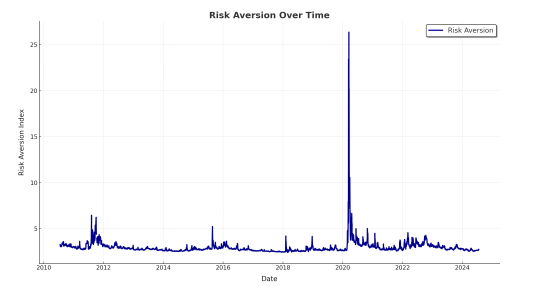

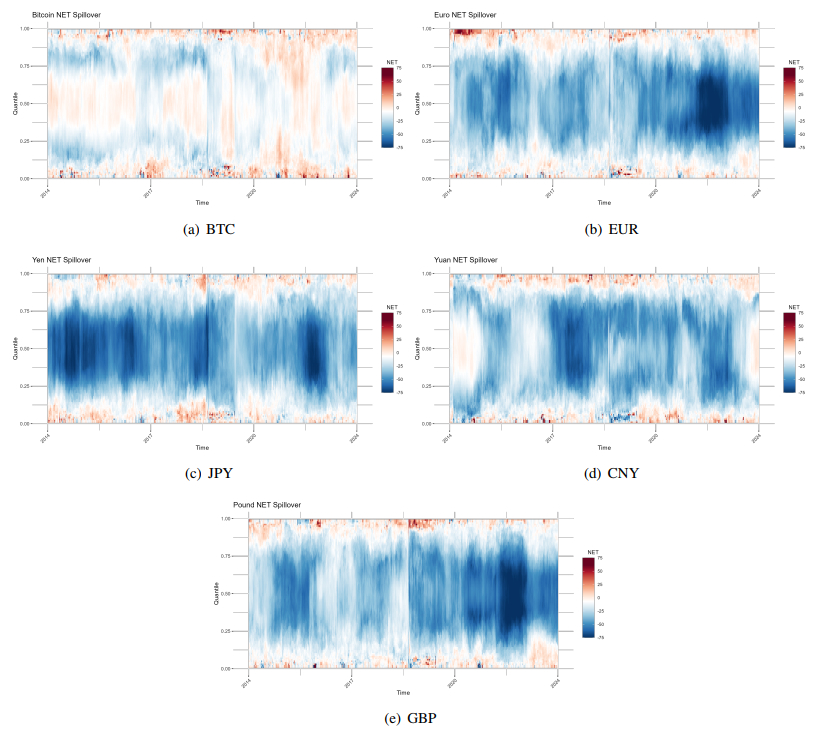

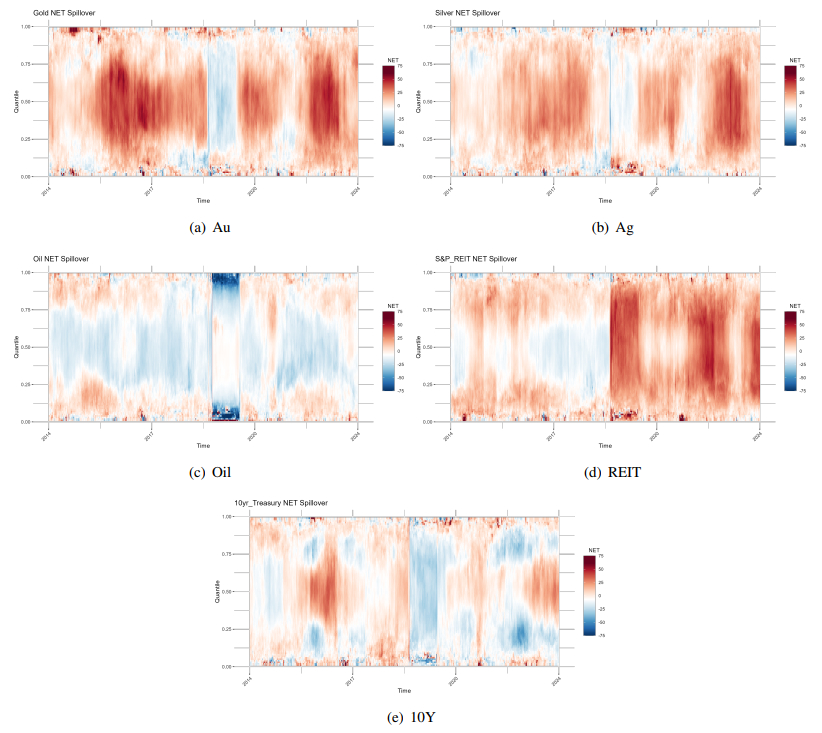

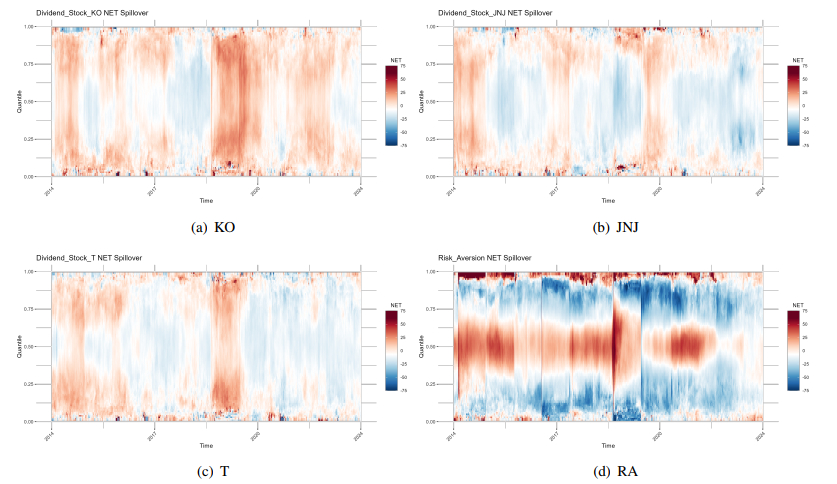

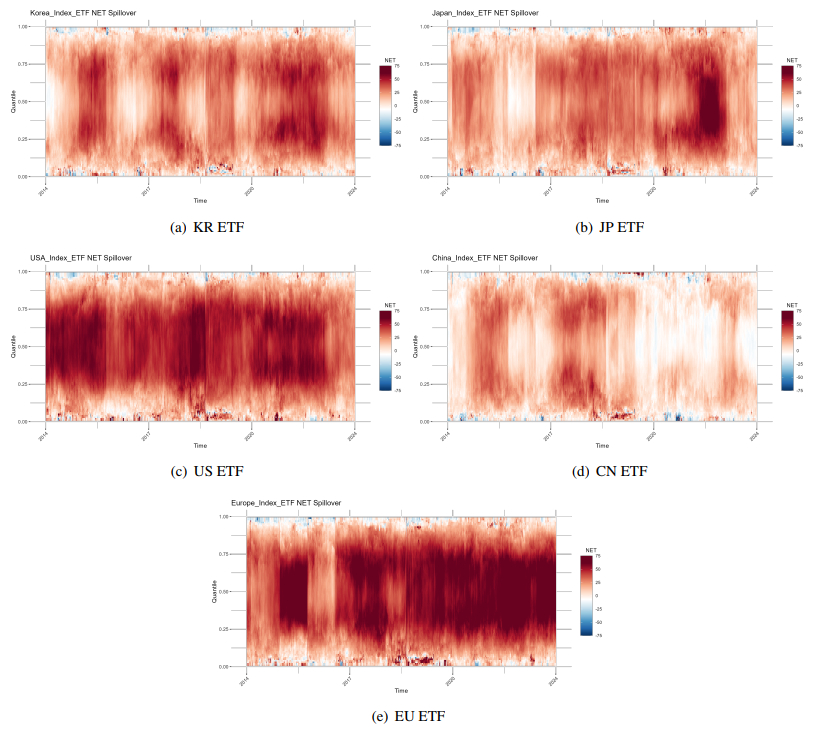

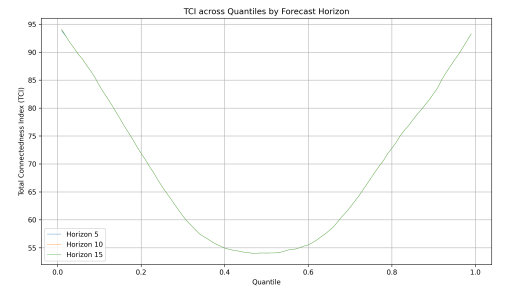

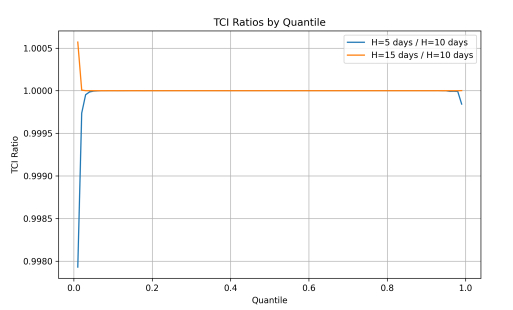

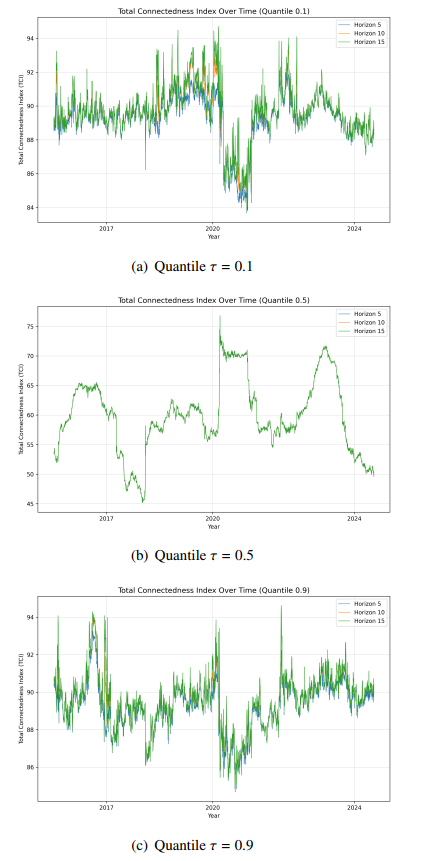

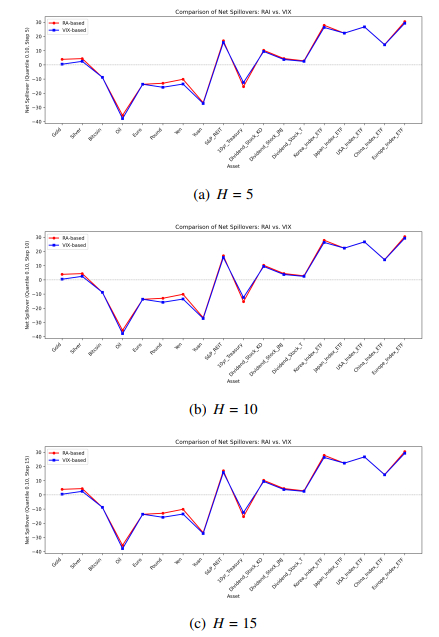

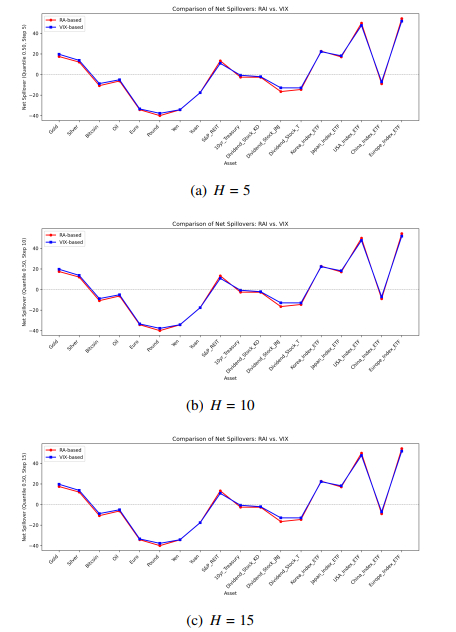

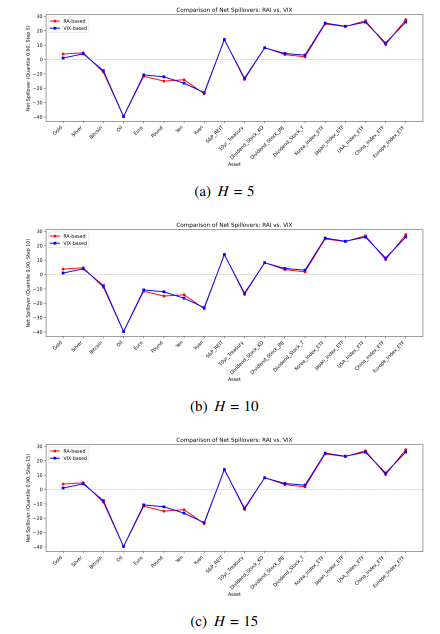

In this study, we used a rolling-window quantile vector autoregression (QVAR) spillover framework to analyze how shocks associated with investor risk aversion propagate across major asset classes under different market states. The study spanned July 2014 to July 2024 and included gold, silver, Bitcoin, crude oil, major currencies, real estate investment trusts (REITs), U.S. Treasuries, dividend-paying equities, and broad equity indices. By estimating spillovers at the 10th, 50th, and 90th conditional return quantiles, we distinguished risk transmitters and risk absorbers in stressed, normal, and euphoric regimes. We then tested robustness across forecast horizons and alternative fear measures (our baseline risk-aversion index versus the VIX). The results indicated that, under normal conditions, Bitcoin is a dominant net transmitter of shocks, exporting risk to other assets, while traditional safe-haven assets, such as gold and silver, primarily absorb risk. In bull markets, Bitcoin's transmitting role intensifies and aligns with other high-beta assets, such as REITs, suggesting that Bitcoin amplifies risk-taking during periods of market optimism. However, under bear markets, Bitcoin's spillover power weakens sharply. Instead, U.S. Treasuries and gold emerge as key shock absorbers, reinforcing their defensive status during crisis periods. These findings suggest that Bitcoin is valuable for upside-oriented diversification but remains less reliable than Treasuries or gold as a downside hedge. The consistency of these patterns across horizons and fear proxies highlights the broader applicability of our framework for studying systemic risk, portfolio allocation, and safe-haven behavior.

Citation: Seung Ho Choi, Hayoung Choi, Sun-Yong Choi. Risk aversion, safe-haven assets, and Bitcoin's evolving role in global financial markets: Insights from quantile spillover analysis[J]. AIMS Mathematics, 2026, 11(1): 2481-2526. doi: 10.3934/math.2026101

In this study, we used a rolling-window quantile vector autoregression (QVAR) spillover framework to analyze how shocks associated with investor risk aversion propagate across major asset classes under different market states. The study spanned July 2014 to July 2024 and included gold, silver, Bitcoin, crude oil, major currencies, real estate investment trusts (REITs), U.S. Treasuries, dividend-paying equities, and broad equity indices. By estimating spillovers at the 10th, 50th, and 90th conditional return quantiles, we distinguished risk transmitters and risk absorbers in stressed, normal, and euphoric regimes. We then tested robustness across forecast horizons and alternative fear measures (our baseline risk-aversion index versus the VIX). The results indicated that, under normal conditions, Bitcoin is a dominant net transmitter of shocks, exporting risk to other assets, while traditional safe-haven assets, such as gold and silver, primarily absorb risk. In bull markets, Bitcoin's transmitting role intensifies and aligns with other high-beta assets, such as REITs, suggesting that Bitcoin amplifies risk-taking during periods of market optimism. However, under bear markets, Bitcoin's spillover power weakens sharply. Instead, U.S. Treasuries and gold emerge as key shock absorbers, reinforcing their defensive status during crisis periods. These findings suggest that Bitcoin is valuable for upside-oriented diversification but remains less reliable than Treasuries or gold as a downside hedge. The consistency of these patterns across horizons and fear proxies highlights the broader applicability of our framework for studying systemic risk, portfolio allocation, and safe-haven behavior.

| [1] |

J. A. Carlson, Risk aversion, foreign exchange speculation and gambler's ruin, Economica, 65 (1998), 441–453. https://doi.org/10.1111/1468-0335.00138 doi: 10.1111/1468-0335.00138

|

| [2] | R. S. Pindyck, Risk aversion and determinants of stock market behavior, Working Paper, 1986. |

| [3] |

K. Kassimatis, Risk aversion with local risk seeking and stock returns: Evidence from the uk market, J. Bus. Finan. Account., 38 (2011), 713–739. https://doi.org/10.1111/j.1468-5957.2011.02243.x doi: 10.1111/j.1468-5957.2011.02243.x

|

| [4] |

G. Gorton, G. Ordonez, The supply and demand for safe assets, J. Monetary Econ., 125 (2022), 132–147. https://doi.org/10.1016/j.jmoneco.2021.07.010 doi: 10.1016/j.jmoneco.2021.07.010

|

| [5] |

E. Feder-Sempach, P. Szczepocki, J. Bogoebska, Global uncertainty and potential shelters: Gold, bitcoin, and currencies as weak and strong safe havens for main world stock markets, Financ. Innov., 10 (2024), 67. https://doi.org/10.1186/s40854-023-00589-w doi: 10.1186/s40854-023-00589-w

|

| [6] |

F. Le Grand, X. Ragot, Sovereign default and liquidity: The case for a world safe asset, J. Int. Econ., 131 (2021), 103462. https://doi.org/10.1016/j.jinteco.2021.103462 doi: 10.1016/j.jinteco.2021.103462

|

| [7] |

Z. He, A. Krishnamurthy, K. Milbradt, What makes us government bonds safe assets?, Am. Econ. Rev., 106 (2016), 519–523. https://doi.org/10.1257/aer.p20161109 doi: 10.1257/aer.p20161109

|

| [8] |

T. Bettendorf, R. Heinlein, Connectedness between G10 currencies: Searching for the causal structure, Int. J. Finan. Econ., 28 (2023), 3938–3959. https://doi.org/10.1002/ijfe.2629 doi: 10.1002/ijfe.2629

|

| [9] |

Z. Umar, A. Bossman, S. Y. Choi, T. Teplova, The relationship between global risk aversion and returns from safe-haven assets, Financ. Res. Lett., 51 (2023), 103444. https://doi.org/10.1016/j.frl.2022.103444 doi: 10.1016/j.frl.2022.103444

|

| [10] | D. G. Baur, T. Dimpfl, K. Kuck, Safe haven assets-the bigger picture, Available at SSRN 3800872, 2021. https://doi.org/10.2139/ssrn.3800872 |

| [11] |

C. Gurdgiev, A. Petrovskiy, Hedging and safe haven assets dynamics in developed and developing markets: Are different markets that much different?, Int. Rev. Financ. Anal., 92 (2024), 103059. https://doi.org/10.1016/j.irfa.2023.103059 doi: 10.1016/j.irfa.2023.103059

|

| [12] |

R. Khalfaoui, S. B. Jabeur, B. Dogan, The spillover effects and connectedness among green commodities, Bitcoins, and us stock markets: Evidence from the quantile VAR network, J. Environ. Manage., 306 (2022), 114493. https://doi.org/10.1016/j.jenvman.2022.114493 doi: 10.1016/j.jenvman.2022.114493

|

| [13] |

S. Long, Z. Li, Dynamic spillover effects of global financial stress: Evidence from the quantile var network, Int. Rev. Financ. Anal., 90 (2023), 102945. https://doi.org/10.1016/j.irfa.2023.102945 doi: 10.1016/j.irfa.2023.102945

|

| [14] |

M. E. Hoque, M. Billah, B. Kapar, M. A. Naeem, Quantifying the volatility spillover dynamics between financial stress and us financial sectors: Evidence from QVAR connectedness, Int. Rev. Financ. Anal., 95 (2024), 103434. https://doi.org/10.1016/j.irfa.2024.103434 doi: 10.1016/j.irfa.2024.103434

|

| [15] |

J. Wang, S. Mishra, A. Sharif, H. Chen, Dynamic spillover connectedness among green finance and policy uncertainty: Evidence from QVAR network approach, Energ. Econ., 131 (2024), 107330. https://doi.org/10.1016/j.eneco.2024.107330 doi: 10.1016/j.eneco.2024.107330

|

| [16] |

N. Kyriazis, S. Papadamou, P. Tzeremes, S. Corbet, Examining spillovers and connectedness among commodities, inflation, and uncertainty: A quantile-VAR framework, Energ. Econ., 133 (2024), 107508. https://doi.org/10.1016/j.eneco.2024.107330 doi: 10.1016/j.eneco.2024.107330

|

| [17] |

D. J. Kim, E. Noh, S. Y. Choi, Quantile spillover effects and sector dynamics in US stock markets: Normal vs. extreme market conditions, Financ. Res. Lett., 83 (2025), 107608. https://doi.org/10.1016/j.frl.2025.107608 doi: 10.1016/j.frl.2025.107608

|

| [18] |

F. Zhu, S. Fu, X. Liu, A quantile spillover-driven markov switching model for volatility forecasting: Evidence from the cryptocurrency market, Mathematics, 13 (2025), 2382. https://doi.org/10.3390/math13152382 doi: 10.3390/math13152382

|

| [19] |

J. Cunado, I. Chatziantoniou, D. Gabauer, F. P. de Gracia, M. Hardik, Dynamic spillovers across precious metals and oil realized volatilities: Evidence from quantile extended joint connectedness measures, J. Commod. Mark., 30 (2023), 100327. https://doi.org/10.1016/j.jcomm.2023.100327 doi: 10.1016/j.jcomm.2023.100327

|

| [20] |

I. Chatziantoniou, D. Gabauer, H. A. Marfatia, Dynamic connectedness and spillovers across sectors: Evidence from the indian stock market, Scot. J. Polit. Econ., 69 (2022), 283–300. https://doi.org/10.1111/sjpe.12291 doi: 10.1111/sjpe.12291

|

| [21] |

R. Gupta, H. A. Marfatia, The impact of unconventional monetary policy shocks in the us on emerging market reits, J. Real Estate Lit., 26 (2018), 175–188. https://doi.org/10.1080/10835547.2018.12090476 doi: 10.1080/10835547.2018.12090476

|

| [22] |

G. Bekaert, E. C. Engstrom, N. R. Xu, The time variation in risk appetite and uncertainty, Manage. Sci., 68 (2022), 3975–4004. https://doi.org/10.1287/mnsc.2021.4068 doi: 10.1287/mnsc.2021.4068

|

| [23] |

I. Chatziantoniou, D. Gabauer, A. Stenfors, Interest rate swaps and the transmission mechanism of monetary policy: A quantile connectedness approach, Econ. Lett., 204 (2021), 109891. https://doi.org/10.1016/j.econlet.2021.109891 doi: 10.1016/j.econlet.2021.109891

|

| [24] |

I. Chatziantoniou, E. J. A. Abakah, D. Gabauer, A. K. Tiwari, Quantile time–frequency price connectedness between green bond, green equity, sustainable investments and clean energy markets, J. Clean. Prod., 361 (2022), 132088. https://doi.org/10.1016/j.jclepro.2022.132088 doi: 10.1016/j.jclepro.2022.132088

|

| [25] |

E. Bouri, T. Saeed, X. V. Vo, D. Roubaud, Quantile connectedness in the cryptocurrency market, J. Int. Financ. Mark. I., 71 (2021), 101302. https://doi.org/10.1016/j.intfin.2021.101302 doi: 10.1016/j.intfin.2021.101302

|

| [26] |

M. Zhao, H. Park, Quantile time-frequency spillovers among green bonds, cryptocurrencies, and conventional financial markets, Int. Rev. Financ. Anal., 93 (2024), 103198. https://doi.org/10.1016/j.irfa.2024.103198 doi: 10.1016/j.irfa.2024.103198

|

| [27] |

P. Joshi, Regime-specific interdependencies in cryptocurrency markets: A high-frequency gmm-var approach, Data Sci. Financ. Econ., 5 (2025), 419–439. https://doi.org/10.3934/DSFE.2025017 doi: 10.3934/DSFE.2025017

|

| [28] |

P. S. Ko, K. S. Chen, Discovering ai tokens in the fractal markets hypothesis and their time-frequency co-movements with the leading high-carbon cryptocurrency, Data Sci. Financ. Econ., 5 (2025), 293–319. https://doi.org/10.3934/DSFE.2025013 doi: 10.3934/DSFE.2025013

|

| [29] |

M. Abdullah, D. Adeabah, E. J. A. Abakah, C. C. Lee, Extreme return and volatility connectedness among real estate tokens, REITs, and other assets: The role of global factors and portfolio implications, Financ. Res. Lett., 56 (2023), 104062. https://doi.org/10.1016/j.frl.2023.104062 doi: 10.1016/j.frl.2023.104062

|

| [30] |

H. Asgharian, C. Christiansen, A. J. Hou, The effect of uncertainty on stock market volatility and correlation, J. Bank. Financ., 154 (2023), 106929. https://doi.org/10.1016/j.jbankfin.2023.106929 doi: 10.1016/j.jbankfin.2023.106929

|

| [31] |

C. Huber, J. Huber, M. Kirchler, Market shocks and professionals' investment behavior–evidence from the COVID-19 crash, J. Bank. Financ., 133 (2021), 106247. https://doi.org/10.1016/j.jbankfin.2021.106247 doi: 10.1016/j.jbankfin.2021.106247

|

| [32] |

V. Coudert, M. Gex, Does risk aversion drive financial crises? testing the predictive power of empirical indicators, J. Empir. Financ., 15 (2008), 167–184. https://doi.org/10.1016/j.jempfin.2007.06.001 doi: 10.1016/j.jempfin.2007.06.001

|

| [33] |

G. Bekaert, M. Hoerova, M. L. Duca, Risk, uncertainty and monetary policy, J. Monetary Econ., 60 (2013), 771–788. https://doi.org/10.1016/j.jmoneco.2013.06.003 doi: 10.1016/j.jmoneco.2013.06.003

|

| [34] |

S. J. H. Shahzad, E. Bouri, D. Roubaud, L. Kristoufek, B. Lucey, Is bitcoin a better safe-haven investment than gold and commodities?, Int. Rev. Financ. Anal., 63 (2019), 322–330. https://doi.org/10.1016/j.irfa.2019.01.002 doi: 10.1016/j.irfa.2019.01.002

|

| [35] |

L. A. Smales, Bitcoin as a safe haven: Is it even worth considering?, Financ. Res. Lett., 30 (2019), 385–393. https://doi.org/10.1016/j.frl.2018.11.002 doi: 10.1016/j.frl.2018.11.002

|

| [36] |

M. Umar, C. W. Su, S. K. A. Rizvi, X. F. Shao, Bitcoin: A safe haven asset and a winner amid political and economic uncertainties in the us?, Technol. Forecast. Soc., 167 (2021), 120680. https://doi.org/10.1016/j.techfore.2021.120680 doi: 10.1016/j.techfore.2021.120680

|

| [37] |

E. Bouri, P. Molnár, G. Azzi, D. Roubaud, L. I. Hagfors, On the hedge and safe haven properties of bitcoin: Is it really more than a diversifier?, Financ. Res. Lett., 20 (2017), 192–198. https://doi.org/10.1016/j.frl.2016.09.025 doi: 10.1016/j.frl.2016.09.025

|

| [38] |

A. Kliber, P. Marszałek, I. Musiałkowska, K. Świerczyńska, Bitcoin: Safe haven, hedge or diversifier? Perception of Bitcoin in the context of a country's economic situation—a stochastic volatility approach, Physica A, 524 (2019), 246–257. https://doi.org/10.1016/j.physa.2019.04.145 doi: 10.1016/j.physa.2019.04.145

|

| [39] |

E. Bouri, S. J. H. Shahzad, D. Roubaud, L. Kristoufek, B. Lucey, Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis, Q. Rev. Econ. Financ., 77 (2020), 156–164. https://doi.org/10.1016/j.qref.2020.03.004 doi: 10.1016/j.qref.2020.03.004

|

| [40] |

S. J. H. Shahzad, E. Bouri, D. Roubaud, L. Kristoufek, Safe haven, hedge and diversification for G7 stock markets: Gold versus Bitcoin, Econ. Model., 87 (2020), 212–224. https://doi.org/10.5325/pennhistory.87.1.0212 doi: 10.5325/pennhistory.87.1.0212

|

| [41] |

D. G. Baur, B. M. Lucey, Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold, Financ. Rev., 45 (2010), 217–229. https://doi.org/10.1111/j.1540-6288.2010.00244.x doi: 10.1111/j.1540-6288.2010.00244.x

|

| [42] |

N. Antonakakis, I. Chatziantoniou, D. Gabauer, Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions, J. Risk Financ. Manag., 13 (2020), 84. https://doi.org/10.3390/jrfm13040084 doi: 10.3390/jrfm13040084

|

| [43] |

T. Ando, M. Greenwood-Nimmo, Y. Shin, Quantile connectedness: Modeling tail behavior in the topology of financial networks, Manage. Sci., 68 (2022), 2401–2431. https://doi.org/10.1287/mnsc.2021.3984 doi: 10.1287/mnsc.2021.3984

|

| [44] |

S. Corbet, Y. Hou, Y. Hu, L. Oxley, Time varying risk aversion and its connectedness: Evidence from cryptocurrencies, Ann. Oper. Res., 338 (2024), 879–923. https://doi.org/10.1007/s10479-024-06001-9 doi: 10.1007/s10479-024-06001-9

|

| [45] |

R. Demirer, K. Gkillas, R. Gupta, C. Pierdzioch, Risk aversion and the predictability of crude oil market volatility: A forecasting experiment with random forests, J. Oper. Res. Soc., 73 (2022), 1755–1767. https://doi.org/10.1080/01605682.2021.1936668 doi: 10.1080/01605682.2021.1936668

|

| [46] |

C. Pflueger, G. Rinaldi, Why does the fed move markets so much? A model of monetary policy and time-varying risk aversion, J. Financ. Econ., 146 (2022), 71–89. https://doi.org/10.1016/j.jfineco.2022.06.002 doi: 10.1016/j.jfineco.2022.06.002

|

| [47] |

X. Wu, Q. He, H. Xie, Forecasting VIX with time-varying risk aversion, Int. Rev. Econ. Financ., 88 (2023), 458–475. https://doi.org/10.1016/j.iref.2023.06.034 doi: 10.1016/j.iref.2023.06.034

|

| [48] |

Z. Umar, A. Bossman, T. Teplova, E. Marfo-Yiadom, Does time-varying risk aversion sentiment matter in the connectedness among Sub-Saharan African bond markets?, Emerg. Mark. Rev., 61 (2024), 101160. https://doi.org/10.1016/j.ememar.2024.101160 doi: 10.1016/j.ememar.2024.101160

|

| [49] |

S. Y. Choi, E. Hadad, The dynamic relationship among economic and monetary policy, geopolitical risk, sentiment, and risk aversion: A TVP-VAR approach, Financ. Res. Lett., 72 (2025), 106532. https://doi.org/10.1016/j.frl.2024.106532 doi: 10.1016/j.frl.2024.106532

|

| [50] |

A. Sokhanvar, S. Hammoudeh, Comparative analysis of responses of risky and safe haven assets to stock market risk before and after the yield curve inversions in the US, Int. Rev. Econ. Financ., 94 (2024), 103376. https://doi.org/10.1016/j.iref.2024.103376 doi: 10.1016/j.iref.2024.103376

|

| [51] |

T. C. Chiang, Can gold or silver be used as a hedge against policy uncertainty and COVID-19 in the Chinese market?, China Financ. Rev. Int., 12 (2022), 571–600. https://doi.org/10.1108/CFRI-12-2021-0232 doi: 10.1108/CFRI-12-2021-0232

|

| [52] |

D. G. Baur, L. A. Smales, Hedging geopolitical risk with precious metals, J. Bank. Financ., 117 (2020), 105823. https://doi.org/10.1016/j.jbankfin.2020.105823 doi: 10.1016/j.jbankfin.2020.105823

|

| [53] |

B. Elie, J. Naji, A. Dutta, G. S. Uddin, Gold and crude oil as safe-haven assets for clean energy stock indices: Blended copulas approach, Energy, 178 (2019), 544–553. https://doi.org/10.1016/j.energy.2019.04.155 doi: 10.1016/j.energy.2019.04.155

|

| [54] |

S. Skapa, Commodities as a tool of risk diversification, Equilibrium, 8 (2013), 65–77. https://doi.org/10.12775/EQUIL.2013.014 doi: 10.12775/EQUIL.2013.014

|

| [55] |

B. Li, Speculation, risk aversion, and risk premiums in the crude oil market, J. Bank. Financ., 95 (2018), 64–81. https://doi.org/10.1016/j.jbankfin.2018.06.002 doi: 10.1016/j.jbankfin.2018.06.002

|

| [56] |

N. A. Kyriazis, S. Papadamou, P. Tzeremes, Are benchmark stock indices, precious metals or cryptocurrencies efficient hedges against crises?, Econ. Model., 128 (2023), 106502. https://doi.org/10.1016/j.econmod.2023.106502 doi: 10.1016/j.econmod.2023.106502

|

| [57] |

R. M. Dias, M. Chambino, N. Teixeira, P. Alexandre, P. Heliodoro, Balancing portfolios with metals: A safe haven for green energy investors?, Energies, 16 (2023), 7197. https://doi.org/10.3390/en16207197 doi: 10.3390/en16207197

|

| [58] |

S. W. Kim, B. S. Lee, Stock returns, asymmetric volatility, risk aversion, and business cycle: Some new evidence, Econ. Inq., 46 (2008), 131–148. https://doi.org/10.1111/j.1465-7295.2007.00066.x doi: 10.1111/j.1465-7295.2007.00066.x

|

| [59] |

B. J. Cohen, The yuan tomorrow? Evaluating China's currency internationalisation strategy, New Polit. Econ., 17 (2012), 361–371. https://doi.org/10.1080/13563467.2011.615915 doi: 10.1080/13563467.2011.615915

|

| [60] |

R. J. Caballero, E. Farhi, P. O. Gourinchas, The safe assets shortage conundrum, J. Econ. Perspect., 31 (2017), 29–46. https://doi.org/10.1257/jep.31.3.29 doi: 10.1257/jep.31.3.29

|

| [61] |

L. Peritz, R. Weldzius, R. Rogowski, T. Flaherty, Enduring the great recession: Economic integration in the European union, Rev. Int. Organ., 17 (2022), 175–203. https://doi.org/10.1007/s11558-020-09410-0 doi: 10.1007/s11558-020-09410-0

|

| [62] |

C. Jin, X. Tian, Enhanced safe-haven status of Bitcoin: Evidence from the silicon valley bank collapse, Financ. Res. Lett., 59 (2024), 104689. https://doi.org/10.1016/j.frl.2023.104689 doi: 10.1016/j.frl.2023.104689

|

| [63] |

K. J. Lansing, S. F. LeRoy, Risk aversion, investor information and stock market volatility, Eur. Econ. Rev., 70 (2014), 88–107. https://doi.org/10.1016/j.euroecorev.2014.03.009 doi: 10.1016/j.euroecorev.2014.03.009

|

| [64] |

D. A. Guenther, R. Sansing, The effect of tax-exempt investors and risk on stock ownership and expected returns, Account. Rev., 85 (2010), 849–875. https://doi.org/10.2308/accr.2010.85.3.849 doi: 10.2308/accr.2010.85.3.849

|

| [65] |

C. Wu, C. H. Yu, Risk aversion and the yield of corporate debt, J. Bank. Financ., 20 (1996), 267–281. https://doi.org/10.1016/0378-4266(94)00099-9 doi: 10.1016/0378-4266(94)00099-9

|

| [66] |

J. L. Glascock, D. Michayluk, K. Neuhauser, The riskiness of REITs surrounding the October 1997 stock market decline, J. Real Estate Financ., 28 (2004), 339–354. https://doi.org/10.1023/B:REAL.0000018786.39272.fa doi: 10.1023/B:REAL.0000018786.39272.fa

|

| [67] |

R. Demirer, A. Yüksel, A. Yüksel, On the hedging benefits of reits: The role of risk aversion and market states, Econ. Bus. Lett., 10 (2021), 126–132. https://doi.org/10.17811/ebl.10.2.2021.126-132 doi: 10.17811/ebl.10.2.2021.126-132

|

| [68] |

J. Y. Campbell, J. H. Cochrane, By force of habit: A consumption-based explanation of aggregate stock market behavior, J. Polit. Econ., 107 (1999), 205–251. https://doi.org/10.1086/250059 doi: 10.1086/250059

|

| [69] |

M. K. Brunnermeier, L. H. Pedersen, Market liquidity and funding liquidity, Rev. Financ. Stud., 22 (2009), 2201–2238. https://doi.org/10.1093/rfs/hhn098 doi: 10.1093/rfs/hhn098

|

| [70] |

R. J. Caballero, A. Krishnamurthy, Collective risk management in a flight to quality episode, J. Financ., 63 (2008), 2195–2230. https://doi.org/10.1111/j.1540-6261.2008.01394.x doi: 10.1111/j.1540-6261.2008.01394.x

|

| [71] |

D. G. Baur, K. Hong, A. D. Lee, Bitcoin: Medium of exchange or speculative assets?, J. Int. Financ. Mark. I., 54 (2018), 177–189. https://doi.org/10.1016/j.intfin.2017.12.004 doi: 10.1016/j.intfin.2017.12.004

|

| [72] |

S. Choi, J. Shin, Bitcoin: An inflation hedge but not a safe haven, Financ. Res. Lett., 46 (2022), 102379. https://doi.org/10.1016/j.frl.2021.102379 doi: 10.1016/j.frl.2021.102379

|

| [73] |

G. Koop, M. H. Pesaran, S. M. Potter, Impulse response analysis in nonlinear multivariate models, J. Econometrics, 74 (1996), 119–147. https://doi.org/10.1016/0304-4076(95)01753-4 doi: 10.1016/0304-4076(95)01753-4

|

| [74] |

H. H. Pesaran, Y. Shin, Generalized impulse response analysis in linear multivariate models, Econ. Lett., 58 (1998), 17–29. https://doi.org/10.1016/S0165-1765(97)00214-0 doi: 10.1016/S0165-1765(97)00214-0

|

| [75] |

F. X. Diebold, K. Yilmaz, Better to give than to receive: Predictive directional measurement of volatility spillovers, Int. J. Forecast., 28 (2012), 57–66. https://doi.org/10.1016/j.ijforecast.2011.02.006 doi: 10.1016/j.ijforecast.2011.02.006

|

| [76] |

R. Koenker, G. Bassett Jr, Regression quantiles, Econometrica, 46 (1978), 33–50. https://doi.org/10.2307/1913643 doi: 10.2307/1913643

|

| [77] |

M. K. Brunnermeier, L. H. Pedersen, Market liquidity and funding liquidity, Rev. Financ. Stud., 22 (2009), 2201–2238. https://doi.org/10.1093/rfs/hhn098 doi: 10.1093/rfs/hhn098

|

| [78] |

J. B. Kim, L. Luo, H. Xie, Do dividends mitigate bad news hoarding, overinvestments, and stock price crash risk?, Account. Financ., 64 (2024), 3999–4038. https://doi.org/10.1111/acfi.13297 doi: 10.1111/acfi.13297

|

| [79] |

A. Belanes, F. Saâdaoui, A. Amirat, H. Rabbouch, Safety assessment of cryptocurrencies as risky assets during the COVID-19 pandemic, Physica A, 651 (2024), 130013. https://doi.org/10.1016/j.physa.2024.130013 doi: 10.1016/j.physa.2024.130013

|

| [80] |

M. Qadan, D. Kliger, N. Chen, Idiosyncratic volatility, the vix and stock returns, N. Am. J. Econ. Financ., 47 (2019), 431–441. https://doi.org/10.1016/j.najef.2018.06.003 doi: 10.1016/j.najef.2018.06.003

|

| [81] |

D. Bams, I. Honarvar, Vix and liquidity premium, Int. Rev. Financ. Anal., 74 (2021), 101655. https://doi.org/10.1016/j.irfa.2020.101655 doi: 10.1016/j.irfa.2020.101655

|

| [82] |

A. H. Elsayed, G. Gozgor, C. K. M. Lau, Risk transmissions between Bitcoin and traditional financial assets during the COVID-19 era: The role of global uncertainties, Int. Rev. Financ. Anal., 81 (2022), 102069. https://doi.org/10.1016/j.irfa.2022.102069 doi: 10.1016/j.irfa.2022.102069

|

| [83] |

B. Gaies, N. Chaâbane, N. Arfaoui, J. M. Sahut, On the resilience of cryptocurrencies: A quantile-frequency analysis of Bitcoin and ethereum reactions in times of inflation and financial instability, Res. Int. Bus. Financ., 70 (2024), 102302. https://doi.org/10.1016/j.ribaf.2024.102302 doi: 10.1016/j.ribaf.2024.102302

|

| [84] |

J. Annaert, M. De Ceuster, P. V. Roy, C. Vespro, What determines Euro area bank CDS spreads?, J. Int. Money Financ., 32 (2013), 444–461. https://doi.org/10.1016/j.jimonfin.2012.05.029 doi: 10.1016/j.jimonfin.2012.05.029

|

| [85] | T. Leung, R. Sircar, T. Zariphopoulou, Credit derivatives and risk aversion, In: Econometrics and Risk Management, Emerald Group Publishing Limited, 2008,275–291. https://doi.org/10.1016/S0731-9053(08)22011-6 |

| [86] |

A. M'beirick, S. Haddou, The asymmetric response of sovereign credit default swaps spreads to risk aversion, investor sentiment and monetary policy shocks, Int. Rev. Econ. Financ., 93 (2024), 244–272. https://doi.org/10.1016/j.iref.2024.03.064 doi: 10.1016/j.iref.2024.03.064

|

| [87] |

J. Yu, Y. Yuan, Investor sentiment and the mean-variance relation, J. Financ. Econ., 100 (2011), 367–381. https://doi.org/10.1016/j.jfineco.2010.10.011 doi: 10.1016/j.jfineco.2010.10.011

|

| [88] | A. Bandopadhyaya, A. L. Jones, Measuring investor sentiment in equity markets, In: Asset Management: Portfolio Construction, Performance and Returns, Springer, 2016,258–269. https://doi.org/10.1007/978-3-319-30794-7_11 |

| [89] |

S. N. Ung, B. Gebka, R. D. Anderson, An enhanced investor sentiment index, Eur. J. Financ., 30 (2024), 827–864. https://doi.org/10.1080/1351847X.2023.2247440 doi: 10.1080/1351847X.2023.2247440

|

Figures(11) / Tables(6)

Seung Ho Choi, Hayoung Choi, Sun-Yong Choi. Risk aversion, safe-haven assets, and Bitcoin's evolving role in global financial markets: Insights from quantile spillover analysis[J]. AIMS Mathematics, 2026, 11(1): 2481-2526. doi: 10.3934/math.2026101

DownLoad:

DownLoad: