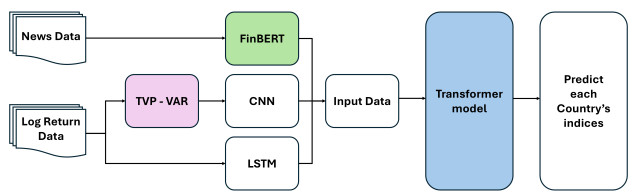

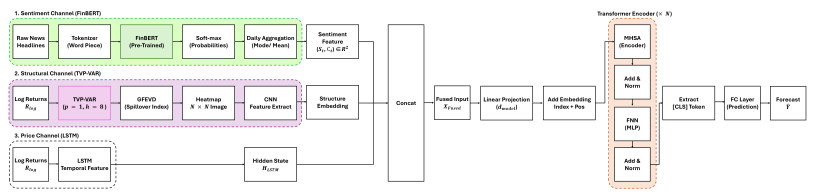

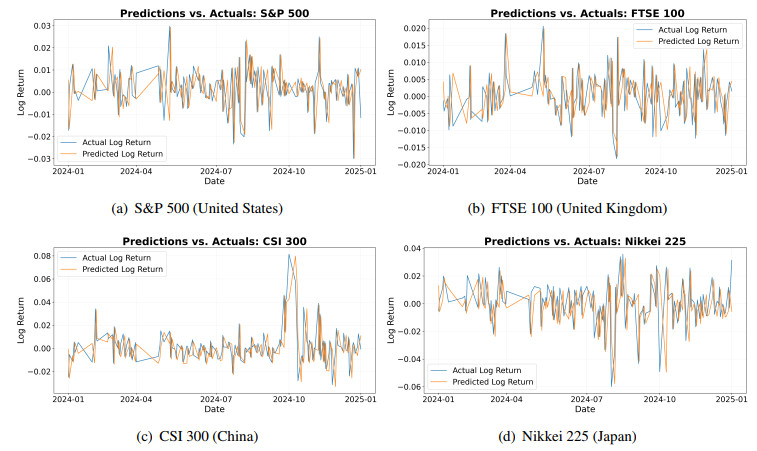

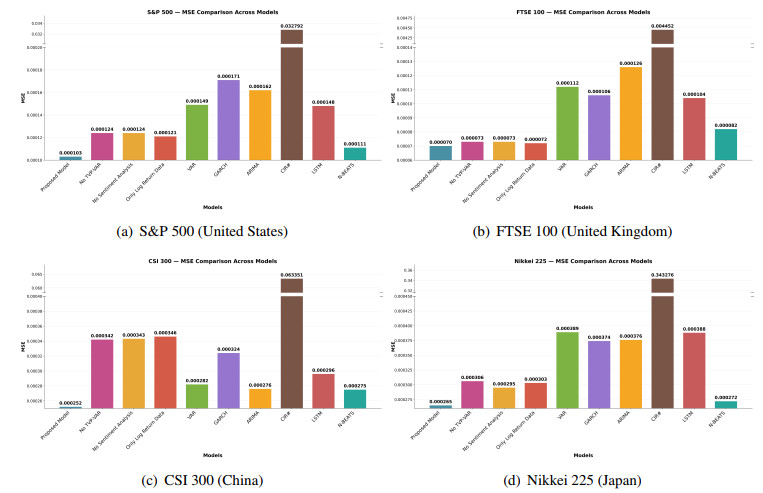

Traditional financial forecasting models are inherently limited as their sole reliance on price data causes them to overlook critical information such as market sentiment and dynamic inter-market interactions. To address this shortcoming, this study proposes a novel hybrid transformer model that integrates heterogeneous data sources. Specifically, our framework combines investor sentiment extracted from news headlines using FinBERT and dynamic changes in market structure analyzed with a TVP-VAR model, along with traditional log-return data. In forecasting experiments conducted on four major global stock indices (S&P 500, FTSE 100, CSI 300, and Nikkei 225), the proposed model consistently demonstrated superior performance compared to both single-data-source models and traditional benchmarks. We found that the inclusion of dynamic market structure information, derived from the TVP-VAR model, as a predictive variable was a decisive factor in improving forecasting accuracy. This research empirically validates that a multi-modal approach combining heterogeneous data can significantly enhance the precision of financial market forecasting.

Citation: Dong-Jun Kim, Eunjung Noh, Sun-Yong Choi. A hybrid transformer framework integrating sentiment and dynamic market structure for stock price movement forecasting[J]. AIMS Mathematics, 2026, 11(1): 977-1020. doi: 10.3934/math.2026043

Traditional financial forecasting models are inherently limited as their sole reliance on price data causes them to overlook critical information such as market sentiment and dynamic inter-market interactions. To address this shortcoming, this study proposes a novel hybrid transformer model that integrates heterogeneous data sources. Specifically, our framework combines investor sentiment extracted from news headlines using FinBERT and dynamic changes in market structure analyzed with a TVP-VAR model, along with traditional log-return data. In forecasting experiments conducted on four major global stock indices (S&P 500, FTSE 100, CSI 300, and Nikkei 225), the proposed model consistently demonstrated superior performance compared to both single-data-source models and traditional benchmarks. We found that the inclusion of dynamic market structure information, derived from the TVP-VAR model, as a predictive variable was a decisive factor in improving forecasting accuracy. This research empirically validates that a multi-modal approach combining heterogeneous data can significantly enhance the precision of financial market forecasting.

| [1] |

X. Zhang, Y. Zong, P. Du, S. Wang, J. Wang, Framework for multivariate carbon price forecasting: A novel hybrid model, J. Environ. Manage., 369 (2024), 122275. https://doi.org/10.1016/j.jenvman.2024.122275 doi: 10.1016/j.jenvman.2024.122275

|

| [2] |

L. Xie, Z. Chen, S. Yu, Deep convolutional transformer network for stock movement prediction, Electronics, 13 (2024), 4225. https://doi.org/10.3390/electronics13214225 doi: 10.3390/electronics13214225

|

| [3] |

A. Huang, L. Qiu, Z. Li, Applying deep learning method in TVP-VAR model under systematic financial risk monitoring and early warning, J. Comput. Appl. Math., 382 (2021), 113065. https://doi.org/10.1016/j.cam.2020.113065 doi: 10.1016/j.cam.2020.113065

|

| [4] |

A. Attarzadeh, M. Isayev, F. Irani, Dynamic interconnectedness and portfolio implications among cryptocurrency, gold, energy, and stock markets: A TVP-VAR approach, Sustain. Futures, 8 (2024), 100375. https://doi.org/10.1016/j.sftr.2024.100375 doi: 10.1016/j.sftr.2024.100375

|

| [5] |

J. Liu, H. Zhu, Z. Huang, L. Deng, Dynamic forecasting of exchange rate spillovers with TVP-VAR and deep learning models, Financ. Res. Lett., 86 (2025), 108677. https://doi.org/10.1016/j.frl.2025.108677 https://doi.org/10.1016/j.frl.2025.108677 doi: 10.1016/j.frl.2025.108677

|

| [6] |

J. Kim, H. S. Kim, S. Y. Choi, Forecasting the S&P 500 index using mathematical-based sentiment analysis and deep learning models: A FinBERT transformer model and LSTM, Axioms, 12 (2023), 835. https://doi.org/10.3390/axioms12090835 doi: 10.3390/axioms12090835

|

| [7] | M. A. B. Jeet, R. M. Haque, M. A. I. Sayem, A. Arman, R. M. Rahman, Using deep learning models and FinBERT to predict the stock price of top banks in the Dhaka Stock Exchange, In: 2024 IEEE/ACIS 24th International Conference on Computer and Information Science (ICIS), IEEE, 2024,121–126. https://doi.org/10.1109/ICIS61260.2024.10778363 |

| [8] |

H. D. Jung, B. Jang, Enhancing financial sentiment analysis ability of language model via targeted numerical change-related masking, IEEE Access, 12 (2024), 50809–50820. https://doi.org/10.1109/ACCESS.2024.3385855 doi: 10.1109/ACCESS.2024.3385855

|

| [9] |

L. Su, X. Zuo, R. Li, X. Wang, H. Zhao, B. Huang, A systematic review for transformer-based long-term series forecasting, Artif. Intell. Rev., 58 (2025), 80. https://doi.org/10.1007/s10462-024-11044-2 doi: 10.1007/s10462-024-11044-2

|

| [10] | W. Zhang, J. Huang, R. Wang, C. Wei, W. Huang, Y. Qiao, Integration of Mamba and Transformer - MAT for long-short range time series forecasting with application to weather dynamics, In: 2024 International Conference on Electrical, Communication and Computer Engineering (ICECCE), IEEE, 2024, 1–6. https://doi.org/10.1109/ICECCE63537.2024.10823516 |

| [11] |

S. A. Farimani, M. V. Jahan, A. M. Fard, An adaptive multimodal learning model for financial market price prediction, IEEE Access, 12 (2024), 121846–121863. https://doi.org/10.1109/ACCESS.2024.3441029 doi: 10.1109/ACCESS.2024.3441029

|

| [12] |

P. Chen, Z. Boukouvalas, R. Corizzo, A deep fusion model for stock market prediction with news headlines and time series data, Neural Comput. Appl., 36 (2024), 21229–21271. https://doi.org/10.1007/s00521-024-10303-1 doi: 10.1007/s00521-024-10303-1

|

| [13] | S. S. Begum, N. S. Fatima, M. Abbas, Enhancing stock market prediction with an LSTM-attention model integrating macroeconomic and sentiment features, In: 2024 International Conference on Innovative Computing, Intelligent Communication and Smart Electrical Systems (ICSES), IEEE, 2024, 1–6. https://doi.org/10.1109/ICSES63760.2024.10910478 |

| [14] | G. N. Rodrigues, M. N. H. Mir, M. S. M. Bhuiyan, M. Al Rafi, K. N. R. Fuad, M. S. Islam, et al., MiniBert24: A lightweight transformer-based model for stock market movement prediction, In: 2024 IEEE 3rd International Conference on Robotics, Automation, Artificial-Intelligence and Internet-of-Things (RAAICON), IEEE, 2024,293–298. |

| [15] | M. B. Mahendran, A. K. Gokul, P. Lakshmi, S. Pavithra, Comparative advances in financial sentiment analysis: A review of BERT, FinBert, and large language models, In: 2025 3rd International Conference on Intelligent Data Communication Technologies and Internet of Things (IDCIoT), IEEE, 2025, 39–45. https://doi.org/10.1109/IDCIOT64235.2025.10914764 |

| [16] | S. Yang, S. Yang, F. Mai, Financial semantic textual similarity: A new dataset and model, In: 2024 IEEE Symposium on Computational Intelligence for Financial Engineering and Economics (CIFEr), IEEE, 2024, 1–8. https://doi.org/10.1109/CIFEr62890.2024.10772793 |

| [17] | Y. Shen, P. K. Zhang, Financial sentiment analysis on news and reports using large language models and FinBert, In: 2024 IEEE 6th International Conference on Power, Intelligent Computing and Systems (ICPICS), IEEE, 2024,717–721. https://doi.org/10.1109/ICPICS62053.2024.10796670 |

| [18] |

O. Shobayo, S. Adeyemi-Longe, O. Popoola, B. Ogunleye, Innovative sentiment analysis and prediction of stock price using FinBERT, GPT-4 and logistic regression: A data-driven approach, Big Data and Cogn. Comput., 8 (2024), 143. https://doi.org/10.3390/bdcc8110143 doi: 10.3390/bdcc8110143

|

| [19] | S. B. Priya, M. Kumar, N. P. JD, N. Krithika, Advanced financial sentiment analysis using FinBERT to explore sentiment dynamics, In: 2025 3rd International Conference on Intelligent Data Communication Technologies and Internet of Things (IDCIoT), IEEE, 2025,889–897. https://doi.org/10.1109/IDCIOT64235.2025.10915080 |

| [20] |

D. Gabauer, R. Gupta, On the transmission mechanism of country-specific and international economic uncertainty spillovers: Evidence from a TVP-VAR connectedness decomposition approach, Econ. Lett., 171 (2018), 63–71. https://doi.org/10.1016/j.econlet.2018.07.007 doi: 10.1016/j.econlet.2018.07.007

|

| [21] |

K. Nyakurukwa, Y. Seetharam, Cross-country categorical economic policy uncertainty spillovers: Evidence from a conditional connectedness TVP-VAR framework, J. Finan. Econ. Policy, 15 (2023), 164–181. https://doi.org/10.1108/JFEP-10-2022-0256 doi: 10.1108/JFEP-10-2022-0256

|

| [22] |

L. Zhao, F. Wen, X. Wang, Interaction among China carbon emission trading markets: Nonlinear Granger causality and time-varying effect, Energ. Econ., 91 (2020), 104901. https://doi.org/10.1016/j.eneco.2020.104901 doi: 10.1016/j.eneco.2020.104901

|

| [23] |

B. Lucey, B. Ren, Time-varying tail risk connectedness among sustainability-related products and fossil energy investments, Energ. Econ., 126 (2023), 106812. https://doi.org/10.1016/j.eneco.2023.106812 doi: 10.1016/j.eneco.2023.106812

|

| [24] | B. Tang, D. S. Matteson, Probabilistic transformer for time series analysis, In: Advances in Neural Information Processing Systems, Curran Associates, Inc., 34 (2021), 23592–23608. |

| [25] | H. Cao, Z. Huang, T. Yao, J. Wang, H. He, Y. Wang, Inparformer: Evolutionary decomposition transformers with interactive parallel attention for long-term time series forecasting, In: Proceedings of the AAAI Conference on Artificial Intelligence, 37 (2023), 6906–6915. https://doi.org/10.1609/aaai.v37i6.25845 |

| [26] | S. Sridhar, S. Sanagavarapu, Multi-head self-attention transformer for Dogecoin price prediction, In: 2021 14th International Conference on Human System Interaction (HSI), IEEE, 2021, 1–6. https://doi.org/10.1109/HSI52170.2021.9538640 |

| [27] | Y. Hao, L. Dong, F. Wei, K. Xu, Self-attention attribution: Interpreting information interactions inside transformer, In: Proceedings of the AAAI Conference on Artificial Intelligence, 35 (2021), 12963–12971. https://doi.org/10.1609/aaai.v35i14.17533 |

| [28] | Y. Liu, H. Wu, J. Wang, M. Long, Non-stationary transformers: Exploring the stationarity in time series forecasting, In: Advances in Neural Information Processing Systems, Curran Associates, Inc., 35 (2022), 9881–9893. |

| [29] | H. Zhou, S. Zhang, J. Peng, S. Zhang, J. Li, H. Xiong, et al., Informer: Beyond efficient transformer for long sequence time-series forecasting, In: Proceedings of the AAAI conference on artificial intelligence, 35 (2021), 11106–11115. https://doi.org/10.1609/aaai.v35i12.17325 |

| [30] | R. Gupta, M. Chen, Sentiment analysis for stock price prediction, In: 2020 IEEE conference on multimedia information processing and retrieval (MIPR), IEEE, 2020,213–218. https://doi.org/10.1109/MIPR49039.2020.00051 |

| [31] |

Z. Jin, Y. Yang, Y. Liu, Stock closing price prediction based on sentiment analysis and LSTM, Neural Comput. Appl., 32 (2020), 9713–9729. https://doi.org/10.1007/s00521-019-04504-2 doi: 10.1007/s00521-019-04504-2

|

| [32] |

X. Li, P. Wu, W. Wang, Incorporating stock prices and news sentiments for stock market prediction: A case of Hong Kong, Inform. Process. Manag., 57 (2020), 102212. https://doi.org/10.1016/j.ipm.2020.102212 doi: 10.1016/j.ipm.2020.102212

|

| [33] | T. Sidogi, R. Mbuvha, T. Marwala, Stock price prediction using sentiment analysis, In: 2021 IEEE International Conference on Systems, Man, and Cybernetics (SMC), IEEE, 2021, 46–51. https://doi.org/10.1109/SMC52423.2021.9659283 |

| [34] |

N. Jing, Z. Wu, H. Wang, A hybrid model integrating deep learning with investor sentiment analysis for stock price prediction, Expert Syst. Appl., 178 (2021), 115019. https://doi.org/10.1016/j.eswa.2021.115019 doi: 10.1016/j.eswa.2021.115019

|

| [35] |

E. Ramos-Pérez, P. J. Alonso-González, J. J. Núñez-Velázquez, Multi-transformer: A new neural network-based architecture for forecasting S&P volatility, Mathematics, 9 (2021), 1794. https://doi.org/10.3390/math9151794 doi: 10.3390/math9151794

|

| [36] |

K. Cao, T. Zhang, J. Huang, Advanced hybrid LSTM-transformer architecture for real-time multi-task prediction in engineering systems, Sci. Rep., 14 (2024), 4890. https://doi.org/10.1038/s41598-024-55483-x doi: 10.1038/s41598-024-55483-x

|

| [37] |

S. Dhanasekaran, D. Gopal, J. Logeshwaran, N. Ramya, A. O. Salau, Multi-model traffic forecasting in smart cities using graph neural networks and transformer-based multi-source visual fusion for intelligent transportation management, Int. J. Intell. Transp., 22 (2024), 518–541. https://doi.org/10.1007/s13177-024-00413-4 doi: 10.1007/s13177-024-00413-4

|

| [38] | K. Karthika, P. Balasubramanie, S. Harishmitha, P. Shanmugapriya, T. Ramya, Deep learning based hybrid transformer model for stock price prediction, In: 2025 International Conference on Multi-Agent Systems for Collaborative Intelligence (ICMSCI), IEEE, 2025, 1603–1608. https://doi.org/10.1109/ICMSCI62561.2025.10894439 |

| [39] |

R. Engle, Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models, J. Bus. Econ. Stat., 20 (2002), 339–350. https://doi.org/10.1198/073500102288618487 doi: 10.1198/073500102288618487

|

| [40] | R. Engle, Anticipating correlations: A new paradigm for risk management, Princeton University Press, 2009. https://doi.org/10.1515/9781400830190 |

| [41] |

F. X. Diebold, K. Yilmaz, Better to give than to receive: Predictive directional measurement of volatility spillovers, Int. J. Forecasting, 28 (2012), 57–66. https://doi.org/10.1016/j.ijforecast.2011.02.006 doi: 10.1016/j.ijforecast.2011.02.006

|

| [42] |

N. Antonakakis, I. Chatziantoniou, D. Gabauer, Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions, J. Risk Financ. Manag., 13 (2020), 84. https://doi.org/10.3390/jrfm13040084 doi: 10.3390/jrfm13040084

|

| [43] |

N. Antonakakis, R. Kizys, Dynamic spillovers between commodity and currency markets, Int. Rev. Financ. Anal., 41 (2015), 303–319. https://doi.org/10.1016/j.irfa.2015.01.016 doi: 10.1016/j.irfa.2015.01.016

|

| [44] |

H. Wang, Z. Xie, D. K. Chiu, K. K. Ho, Multimodal market information fusion for stock price trend prediction in the pharmaceutical sector, Appl. Intell., 55 (2025), 77. https://doi.org/10.1007/s10489-024-05894-0 doi: 10.1007/s10489-024-05894-0

|

| [45] |

W. An, L. Wang, Y. R. Zeng, Social media-based multi-modal ensemble framework for forecasting soybean futures price, Comput. Electron. Agr., 226 (2024), 109439. https://doi.org/10.1016/j.compag.2024.109439 doi: 10.1016/j.compag.2024.109439

|

| [46] |

C. Li, Commodity demand forecasting based on multimodal data and recurrent neural networks for e-commerce platforms, Intell. Syst. Appl., 22 (2024), 200364. https://doi.org/10.1016/j.iswa.2024.200364 doi: 10.1016/j.iswa.2024.200364

|

| [47] |

W. Huang, J. Zhao, X. Wang, Model-driven multimodal LSTM-CNN for unbiased structural forecasting of European Union allowances open-high-low-close price, Energ. Econ., 132 (2024), 107459. https://doi.org/10.1016/j.eneco.2024.107459 doi: 10.1016/j.eneco.2024.107459

|

| [48] |

C. Hong, Q. He, Integrating financial knowledge for explainable stock market sentiment analysis via query-guided attention, Appl. Sci., 15 (2025), 6893. https://doi.org/10.3390/app15126893 doi: 10.3390/app15126893

|

| [49] |

G. Lombardo, A. Bertogalli, S. Consoli, D. R. Recupero, Natural language processing and deep learning for bankruptcy prediction: An end-to-end architecture, IEEE Access, 12 (2024), 151075–151091. https://doi.org/10.1109/ACCESS.2024.3476621 doi: 10.1109/ACCESS.2024.3476621

|

| [50] | X. Ding, Y. Zhang, T. Liu, J. Duan, Deep learning for event-driven stock prediction, In: Proceedings of the 24th International Conference on Artificial Intelligence, AAAI Press, 2015, 2327–2333. |

| [51] | K. Koh, The impact of investor sentiment on stock returns in developed and emerging markets: The case of US and South Korea, Emerg. Mark. Financ. Tr., 2025, 1–24. https://doi.org/10.1080/1540496X.2025.2588236 |

| [52] |

N. A. Boamah, Integration, investor protection rules and global informational inefficiency of emerging financial markets, SN Bus. Econ., 1 (2021), 82. https://doi.org/10.1007/s43546-021-00084-3 doi: 10.1007/s43546-021-00084-3

|

| [53] |

M. E. Hoque, M. A. S. Zaidi, Global and country-specific geopolitical risk uncertainty and stock return of fragile emerging economies, Borsa Istanb. Rev., 20 (2020), 197–213. https://doi.org/10.1016/j.bir.2020.05.001 doi: 10.1016/j.bir.2020.05.001

|

| [54] |

A. Sehl, M. Eder, News personalization and public service media: The audience perspective in three European countries, J. Media, 4 (2023), 322–338. https://doi.org/10.3390/journalmedia4010022 doi: 10.3390/journalmedia4010022

|

| [55] |

P. C. Tetlock, Giving content to investor sentiment: The role of media in the stock market, J. Finance, 62 (2007), 1139–1168. https://doi.org/10.1111/j.1540-6261.2007.01232.x doi: 10.1111/j.1540-6261.2007.01232.x

|

| [56] |

G. Birz, E. Devos, S. Dutta, D. Tsang, Is good news good and bad news bad in the REIT market?, J. Real Estate Portfolio Manag., 27 (2021), 43–62. https://doi.org/10.1080/10835547.2021.1967689 doi: 10.1080/10835547.2021.1967689

|

| [57] |

T. Loughran, B. McDonald, When is a liability not a liability? textual analysis, dictionaries, and 10-ks, J. Finance, 66 (2011), 35–65. https://doi.org/10.1111/j.1540-6261.2010.01625.x doi: 10.1111/j.1540-6261.2010.01625.x

|

| [58] |

C. Kearney, S. Liu, Textual sentiment in finance: A survey of methods and models, Int. Rev. Financ. Anal., 33 (2014), 171–185. https://doi.org/10.1016/j.irfa.2014.02.006 doi: 10.1016/j.irfa.2014.02.006

|

| [59] |

J. W. Kang, S. Y. Choi, Comparative investigation of GPT and FinBERT's sentiment analysis performance in news across different sectors, Electronics, 14 (2025), 1090. https://doi.org/10.3390/electronics14061090 doi: 10.3390/electronics14061090

|

| [60] |

J. P. Venugopal, A. A. V. Subramanian, G. Sundaram, M. Rivera, P. Wheeler, A comprehensive approach to bias mitigation for sentiment analysis of social media data, Appl. Sci., 14 (2024), 11471. https://doi.org/10.3390/app142311471 doi: 10.3390/app142311471

|

| [61] |

I. Ghosh, T. D. Chaudhuri, S. Sarkar, S. Mukhopadhyay, A. Roy, Macroeconomic shocks, market uncertainty and speculative bubbles: A decomposition-based predictive model of Indian stock markets, China Financ. Rev. Int., 15 (2025), 166–201. https://doi.org/10.1108/CFRI-09-2023-0237 doi: 10.1108/CFRI-09-2023-0237

|

| [62] |

M. L. Narayana, A. J. Kartha, A. K. Mandal, A. Suresh, A. C. Jose, Ensemble time series models for stock price prediction and portfolio optimization with sentiment analysis, J. Intell. Inform. Syst., 63 (2025), 1079–1103. https://doi.org/10.1007/s10844-025-00928-6 doi: 10.1007/s10844-025-00928-6

|

| [63] |

M. N. H. Mir, M. S. M. Bhuiyan, M. Al Rafi, G. N. Rodrigues, M. Mridha, M. A. Hamid, et al., Joint topic-emotion modeling in financial texts: A novel approach to investor sentiment and market trends, IEEE Access, 13 (2025), 28664–28677. https://doi.org/10.1109/ACCESS.2025.3538760 doi: 10.1109/ACCESS.2025.3538760

|

| [64] | R. Liu, J. Liang, H. Chen, Y. Hu, Analyst reports and stock performance: Evidence from the Chinese market, Asia-Pac. Financ. Mark., 2025, 1–26. https://doi.org/10.1007/s10690-025-09522-w |

| [65] |

X. L. Gong, H. Y. Ning, X. Xiong, Research on the cross-contagion between international stock markets and geopolitical risks: The two-layer network perspective, Financ. Innov., 11 (2025), 23. https://doi.org/10.1186/s40854-024-00687-3 doi: 10.1186/s40854-024-00687-3

|

| [66] |

S. D. Yeboah, S. K. Agyei, D. Korsah, M. P. Fumey, P. K. Akorsu, V. Adela, Geopolitical risk and exchange rate dynamics in Sub-Saharan Africa's emerging economies, Futur. Bus. J., 11 (2025), 78. https://doi.org/10.1186/s43093-025-00505-x doi: 10.1186/s43093-025-00505-x

|

| [67] |

Y. Ding, X. Zhu, R. Pan, B. Zhang, Network vector autoregression with time-varying nodal influence, Comput. Econ., 66 (2025), 4161–4187. https://doi.org/10.1007/s10614-024-10841-9 doi: 10.1007/s10614-024-10841-9

|

| [68] |

Q. Liu, C. Xu, Z. Xu, The impact of geopolitical risk on food prices: Evidence from the TVP-SV-VAR model, J. Econ. Financ., 49 (2025), 450–473. https://doi.org/10.1007/s12197-025-09710-4 doi: 10.1007/s12197-025-09710-4

|

| [69] |

H. Le, A. Bouteska, T. Sharif, M. Z. Abedin, Dynamic interlinkages between carbon risk and volatility of green and renewable energy: A TVP-VAR analysis, Res. Int. Bus. Financ., 69 (2024), 102278. https://doi.org/10.1016/j.ribaf.2024.102278 doi: 10.1016/j.ribaf.2024.102278

|

| [70] |

M. Yousfi, H. Bouzgarrou, Exploring interconnections and risk evaluation of green equities and bonds: Fresh perspectives from TVP-VAR model and wavelet-based VaR analysis, China Financ. Rev. Int., 15 (2025), 117–139. https://doi.org/10.1108/CFRI-05-2024-0237 doi: 10.1108/CFRI-05-2024-0237

|

| [71] |

F. Ahmadian-Yazdi, A. Sokhanvar, S. Roudari, A. K. Tiwari, Dynamics of the relationship between stock markets and exchange rates during quantitative easing and tightening, Financ. Innov., 11 (2025), 51. https://doi.org/10.1186/s40854-024-00694-4 doi: 10.1186/s40854-024-00694-4

|

| [72] | H. G. Souto, A. Moradi, Can transformers transform financial forecasting?, China Financ. Rev. Int., 2024. https://doi.org/10.1108/CFRI-01-2024-0032 |

| [73] |

J. Yang, P. Li, Y. Cui, X. Han, M. Zhou, Multi-sensor temporal fusion transformer for stock performance prediction: An adaptive Sharpe ratio approach, Sensors, 25 (2025), 976. https://doi.org/10.3390/s25030976 doi: 10.3390/s25030976

|

| [74] |

M. Mohseni, I. Mohammadzaman, Robust meta-reinforcement learning for autonomous spacecraft rendezvous with transformer networks under delayed observations, Int. J. Aeronaut. Space Sci., 26 (2025), 2724–2749. https://doi.org/10.1007/s42405-025-00917-7 doi: 10.1007/s42405-025-00917-7

|

| [75] |

D. Xiang, W. Yang, Z. Zhou, J. Zhang, J. Li, J. Ouyang, et al., DPMFformer: An underwater image enhancement network based on deep pooling and multi-scale fusion transformer, Earth Sci. Inform., 18 (2025), 61. https://doi.org/10.1007/s12145-024-01573-3 doi: 10.1007/s12145-024-01573-3

|

| [76] |

S. Li, Y. Sun, W. Yue, M. Yao, Y. Han, G. Gui, et al., A novel multi-scale time fusion transformer for long-range spectrum occupancy prediction, IEEE T. Veh. Technol., 74 (2025), 9299–9312. https://doi.org/10.1109/TVT.2025.3540920 doi: 10.1109/TVT.2025.3540920

|

| [77] |

S. Liu, X. Wang, An improved transformer based traffic flow prediction model, Sci. Rep., 15 (2025), 8284. https://doi.org/10.1038/s41598-025-92425-7 doi: 10.1038/s41598-025-92425-7

|

| [78] |

G. Campisi, S. Muzzioli, A. Zaffaroni, Nonlinear dynamics in asset pricing: The role of a sentiment index, Nonlinear Dynam., 105 (2021), 2509–2523. https://doi.org/10.1007/s11071-021-06724-5 doi: 10.1007/s11071-021-06724-5

|

| [79] |

G. Tedeschi, F. Caccioli, M. C. Recchioni, Taming financial systemic risk: Models, instruments and early warning indicators, J. Econ. Interact. Coor., 15 (2020), 1–7. https://doi.org/10.1007/s11403-019-00278-x doi: 10.1007/s11403-019-00278-x

|

| [80] |

P. Malo, A. Sinha, P. Korhonen, J. Wallenius, P. Takala, Good debt or bad debt: Detecting semantic orientations in economic texts, J. Assoc. Inf. Sci. Tech., 65 (2014), 782–796. https://doi.org/10.1002/asi.23062 doi: 10.1002/asi.23062

|

| [81] | D. Araci, FinBERT: Financial sentiment analysis with pre-trained language models, arXiv preprint, 2019. https://doi.org/10.48550/arXiv.1908.10063 |

| [82] | Z. Wang, T. Oates, Encoding time series as images for visual inspection and classification using tiled convolutional neural networks, In: Workshops at the twenty-ninth AAAI conference on artificial intelligence, vol. 1. AAAI, 2015, 000091–000096. |

| [83] |

O. B. Sezer, A. M. Ozbayoglu, Algorithmic financial trading with deep convolutional neural networks: Time series to image conversion approach, Appl. Soft Comput., 70 (2018), 525–538. https://doi.org/10.1016/j.asoc.2018.04.024 doi: 10.1016/j.asoc.2018.04.024

|

| [84] |

E. Hoseinzade, S. Haratizadeh, CNNpred: CNN-based stock market prediction using a diverse set of variables, Expert Syst. Appl., 129 (2019), 273–285. https://doi.org/10.1016/j.eswa.2019.03.029 doi: 10.1016/j.eswa.2019.03.029

|

| [85] |

S. Barra, S. M. Carta, A. Corriga, A. S. Podda, D. R. Recupero, Deep learning and time series-to-image encoding for financial forecasting, IEEE/CAA J. Automatic., 7 (2020), 683–692. https://doi.org/10.1109/JAS.2020.1003132 doi: 10.1109/JAS.2020.1003132

|

| [86] |

M. Davidovic, J. McCleary, News sentiment and stock market dynamics: A machine learning investigation, J. Risk Financ. Manag., 18 (2025), 412. https://doi.org/10.3390/jrfm18080412 doi: 10.3390/jrfm18080412

|

| [87] | G. Shashank, G. Pandey, S. G. Koolagudi, Time based sentiment analysis of financial headlines using recurrent neural network, In: 2025 International Conference on Artificial Intelligence and Data Engineering (AIDE), IEEE, 2025,752–756. https://doi.org/10.1109/AIDE64228.2025.10987536 |

| [88] |

S. R. Baker, N. Bloom, S. J. Davis, Measuring economic policy uncertainty, Q. J. Econ., 131 (2016), 1593–1636. https://doi.org/10.1093/qje/qjw024 doi: 10.1093/qje/qjw024

|

| [89] |

L. Pastor, P. Veronesi, Uncertainty about government policy and stock prices, J. Finance, 67 (2012), 1219–1264. https://doi.org/10.1111/j.1540-6261.2012.01746.x doi: 10.1111/j.1540-6261.2012.01746.x

|

| [90] |

G. Orlando, M. Bufalo, Interest rates forecasting: Between Hull and White and the CIR#-how to make a single-factor model work, J. Forecasting, 40 (2021), 1566–1580. https://doi.org/10.1002/for.2783 doi: 10.1002/for.2783

|

| [91] |

G. Orlando, M. Bufalo, Time series forecasting with the CIR# model: From hectic markets sentiments to regular seasonal tourism, Technol. Econ. Dev. Eco., 29 (2023), 1216–1238. https://doi.org/10.3846/tede.2023.19294 doi: 10.3846/tede.2023.19294

|

Figures(7) / Tables(14)

Dong-Jun Kim, Eunjung Noh, Sun-Yong Choi. A hybrid transformer framework integrating sentiment and dynamic market structure for stock price movement forecasting[J]. AIMS Mathematics, 2026, 11(1): 977-1020. doi: 10.3934/math.2026043

DownLoad:

DownLoad: