016/j.jeconom.2016.12.004

|

| [6] |

M. Chen, X. Tan, J. Wu, Time varying factor models with possibly strongly correlated noises, J. Appl. Stat., 48 (2021), 887–906. https://doi.org/10.1080/02664763.2020.1753024 doi: 10.1080/02664763.2020.1753024

|

| [7] |

M. Barigozzi, M. Hallin, S. Soccorsi, R. von Sachs, Time-varying general dynamic factor models and the measurement of financial connectedness, J. Econ., 222 (2021), 324–343. https://doi.org/10.1016/j.jeconom.2020.07.004 doi: 10.1016/j.jeconom.2020.07.004

|

| [8] |

L. Chen, J. J. Dolado, J. Gonzalo, Quantile factor models, Econometrica, 89 (2021), 875–910. https://doi.org/10.3982/ECTA15746 doi: 10.3982/ECTA15746

|

| [9] | Q. Chen, N. Roussanov, X. Wang, Semiparametric conditional factor models: Estimation and inference, technical report, National Bureau of Economic Research, 2023. |

| [10] |

X. Wang, S. Jin, Y. Li, J. Qian, L. Su, On time-varying panel data models with time-varying interactive fixed effects, J. Econ., 249 (2025), 105960. https://doi.org/10.1016/j.jeconom.2025.105960 doi: 10.1016/j.jeconom.2025.105960

|

| [11] |

Y. Tu, S. Wang, Quantile prediction with factor-augmented regression: Structural instability and model uncertainty, J. Econ., 249 (2025), 105999. https://doi.org/10.1016/j.jeconom.2025.105999 doi: 10.1016/j.jeconom.2025.105999

|

| [12] |

R. F. Engle, K. F. Kroner, Multivariate simultaneous generalized arch, Econ. Theory, 11 (1995), 122–150. https://doi.org/10.1017/S0266466600009063 doi: 10.1017/S0266466600009063

|

| [13] | T. Bollerslev, Modelling the coherence in short-run nominal exchange rates: A multivariate generalized arch model, Rev. Econom. Stat., 1990,498–505. |

| [14] |

R. Engle, Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models, J. Busin. Econ. Stat., 20 (2002), 339–350. https://doi.org/10.1198/073500102288618487 doi: 10.1198/073500102288618487

|

| [15] |

S. Guo, J. L. Box, W. Zhang, A dynamic structure for high-dimensional covariance matrices and its application in portfolio allocation, J. Amer. Stat. Assoc., 112 (2017), 235–253. https://doi.org/10.1080/01621459.2015.1129969 doi: 10.1080/01621459.2015.1129969

|

| [16] |

P. Wang, X. Liu, S. Wu, Dynamic linkage between bitcoin and traditional financial assets: A comparative analysis of different time frequencies, Entropy, 24 (2022), 1565. https://doi.org/10.3390/e24111565 doi: 10.3390/e24111565

|

| [17] |

X. L. Li, Y. Li, J. Z. Pan, X. F. Zhang, A factor-garch model for high dimensional volatilities, Acta Math. Appl. Sin. Engl. Ser., 38 (2022), 635–663. https://doi.org/10.1007/s10255-022-1104-6 doi: 10.1007/s10255-022-1104-6

|

| [18] |

Y. Liu, Y. Li, X. Zhang, Estimation of conditional covariance matrices for a class of high-dimensional varying coefficient factor-generalized autoregressive conditional heteroscedasticity model, Symmetry, 16 (2024), 1635. https://doi.org/10.3390/sym16121635 doi: 10.3390/sym16121635

|

| [19] |

A. Laksaci, F. Alshahrani, I. M. Almanjahie, Z. Kaid, Nonparametric multifunctional garch time series data analysis: Application to dynamic forecasting in financial data, AIMS Math., 10 (2025), 26459–26483. https://doi.org/10.3934/math.20251163 doi: 10.3934/math.20251163

|

| [20] |

R. Alraddadi, The markov-switching threshold blgarch model, AIMS Math., 10 (2025), 18838–18860. http://doi.org/10.3934/math.2025842 doi: 10.3934/math.2025842

|

| [21] |

Y. Ruan, X. Zhang, Y. Liu, A semi-parametric factor-garch model for high dimensional covariance matrix estimation, J. Korean Stat. Soc., 54 (2025), 888–919. https://doi.org/10.1007/s42952-025-00324-4 doi: 10.1007/s42952-025-00324-4

|

| [22] |

M. H. Pesaran, Estimation and inference in large heterogeneous panels with a multifactor error structure, Econometrica, 74 (2006), 967–1012. https://doi.org/10.1111/j.1468-0262.2006.00692.x doi: 10.1111/j.1468-0262.2006.00692.x

|

| [23] |

S. C. Ahn, A. R. Horenstein, Eigenvalue ratio test for the number of factors, Econometrica, 81 (2013), 1203–1227. https://doi.org/10.3982/ECTA8968 doi: 10.3982/ECTA8968

|

| [24] |

C. Francq, J. M. Zakoïan, Estimating multivariate volatility models equation by equation, J. Royal Stat. Soc. Ser. B: Stat. Methodol., 78 (2016), 613–635. https://doi.org/10.1111/rssb.12126 doi: 10.1111/rssb.12126

|

| [25] |

J. Fan, Y. Fan, J. Lv, High dimensional covariance matrix estimation using a factor model, J. Econ., 147 (2008), 186–197. https://doi.org/10.1016/j.jeconom.2008.09.017 doi: 10.1016/j.jeconom.2008.09.017

|

| [26] |

J. H. Stock, M. W. Watson, Forecasting using principal components from a large number of predictors, J. Amer. Stat. Assoc., 97 (2002), 1167–1179. https://doi.org/10.1198/016214502388618960 doi: 10.1198/016214502388618960

|

| [27] |

J. Bai, Inferential theory for factor models of large dimensions, Econometrica, 71 (2003), 135–171. https://doi.org/10.1111/1468-0262.00392 doi: 10.1111/1468-0262.00392

|

| [28] | W. James, C. Stein, Estimation with quadratic loss, In: Breakthroughs in Statistics: Foundations and Basic Theory, New York: Springer, 1992,443–460. |

| [29] | R. S. Tsay, Multivariate Time Series Analysis: With R and Financial Applications, Hoboken: John Wiley & Sons, 2013. |

| [30] |

R. C. Scott, P. A. Horvath, On the direction of preference for moments of higher order than the variance, J. Finance, 35 (1980), 915–919. https://doi.org/10.2307/2327209 doi: 10.2307/2327209

|

| [31] |

R. F. Dittmar, Nonlinear pricing kernels, kurtosis preference, and evidence from the cross section of equity returns, J. Finance, 57 (2002), 369–403. https://doi.org/10.1111/1540-6261.00425 doi: 10.1111/1540-6261.00425

|

| [32] |

Z. Zhu, N. Zhang, K. Zhu, Big portfolio selection by graph-based conditional moments method, J. Empir. Finance, 78 (2024), 101533. https://doi.org/10.1016/j.jempfin.2024.101533 doi: 10.1016/j.jempfin.2024.101533

|

| [33] |

J. Fan, Y. Liao, M. Mincheva, High dimensional covariance matrix estimation in approximate factor models, Ann. Stat., 39 (2011), 3320. https://doi.org/10.1214/11-AOS944 doi: 10.1214/11-AOS944

|

| [34] |

X. Li, X. Zhang, Y. Li, High-dimensional conditional covariance matrices estimation using a factor-garch model, Symmetry, 14 (2022), 158. https://doi.org/10.3390/sym14010158 doi: 10.3390/sym14010158

|

Figures(6) / Tables(8)

Yuwen Ruan, Xingfa Zhang, Yujiao Liu, Yan Wang, Tianli Lei. A time-varying latent factor model with GARCH noise for high-dimensional covariance matrix estimation[J]. AIMS Mathematics, 2026, 11(3): 5575-5599. doi: 10.3934/math.2026230

DownLoad:

DownLoad: