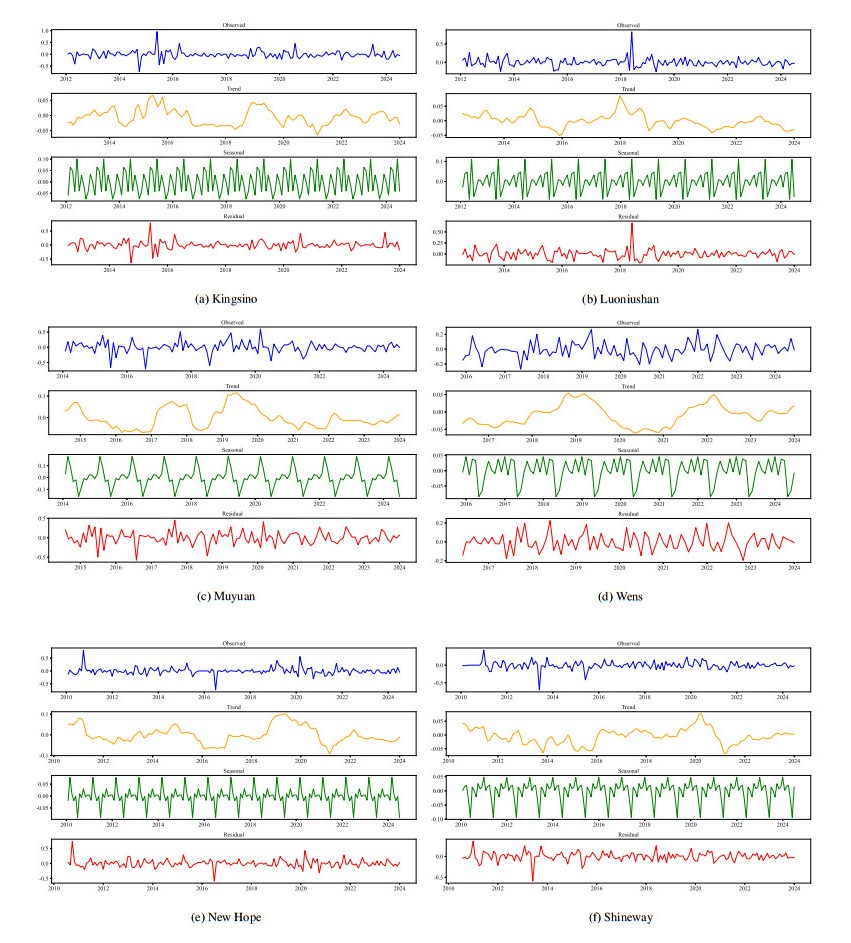

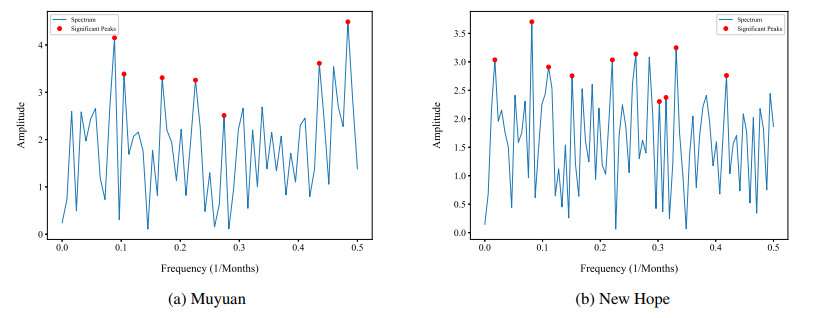

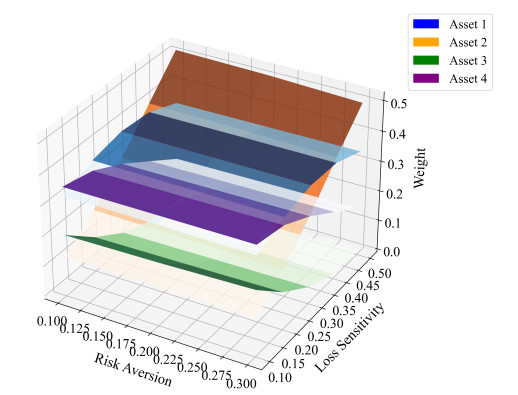

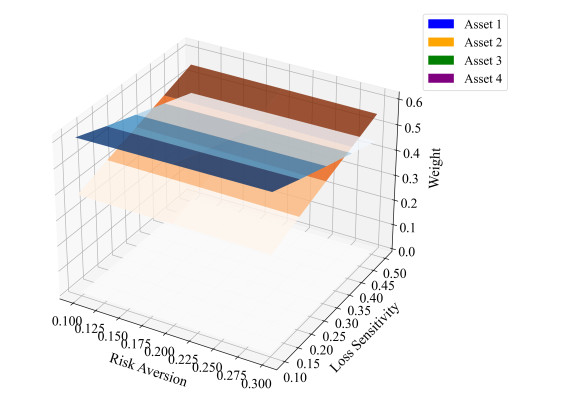

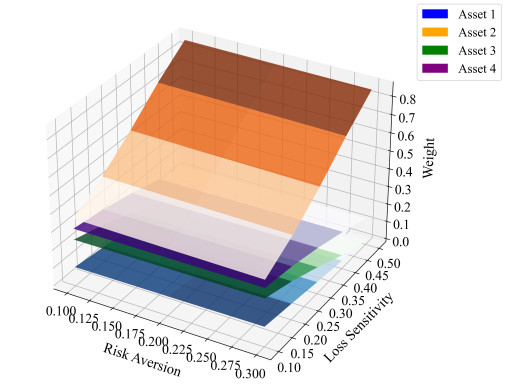

This study focused on the optimal strategy of livestock stock portfolios, where several representative livestock stocks were selected to construct portfolios and their time-series characteristics were explored through time-series analysis methods, including spectral analysis to identify periodic and non-periodic characteristics in stock returns. Based on modern portfolio theory, we proposed a novel utility function that integrates conditional value at risk (CVaR), risk aversion, and loss sensitivity into the classical utility model. Combined with the historical return data, we estimated the specific expressions of each index about the weight vector, and calculated the optimal weight allocation of the portfolio in different periods through the gradient descent method for investors with different degrees of risk aversion and loss sensitivity. The results show that non-periodic stocks have a relative advantage in terms of expected return and volatility control, and as investors' risk aversion increases, the investment weights are gradually tilted toward low-volatility stocks. This study provides empirical support for the investment strategy of livestock stocks, and provides a reference for investors to achieve a balance between risk control and return optimization in a complex and volatile market environment.

Citation: Ziyue Liu, Sheng Zhu, Haixin Qian. Time-series characteristics and optimal investment strategies for livestock stocks[J]. Big Data and Information Analytics, 2025, 9: 68-91. doi: 10.3934/bdia.2025004

This study focused on the optimal strategy of livestock stock portfolios, where several representative livestock stocks were selected to construct portfolios and their time-series characteristics were explored through time-series analysis methods, including spectral analysis to identify periodic and non-periodic characteristics in stock returns. Based on modern portfolio theory, we proposed a novel utility function that integrates conditional value at risk (CVaR), risk aversion, and loss sensitivity into the classical utility model. Combined with the historical return data, we estimated the specific expressions of each index about the weight vector, and calculated the optimal weight allocation of the portfolio in different periods through the gradient descent method for investors with different degrees of risk aversion and loss sensitivity. The results show that non-periodic stocks have a relative advantage in terms of expected return and volatility control, and as investors' risk aversion increases, the investment weights are gradually tilted toward low-volatility stocks. This study provides empirical support for the investment strategy of livestock stocks, and provides a reference for investors to achieve a balance between risk control and return optimization in a complex and volatile market environment.

| [1] |

Fama EF, French KR, (1988) Permanent and temporary components of stock prices. J Polit Econ 96: 246–273. https://doi.org/10.1086/261535 doi: 10.1086/261535

|

| [2] |

Gibbons MR, Hess P, (1981) Day of the week effects and asset returns. J Bus 54: 579–596. https://doi.org/10.1086/296147 doi: 10.1086/296147

|

| [3] | Box GEP, Jenkins GM, Reinsel GC, (2015) Time Series Analysis: Forecasting and Control, Wiley. https://doi.org/10.1111/jtsa.12194 |

| [4] | Hyndman RJ, Athanasopoulos G, (2018) Forecasting: Principles and Practice, OTexts. |

| [5] |

Schneider L, Tavin B, (2024) Seasonal volatility in agricultural markets: Modelling and empirical investigations. Ann Oper Res 334: 7–58. https://doi.org/10.1007/s10479-021-04241-7 doi: 10.1007/s10479-021-04241-7

|

| [6] |

Arismendi JC, Back J, Prokopczuk M, Paschke R, Rudolf M, (2016) Seasonal stochastic volatility: implications for the pricing of commodity options. J Bank Finance 66: 53–65. https://doi.org/10.1086/261535 doi: 10.1086/261535

|

| [7] | Vasicek O, Weber T, Leung SKL, (2020) Dynamic portfolio optimization with Kalman filter-based state-space models. J Risk 22: 215–234. |

| [8] | Liang F, Zhao X, (2022) Quantile autoregression in financial risk analysis. J Financ Econ 34: 92–105. |

| [9] |

Paul RK, Das T, Yeasin M, (2023) Ensemble of time series and machine learning model for forecasting volatility in agricultural prices. Natl Acad Sci Lett 46: 67–82. https://doi.org/10.1007/s40009-023-01218-x doi: 10.1007/s40009-023-01218-x

|

| [10] |

Markowitz HM, (1952) Portfolio selection. J Finance 7: 77–91. https://doi.org/10.1111/j.1540-6261.1952.tb01525.x doi: 10.1111/j.1540-6261.1952.tb01525.x

|

| [11] | Arrow KJ, (1971) Essays in the Theory of Risk-Bearing, Markham Publishing Co, Chicago. |

| [12] |

Pratt JW, (1964) Risk aversion in the small and in the large. Econometrica 32: 122–136. https://doi.org/10.2307/1913738 doi: 10.2307/1913738

|

| [13] | Huang CF, Litzenberger RH, (1988) Foundations for Financial Economics, North-Holland. |

| [14] |

Kahneman D, Tversky A, (1979) Prospect theory: An analysis of decision under risk. Econometrica 47: 363–391. https://doi.org/10.2307/1914185 doi: 10.2307/1914185

|

| [15] |

Tversky A, Kahneman D, (1992) Advances in prospect theory: Cumulative representation of uncertainty. J Risk Uncertain 5: 297–323. https://doi.org/10.1007/BF00122574 doi: 10.1007/BF00122574

|

| [16] |

Almansour BY, Elkrghli S, Almansour AY, (2023) Behavioral finance factors and investment decisions: A mediating role of risk perception. Cogent Econ Finance 11: 2239032. https://doi.org/10.1080/23322039.2023.2239032 doi: 10.1080/23322039.2023.2239032

|

| [17] |

Harris J, Mazibasz M, (2022) Behavioral preferences and memory effects in dynamic portfolio allocation. J Behav Finance 23: 55–72. https://doi.org/10.1080/15427560.2021.1996646 doi: 10.1080/15427560.2021.1996646

|

| [18] | Chiu WY, (2024) Hierarchical heterogeneous risk aversion and dynamic portfolio optimization. J Financ Econ 41: 150–169. |

| [19] |

Alexander GJ, Baptista AM, (2004) A comparison of VaR and CVaR constraints on portfolio selection with the mean-variance model. Manag Sci 50: 1261–1273. https://doi.org/10.1287/mnsc.1040.0201 doi: 10.1287/mnsc.1040.0201

|

| [20] |

Kibzun AI, Vagin VN, (2003) Comparison of VaR and CVaR criteria. J Autom Remote Control 64: 1154–1164. https://doi.org/10.1023/A:1024794420632 doi: 10.1023/A:1024794420632

|

| [21] |

Rockafellar RT, Uryasev S, (2000) Optimization of conditional value-at-risk. J Risk 2: 21–42. https://doi.org/10.21314/JOR.2000.038 doi: 10.21314/JOR.2000.038

|

| [22] |

Kartik K, Robert R, (2018) Comparing VaR and CVaR for portfolio optimization: A review. J Financ Risk Manag 10: 45–65. https://doi.org/10.1111/jfrm.12145 doi: 10.1111/jfrm.12145

|

| [23] |

Pavlikov K, Uryasev S, (2014) CVaR optimization for portfolio with tail risk constraints. J Portf Manag 40: 100–120. https://doi.org/10.3905/jpm.2014.40.2.100 doi: 10.3905/jpm.2014.40.2.100

|

| [24] |

Benati S, Conde E, (2022) A relative robust approach on expected returns with bounded CVaR for portfolio selection. Eur J Oper Res 296: 332–352. https://doi.org/10.1016/j.ejor.2021.04.038 doi: 10.1016/j.ejor.2021.04.038

|

| [25] |

Dudek G, (2023) STD: A seasonal-trend-dispersion decomposition of time series. IEEE Trans Knowl Data Eng 35: 10339–10350. https://doi.org/10.1109/TKDE.2023.3268125 doi: 10.1109/TKDE.2023.3268125

|

| [26] |

Linsmeier TJ, Pearson ND, (2000) Value at risk. Financ Analysts J 56: 47–67. https://doi.org/10.2469/faj.v56.n2.2343 doi: 10.2469/faj.v56.n2.2343

|

| [27] | Goodfellow I, Bengio Y, Courville A, (2016) Deep Learning, MIT Press. |

| [28] | Nocedal J, Wright S, (2006) Numerical Optimization, Springer. https://doi.org/10.1007/978-0-387-40065-5 |

| [29] | Harvey AC, (1993) Time Series Models, Harvester Wheatsheaf. |

| [30] | Priestley MB, (1981) Spectral Analysis and Time Series, Academic Press. |

| [31] |

Stoffer DS, Bloomfield P, (2000) Fourier analysis of time series: an introduction. J Am Stat Assoc 452: 4–12. https://doi.org/10.2307/2669794 doi: 10.2307/2669794

|

Figures(5) / Tables(15)

Ziyue Liu, Sheng Zhu, Haixin Qian. Time-series characteristics and optimal investment strategies for livestock stocks[J]. Big Data and Information Analytics, 2025, 9: 68-91. doi: 10.3934/bdia.2025004

DownLoad:

DownLoad: