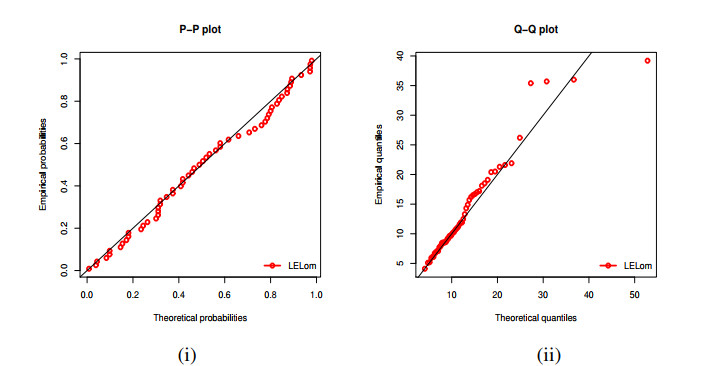

In this paper, a promising modeling strategy for data fitting is derived from a new general class of univariate continuous distributions. This class is governed by an original logarithmically-exponential one-parameter transformation which has the ability to enhance some modeling capabilities of any parental distribution. In relation to the current literature, it appears to be a "limit case" of the well-established truncated generalized Fréchet generated class. In addition, it offers a natural alternative to the famous odd inverse exponential generated class. Some special distributions are presented, with particular interest in a novel heavy-tailed three-parameter distribution based on the Lomax distribution. Functional equivalences, modes analysis, stochastic ordering, functional expansions, moment measures, information measures and reliability measures are derived. From generic or real data, our modeling strategy is based on the new class combined with the maximum likelihood approach. We apply this strategy to the introduced modified Lomax model. The efficiency of the three parameter estimates is validated by a simulation study. Subsequently, two referenced real data sets are adjusted according to the rules of the art; the first one containing environmental data and the second one, financial data. In particular, we show that the proposed model is preferable to four concurrents also derived from the Lomax model, including the odd inverse exponential Lomax model.

Citation: Abdulhakim A. Al-Babtain, Ibrahim Elbatal, Christophe Chesneau, Mohammed Elgarhy. On a new modeling strategy: The logarithmically-exponential class of distributions[J]. AIMS Mathematics, 2021, 6(7): 7845-7871. doi: 10.3934/math.2021456

In this paper, a promising modeling strategy for data fitting is derived from a new general class of univariate continuous distributions. This class is governed by an original logarithmically-exponential one-parameter transformation which has the ability to enhance some modeling capabilities of any parental distribution. In relation to the current literature, it appears to be a "limit case" of the well-established truncated generalized Fréchet generated class. In addition, it offers a natural alternative to the famous odd inverse exponential generated class. Some special distributions are presented, with particular interest in a novel heavy-tailed three-parameter distribution based on the Lomax distribution. Functional equivalences, modes analysis, stochastic ordering, functional expansions, moment measures, information measures and reliability measures are derived. From generic or real data, our modeling strategy is based on the new class combined with the maximum likelihood approach. We apply this strategy to the introduced modified Lomax model. The efficiency of the three parameter estimates is validated by a simulation study. Subsequently, two referenced real data sets are adjusted according to the rules of the art; the first one containing environmental data and the second one, financial data. In particular, we show that the proposed model is preferable to four concurrents also derived from the Lomax model, including the odd inverse exponential Lomax model.

| [1] | M. V. Aarset, How to identify bathtub hazard rate, IEEE Trans. Reliab., 36 (1987), 106–108. |

| [2] | M. A. Abdullah, H. A. Abdullah, Estimation of Lomax parameters based on generalized probability weighted moment, J. King Saud Univ. Sci., 22 (2010), 171–184. |

| [3] | A. Afaq, S. P. Ahmad, A. Ahmed, Bayesian Analysis of shape parameter of Lomax distribution under different loss functions, Int. J. Stat. Math., 2 (2010), 55–65. |

| [4] | M. Ahsanullah, Record values of Lomax distribution, Stat. Neerl., 41 (1991), 21–29. |

| [5] |

A. A. Al-Babtain, I. Elbatal, C. Chesneau, F. Jamal, The transmuted Muth generated class of distributions with applications, Symmetry, 12 (2020), 1677. doi: 10.3390/sym12101677

|

| [6] |

A. A. Al-Babtain, I. Elbatal, C. Chesneau, F. Jamal, Box-Cox gamma-G family of distributions: Theory and applications, Mathematics, 8 (2020), 1801. doi: 10.3390/math8101793

|

| [7] | S. Al-Marzouki, F. Jamal, C. Chesneau, M. Elgarhy, Topp-Leone odd Fréchet generated family of distributions with applications to Covid-19 data sets, Comput. Model Eng. Sci., 125 (2020), 437–458. |

| [8] | M. A. Aldahlan, F. Jamal, C. Chesneau, I. Elbatal, M. Elgarhy, Exponentiated power generalized Weibull power series family of distributions: Properties, estimation and applications, PloS One, 15 (2020), 1–25. |

| [9] | M. A. Aldahlan, F. Jamal, C. Chesneau, M. Elgarhy, I. Elbatal, The truncated Cauchy power family of distributions with inference and applications, Entropy, 22 (2020), 1–25. |

| [10] | A. M. Almarashi, M. Elgarhy, F. Jamal, C. Chesneau, The exponentiated truncated inverse Weibull generated family of distributions with applications, Symmetry, 12 (2020), 1–21. |

| [11] |

J. M. Amigo, S. G. Balogh, S. Hernandez, A brief review of generalized entropies, Entropy, 20 (2018), 813. doi: 10.3390/e20110813

|

| [12] |

M. Aslam, Z. Asghar, Z. Hussain, S. F. Shah, A modified T-X family of distributions: classical and Bayesian analysis, J. Taibah Univ. Sci., 14 (2020), 254–264. doi: 10.1080/16583655.2020.1732642

|

| [13] | M. A. Badr, I. Elbatal, F. Jamal, C. Chesneau, M. Elgarhy, The transmuted odd Fréchet-G family of distributions: Theory and applications, Mathematics, 8 (2020), 1–20. |

| [14] | N. Balakrishnan, M. Ahsanullah, Relations for single and product moments of record values from Lomax distribution, Sankhya B, 56 (1994), 140–146. |

| [15] | A. Balkema, L. de Haan, Residual life time at great age, Ann. Probab., 2 (1974), 792–804. |

| [16] | R. A. R. Bantan, C. Chesneau, F. Jamal, M. Elgarhy, On the analysis of new Covid-19 cases in Pakistan using an exponentiated version of the M family of distributions, Mathematics, 8 (2020), 1–20. |

| [17] | R. A. R. Bantan, F. Jamal, C. Chesneau, M. Elgarhy, Type II Power Topp-Leone generated family of distributions with statistical inference and applications, Symmetry, 12 (2020), 1–24. |

| [18] |

M. A. Beg, On the estimation of $P(Y <X)$ for the two parameter exponential distribution, Metrika, 27 (1980), 29–34. doi: 10.1007/BF01893574

|

| [19] | C. C. R. Brito, L. C. Rêgo, W. R. Oliveira, F. Gomes-Silva, Method for generating distributions and classes of probability distributions: The univariate case. Hacettepe J. Math. Stat., 48 (2019), 897–930. |

| [20] |

M. C. Bryson, Heavy-tailed distributions: Properties and tests, Technometrics, 16 (1974), 61–68. doi: 10.1080/00401706.1974.10489150

|

| [21] | G. Casella, R. L. Berger, Statistical Inference, Brooks/Cole Publishing Company: Bel Air, CA, USA, 1990. |

| [22] |

C. Chesneau, T. El Achi, Modified odd Weibull family of distributions: Properties and applications, J. Indian Soc. Prob. Stat., 21 (2020), 259–286. doi: 10.1007/s41096-020-00075-x

|

| [23] | G. M. Cordeiro, R. B. Silva, A. D. C. Nascimento, Recent Advances in Lifetime and Reliability Models, Bentham Sciences Publishers, Sharjah, UAE, 2020. |

| [24] | A. El-Bassiouny, N. Abdo, H. Shahen, Exponential Lomax distribution, Int. J. Comput. Appl., 121 (2015), 24–29. |

| [25] | W. Gilchrist, Statistical Modelling with Quantile Functions, CRC Press, Abingdon, 2000. |

| [26] |

M. A. Haq, M. Elgarhy, The odd Fréchet-G family of probability distributions, J. Stat. Appl. Prob., 7 (2018), 189–203. doi: 10.18576/jsap/070117

|

| [27] | F. Jamal, C. Chesneau, M. Elgarhy, Type II general inverse exponential family of distributions, J. Stat. Manage. Syst., 23 (2020), 617–641. |

| [28] |

D. Kumar, U. Singh, S. K. Singh, Life time distribution: Derived from some minimum guarantee distribution, Sohag J. Math., 4 (2017), 7–11. doi: 10.18576/sjm/040102

|

| [29] |

A. J. Lemonte, G. M. Cordeiro, An extended Lomax distribution, Statistics, 47 (2013), 800–816. doi: 10.1080/02331888.2011.568119

|

| [30] | M. Mead, A new generalization of Burr XII distribution, J. Stat.: Adv. Theo. Appl., 12 (2014), 53–71. |

| [31] |

N. U. Nair, P. G. Sankaran, Quantile based reliability analysis, Commun. Stat. Theory Methods, 38 (2009), 222–232. doi: 10.1080/03610920802187430

|

| [32] | M. A. Nasir, M. H. Tahir, C. Chesneau, F. Jamal, M. A. A. Shah, The odd generalized gamma-G family of distributions: Properties, regressions and applications, Statistica, 80 (2020), 3–38. |

| [33] | S. Nasiru, Extended odd Fréchet-G family of distributions, J. Probab. Stat., 1 (2018), 1–12. |

| [34] | D. Bates, J. Chambers, P. Dalgaard, S. Falcon, R Development Core Team, R: A language and environment for statistical computing, R Foundation for Statistical Computing, Vienna, Austria, ISBN 3-900051-07-0, Available from: http://www.R-project.org, 2005. |

| [35] |

E. A. Rady, W. A. Hassanein, T. A. Elhaddad, The power Lomax distribution with an application to bladder cancer data, SpringerPlus, 5 (2016), 1838. doi: 10.1186/s40064-016-3464-y

|

| [36] | A. Rényi, On measures of entropy and information, Proc. 4th Berkeley symposium on mathematical statistics and probability, 1 (1960), 47–561. |

| [37] | M. Shaked, J. G. Shanthikumar, Stochastic Orders, Wiley, New York, N.Y., USA, 2007. |

| [38] | M. H. Tahir, G. M. Cordeiro, Compounding of distributions: A survey and new generalized classes, J. Stat. Distrib. Appl., 3 (2016), 1–35. |

| [39] |

C. Tsallis, Possible generalization of Boltzmann-Gibbs statistics, J. Stat. Phys., 52 (1988), 479–487. doi: 10.1007/BF01016429

|

| [40] |

M. A. J. Van Montfort, On testing that the distribution of extremes is of type I when type II is the alternative, J. Hydrol., 11 (1970), 421–427. doi: 10.1016/0022-1694(70)90006-5

|

| [41] | H. M. Yousof, M. Rasekhi, M. Alizadeh, G. G. Hamedani, The Marshall-Olkin exponentiated generalized G family of distributions: properties, applications and characterizations, J. Nonlinear Sci. Appl., 13 (2020), 34–52. |

| [42] | R. A. ZeinEldin, C. Chesneau, F. Jamal, M. Elgarhy, A. M. Almarashi, S. Al-Marzouki, Truncated generalized Fréchet generated family of distributions with applications, Comput. Model Eng. Sci., 126 (2021), 791–819. |

Figures(5) / Tables(9)

Abdulhakim A. Al-Babtain, Ibrahim Elbatal, Christophe Chesneau, Mohammed Elgarhy. On a new modeling strategy: The logarithmically-exponential class of distributions[J]. AIMS Mathematics, 2021, 6(7): 7845-7871. doi: 10.3934/math.2021456

DownLoad:

DownLoad: