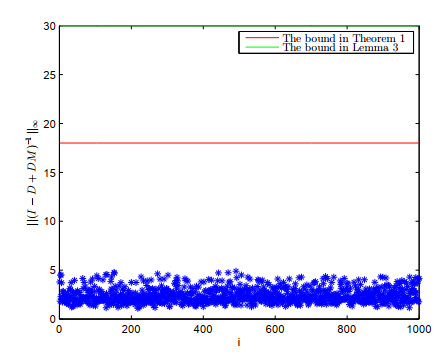

$ S $-$ SDDS $-$ B $ matrices is a subclass of $ P $-matrices which contains $ B $-matrices. New error bound of the linear complementarity problem for $ S $-$ SDDS $-$ B $ matrices is presented, which improves the corresponding result in [

Citation: Lanlan Liu, Pan Han, Feng Wang. New error bound for linear complementarity problem of $ S $-$ SDDS $-$ B $ matrices[J]. AIMS Mathematics, 2022, 7(2): 3239-3249. doi: 10.3934/math.2022179

$ S $-$ SDDS $-$ B $ matrices is a subclass of $ P $-matrices which contains $ B $-matrices. New error bound of the linear complementarity problem for $ S $-$ SDDS $-$ B $ matrices is presented, which improves the corresponding result in [

| [1] |

M. García-Esnaola, J. M. Pe$\tilde{n}$a, Error bounds for linear complementarity problems for $B$-matrices, Appl. Math. Lett., 22 (2009), 1071–1075. doi: 10.1016/j.aml.2008.09.001. doi: 10.1016/j.aml.2008.09.001

|

| [2] | K. G. Murty, F. T. Yu, Linear complementarity, linear and nonlinear programming, Berlin: Heldermann, 1988. |

| [3] | R. W. Cottle, J. S. Pang, R. E. Stone, The linear complementarity problem, Boston: Academic Press, 1992. |

| [4] |

Z. Q. Luo, P. Tseng, On the linear convergence of descent methods for convex essentially smooth minimization, SIAM J. Control Optim., 30 (1992), 408–425. doi: 10.1137/0330025. doi: 10.1137/0330025

|

| [5] |

Z. Q. Luo, P. Tseng, Error bound and convergence analysis of matrix splitting algorithms for the affine variational inequality problem, SIAM J. Optim., 2 (1992), 43–54. doi: 10.1137/0802004. doi: 10.1137/0802004

|

| [6] |

J. S. Pang, A posteriori error bound for the linearly-constrained variational inequality problem, Math. Oper. Res., 12 (1987), 474–484. doi: 10.1287/moor.12.3.474. doi: 10.1287/moor.12.3.474

|

| [7] |

J. S. Pang, Inexact Newton methods for the nonlinear complementarity problem, Math. Program., 36 (1986), 54–71. doi: 10.1007/BF02591989. doi: 10.1007/BF02591989

|

| [8] |

X. J. Chen, S. H. Xiang, Computation of error bounds for $P$-matix linear complementary problems, Math. Program., 106 (2006), 513–525. doi: 10.1007/s10107-005-0645-9. doi: 10.1007/s10107-005-0645-9

|

| [9] |

L. Y. Kolotilina, Bounds for the inverses of generalized Nekrosov matrices, J. Math. Sci., 207 (2015), 786–794. doi: 10.1007/s10958-015-2401-x. doi: 10.1007/s10958-015-2401-x

|

| [10] | L. Cvetkovi$\acute{{c}}$, V. Kosti$\acute{{c}}$, R. S. Varga, A new Geršgorin-type eigenvalue inclusion set, Electron. T. Numer. Ana., 302 (2004), 73–80. |

| [11] |

T. Szulc, L. Cvetkovi$\acute{{c}}$, M. Nedovi$\acute{{c}}$, Scaling technique for partition-Nekrasov matrices, Appl. Math. Comput., 207 (2015), 201–208. doi: 10.1016/j.amc.2015.08.136. doi: 10.1016/j.amc.2015.08.136

|

| [12] |

L. Cvetkovi$\acute{c}$, V. Kosti$\acute{c}$, S. Rauški, A new subclass of $H$-matrices, Appl. Math. Comput., 208 (2009), 206–210. doi: 10.1016/j.amc.2008.11.037. doi: 10.1016/j.amc.2008.11.037

|

| [13] |

P. F. Dai, J. C. Li, Y. T. Li, C. Y. Zhang, Error bounds for linear complementarity problems of $QN$-matrices, Calcolo, 53 (2016), 647–657. doi: 10.1007/s10092-015-0167-7. doi: 10.1007/s10092-015-0167-7

|

| [14] |

L. Gao, Y. Q. Wang, C. Q. Li, New error bounds for the linear complementarity problem of $QN$-matrices, Numer. Algorithms, 77 (2018), 229–242. doi: 10.1007/s11075-017-0312-2. doi: 10.1007/s11075-017-0312-2

|

| [15] |

Z. W. Hou, X. Jing, L. Gao, New error bounds for linear complementarity problems of $\Sigma$-SDD matrices and SB-matirces, Open Math., 17 (2019), 1599–1614. doi: 10.1515/math-2019-0127. doi: 10.1515/math-2019-0127

|

| [16] |

P. F. Dai, Y. T. Li, C. J. Lu, New error bounds for the linear complementarity problem with an $SB$-matrix, Numer. Algorithms, 64 (2013), 741–757. doi: 10.1007/s11075-012-9691-6. doi: 10.1007/s11075-012-9691-6

|

| [17] |

M. García-Esnaola, J. M. Pe$\tilde{n}$a, Error bounds for linear complementarity problems involving $B^{S}$-matrices, Appl. Math. Lett., 25 (2012), 1379–1383. doi: 10.1016/j.aml.2011.12.006. doi: 10.1016/j.aml.2011.12.006

|

| [18] |

F. Wang, Error bounds for linear complementarity problem of weakly chained diagonally dominant $B$-matrices, J. Inequal. Appl., 2017 (2017), 1–8. doi: 10.1186/s13660-017-1303-5. doi: 10.1186/s13660-017-1303-5

|

| [19] |

P. F. Dai, Error bounds for linear complementarity problems of $DB$-matrices, Linear Algebra Appl., 434 (2011), 830–840. doi: 10.1016/j.laa.2010.09.049. doi: 10.1016/j.laa.2010.09.049

|

| [20] |

T. T. Chen, W. Li, X. P. Wu, S. Vong, Error bounds for linear complementarity problems of $MB$-matrices, Numer. Algorithms, 70 (2015), 341–356. doi: 10.1007/s11075-014-9950-9. doi: 10.1007/s11075-014-9950-9

|

| [21] |

C. Q. Li, Y. T. Li, Note on error bounds for linear complementarity problems for $B$-matrices, Appl. Math. Lett., 57 (2016), 108–113. doi: 10.1016/j.aml.2016.01.013. doi: 10.1016/j.aml.2016.01.013

|

| [22] |

C. Q. Li, M. T. Gan, S. R. Yang, A new error bounds for linear complementarity problems for $B$-matrices, Electron. J. Linear Al., 31 (2016), 476–484. doi: 10.13001/1081-3810.3250. doi: 10.13001/1081-3810.3250

|

| [23] |

M. García-Esnaola, J. M. Pe$\tilde{n}$a, A comparison of error bounds for linear complementarity problems of $H$-matrices, Linear Algebra Appl., 433 (2010), 956–964. doi: 10.1016/j.laa.2010.04.024. doi: 10.1016/j.laa.2010.04.024

|

| [24] |

C. Q. Li, Y. T. Li, Weakly chained diagonally dominant $B$-matrices and error bounds for linear complementarity problem, Numer. Algorithms, 73 (2016), 985–998. doi: 10.1007/s11075-016-0125-8. doi: 10.1007/s11075-016-0125-8

|

| [25] |

D. Sun, F. Wang, New error bounds for linear complementarity problem of weakly chained diagonally dominant $B$-matrices, Open Math., 15 (2017), 978–986. doi: 10.1515/math-2017-0080. doi: 10.1515/math-2017-0080

|

| [26] |

L. Y. Kolotilina, Some bounds for inverses involving matrix sparsity pattern, J. Math. Sci., 249 (2020), 242–255. doi: 10.1007/s10958-020-04938-3. doi: 10.1007/s10958-020-04938-3

|

| [27] |

J. M. Pe$\tilde{n}$a, A class of $P$-matrix with applications to localization of the eigenvalues of a real matrix, SIAM J. Matrix Anal. Appl., 22 (2001), 1027–1037. doi: 10.1137/S0895479800370342. doi: 10.1137/S0895479800370342

|

Figures(1)

Lanlan Liu, Pan Han, Feng Wang. New error bound for linear complementarity problem of $ S $-$ SDDS $-$ B $ matrices[J]. AIMS Mathematics, 2022, 7(2): 3239-3249. doi: 10.3934/math.2022179

DownLoad:

DownLoad: