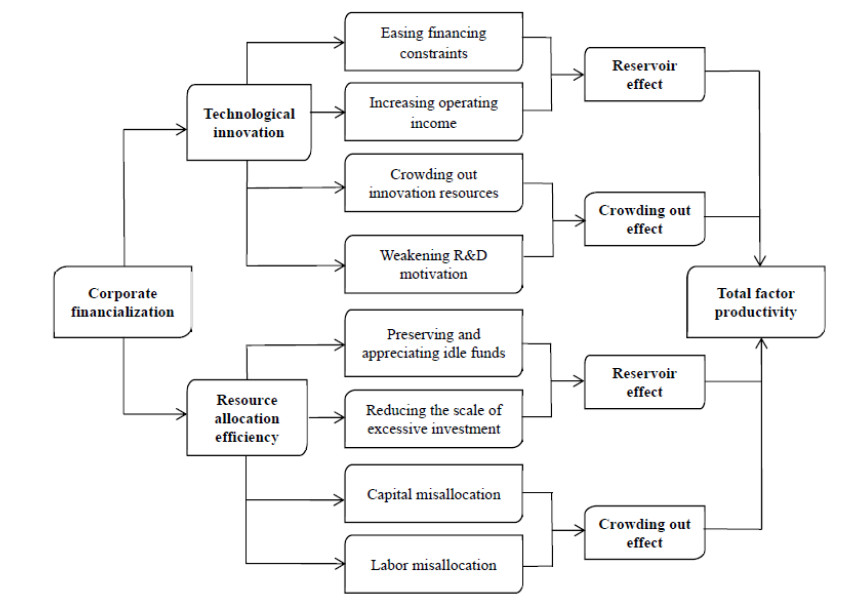

This paper examines the effects and mechanism of the financialization of manufacturing enterprises on total factor productivity (TFP). Thus, it provides evidence of the economic consequences of corporate financialization from the perspective of productivity. Using the panel data of China's listed manufacturing companies from 2007 to 2018, the level of corporate financialization is measured using the proportion of financial assets in the total assets. The results show that the deepening of the financialization of manufacturing enterprises significantly reduces TFP and the magnitude of the impacts of different types of financial assets variates. In addition, the effects of corporate financialization on TFP are heterogeneous in terms of their significance and degrees in different types of enterprises as well as in different levels of enterprises' TFP. The further analysis of the influencing mechanism shows that corporate financialization has different effects on the TFP of manufacturing enterprises through technological innovation and resource allocation efficiency.

Citation: Siming Liu, Xiaoyan Shen, Tianpei Jiang, Pierre Failler. Impacts of the financialization of manufacturing enterprises on total factor productivity: empirical examination from China's listed companies[J]. Green Finance, 2021, 3(1): 59-89. doi: 10.3934/GF.2021005

This paper examines the effects and mechanism of the financialization of manufacturing enterprises on total factor productivity (TFP). Thus, it provides evidence of the economic consequences of corporate financialization from the perspective of productivity. Using the panel data of China's listed manufacturing companies from 2007 to 2018, the level of corporate financialization is measured using the proportion of financial assets in the total assets. The results show that the deepening of the financialization of manufacturing enterprises significantly reduces TFP and the magnitude of the impacts of different types of financial assets variates. In addition, the effects of corporate financialization on TFP are heterogeneous in terms of their significance and degrees in different types of enterprises as well as in different levels of enterprises' TFP. The further analysis of the influencing mechanism shows that corporate financialization has different effects on the TFP of manufacturing enterprises through technological innovation and resource allocation efficiency.

| [1] |

Ang JB (2010) Does foreign aid promote growth? exploring the role of financial liberalization. Rev Dev Econ 14: 197–212. doi: 10.1111/j.1467-9361.2010.00547.x

|

| [2] |

Ackerberg DA, Caves K, Frazer G (2015) Identification properties of recent production function estimators. Econometrica 83: 2411–2451. doi: 10.3982/ECTA13408

|

| [3] |

Arizala F, Cavallo E, Galindo A (2013) Financial development and TFP growth: cross-country and industry-level evidence. Appl Finan Econ 23: 433–448. doi: 10.1080/09603107.2012.725931

|

| [4] |

Baum CF, Caglayan M, Ozkan N, et al. (2006) The impact of macroeconomic uncertainty on non-financial firms' demand for liquidity. Rev Financ Econ 15: 289–304. doi: 10.1016/j.rfe.2006.01.002

|

| [5] | Beck THL, Levine R (2002) Industry growth and capital allocation: Does having a market- or bank-based system matter? J Financ Econ 64: 147–180. |

| [6] |

Blundell R, Bond S (1998) Initial Conditions and Moment Conditions in Dynamic Panel Data Model. J Econometrics 87: 115–143. doi: 10.1016/S0304-4076(98)00009-8

|

| [7] |

Bonfiglioli A (2008) Financial integration, productivity and capital accumulation. J Int Econ 76: 337–355. doi: 10.1016/j.jinteco.2008.08.001

|

| [8] |

Bonizzi B (2013) Financialization in Developing and Emerging Countries. Int J Polit Economy 42: 83–107. doi: 10.2753/IJP0891-1916420405

|

| [9] |

Borensztein, Eduardo R (1987) Alternative Hypotheses about the Excess Return on Dollar Assets, 1980–84. IMF Econ Rev 34: 29–59. doi: 10.2307/3867023

|

| [10] |

Boumparis P, Milas C, Panagiotidis T (2017) Economic policy uncertainty and sovereign credit rating decisions: Panel quantile evidence for the Eurozone. J Int Money Finance 79: 39–71. doi: 10.1016/j.jimonfin.2017.08.007

|

| [11] |

Broni M, Hosen M, Masih M (2019) Does a country's external debt level affect its Islamic banking sector development? Evidence from Malaysia based on Quantile regression and Markov regime-switching. Quant Financ Econ 3: 366–389. doi: 10.3934/QFE.2019.2.366

|

| [12] | Cetina K, Karin, Preda A (2012) The Oxford Handbook of the Sociology of Finance, Oxford University Press: New York, NY, USA. |

| [13] | Chen DQ, Chen YS, Dong ZY (2017) Policy Uncertainty, Market Competition and Allocation of Capital: Evidence from Turnover of City-level Leaders. J Finan Res 11: 65–80. |

| [14] |

Chen X (2015) The Influence of Financialization on Industrial Development: An Empirical Analysis in China. Arch Bus Res 3: 65–77. doi: 10.14738/abr.31.780

|

| [15] | Cibils A, Allami C (2013) Financialisation vs. Development Finance: the Case of the Post-Crisis Argentine Banking System. Revue de la régulation 13. |

| [16] | Consolandi C, Cupertino S, Vercelli A (2019) Corporate Social Performance, Financialization, and Real Investment in US Manufacturing Firms. Sustainability 11: 1–15. |

| [17] | Cooper R, Kleinschmidt E (1987) New Products: What Separates Winners from Losers? J Prod Innov Manage 4: 169–184. |

| [18] | Dai M, Li X, Lu Y (2017) How Urbanization Economies Impact TFP of R & D Performers: Evidence from China. Sustainability 9: 1766. |

| [19] |

Davis L (2018) Financialization and the non-financial corporation: An investigation of firm-level investment behavior in the United States. Metroeconomica 69: 270–307. doi: 10.1111/meca.12179

|

| [20] |

Demir F (2009a) Financial Liberalization, Private Investment and Portfolio Choice: Financialization of Real Sectors in Emerging Markets. J Dev Econ 88: 314–324. doi: 10.1016/j.jdeveco.2008.04.002

|

| [21] |

Demir F (2009b) Financialization and Manufacturing Firm Profitability under Uncertainty and Macroeconomic Volatility: Evidence from an Emerging Market. Rev Dev Econ 13: 592–609. doi: 10.1111/j.1467-9361.2009.00522.x

|

| [22] |

Dept E, Lamarche C (2009) A quantile regression approach for estimating panel data models using instrumental variables. Econ Lett 104: 133–135. doi: 10.1016/j.econlet.2009.04.025

|

| [23] |

Doepke M, Schneider M (2006) Inflation and the Redistribution of Nominal Wealth. J Polit Economy 114: 1069–1097. doi: 10.1086/508379

|

| [24] | Epstein GA (2005) Financialization and the World Economy, Edward Elgar Publishing: Cheltenham, UK. |

| [25] |

Frésard L (2010) Financial Strength and Product Market Behavior: The Real Effects of Corporate Cash Holdings. J Financ 65: 1097–1122. doi: 10.1111/j.1540-6261.2010.01562.x

|

| [26] |

Gehringer A (2013) Growth, productivity and capital accumulation: The effects of financial liberalization in the case of European integration. Int Rev Econ Financ 25: 291–309. doi: 10.1016/j.iref.2012.07.015

|

| [27] |

Gregorio JD, Guidotti PE (1995) Financial development and economic growth. World Dev 23: 433–448. doi: 10.1016/0305-750X(94)00132-I

|

| [28] | Hall BH (2005) The financing of innovation, The handbook of technology and innovation management. Wiley-Blackwell Publishers, Ltd., Oxford, UK, 409–430. |

| [29] |

Hall BH (2002) The Financing of Research and Development. Oxford Rev Econ Pol 18: 35–51. doi: 10.1093/oxrep/18.1.35

|

| [30] |

Holmström B (1989) Agency Cost and Innovation. J Econ Behav Organ 12: 305–327. doi: 10.1016/0167-2681(89)90025-5

|

| [31] |

Hong M, Drakeford B, Zhang KX (2020) The impact of mandatory CSR disclosure on green innovation: evidence from China. Green Financ 2: 302–322. doi: 10.3934/GF.2020017

|

| [32] | Hou P, Li YL, Tan Y, et al. (2020) Energy Price and Energy Efficiency in China: A Linear and Nonlinear Empirical Investigation. Energies 13. |

| [33] |

Hsieh CT, Klenow P (2009) Misallocation and Manufacturing TFP in China and India. Q J Econ 124: 1403–1448. doi: 10.1162/qjec.2009.124.4.1403

|

| [34] |

Hudson M (2010) From Marx to Goldman Sachs: The Fictions of Fictitious Capital, and the Financialization of Industry. Critique 38: 419–444. doi: 10.1080/03017605.2010.492685

|

| [35] | Islam N, Dai E, Sakamoto H (2006) Role of TFP in China's growth. Asian Econ J 20: 127–159. |

| [36] | Jin L, Mo C, Zhang B, et al. (2018) What Is the Focus of Structural Reform in China?—Comparison of the Factor Misallocation Degree within the Manufacturing Industry with a Unified Model. Sustainability 10: 4051. |

| [37] |

Karacimen E (2014) Financialization in Turkey: The Case of Consumer Debt. J Balkan Near E Stud 16: 161–180. doi: 10.1080/19448953.2014.910393

|

| [38] | Kasahara H, Rodrigue J (2008) Does the use of imported intermediates increase productivity? Plant–level evidence. J Dev Econ: 106–118. |

| [39] |

Kato R, Kiyotaki N, Moore J (1997) Credit Cycle. J Polit Economy 105: 211–248. doi: 10.1086/262072

|

| [40] |

Kliman A, Williams S (2015) Why 'Financialisation' Hasn't Depressed US Productive Investment. Cambridge J Econ 39: 67–92. doi: 10.1093/cje/beu033

|

| [41] | Kneer C (2013) Finance as a Magnet for the Best and Brightest: Implications for the Real Economy, DNB Working Paper No.392. |

| [42] | Koenker R (2004) Quantile regression for longitudinal data. JMA 91: 74–89. |

| [43] |

Kotz DM (2009) The Financial and Economic Crisis of 2008: A Systemic Crisis of Neoliberal Capitalism. Rev Radical Polit Econ 41: 305–317. doi: 10.1177/0486613409335093

|

| [44] |

Krippner GR (2005) The financialization of the American economy. Socioecon Rev 3:173–208. doi: 10.1093/SER/mwi008

|

| [45] | Krugman PR (1995) The age of diminished expectations, MIT Press: Cambridge, MA, USA. |

| [46] |

Lapavitsas C (2013) The financialization of capitalism: 'Profiting without producing'. City 17: 792–805. doi: 10.1080/13604813.2013.853865

|

| [47] | Levine R (2004) Finance and Growth: Theory and Evidence. National Bureau of Economic Research, Inc, NBER Working Papers 10766. |

| [48] |

Levinsohn J, Petrin A (2003) Estimating Production Function Using Inputs to Control for Observables. Rev Econ Stud 70: 317–341. doi: 10.1111/1467-937X.00246

|

| [49] |

Li ZH, Liao GK, Albitar K (2020) Does corporate environmental responsibility engagement affect firm value? The mediating role of corporate innovation. Bus Strategy Environ 29: 1045–1055. doi: 10.1002/bse.2416

|

| [50] | Li ZH, Chen LM, Dong H (2021) What are bitcoin market reactions to its-related events? Int Rev Econ Financ 73: 1–10. |

| [51] |

Liu Y, Li ZH, Xu MR (2020) The influential factors of financial cycle spillover: evidence from China. Emerg Mark Financ Tr 56: 1336–1350. doi: 10.1080/1540496X.2019.1658076

|

| [52] |

Love J, Roper S (1999) The Determinants of Innovation: R & D, Technology Transfer and Networking Effects. Rev Ind Organ 15: 43–64. doi: 10.1023/A:1007757110963

|

| [53] | Lu L, Min N (2019) The Inverted U-Shaped Relationship between Commodity Financialization and Portfolio Performance. Stud Int Financ, 67–76. |

| [54] |

Lu X, Guo K, Dong Z, et al. (2017) Financial development and relationship evolvement among money supply, economic growth and inflation: a comparative study from the US and China. Appl Econ 49: 1032–1045. doi: 10.1080/00036846.2016.1210776

|

| [55] |

McLean R, Zhang T, Zhao M (2012) Why Does the Law Matter? Investor Protection and Its Effects on Investment, Finance, and Growth. J Fin 67: 313–350. doi: 10.1111/j.1540-6261.2011.01713.x

|

| [56] |

Milberg W (2008) Shifting sources and uses of profits: sustaining US financialization with global value chains. Economy Society 37: 420–451. doi: 10.1080/03085140802172706

|

| [57] | Mohamed S (2016) Financialization of the South African Economy. Development, 137–142. |

| [58] |

Mollisi V, Rovigatti G (2018) Theory and Practice of TFP Estimation: The Control Function Approach Using Stata. Stata J 18: 618–662. doi: 10.1177/1536867X1801800307

|

| [59] | Monaghan L, O'Flynn M (2012) More Than Anarchy in the UK: 'Social Unrest' and its Resurgence in the Madoffized Society. Soc Res Online 17. |

| [60] | Montgomerie J (2008) Bridging the critical divide: Global finance, financialization and contemporary capitalism. Contemp. Politics 14: 233–252. |

| [61] | Moreira C, Almeida A (2010) "Financialization" of capitalism and its recent effects on Latin American emergent economies. World Rev Polit Economy 1: 500–516. |

| [62] |

Morris D (2018) Innovation and productivity among heterogeneous firms. Res Pol 47: 1918–1932. doi: 10.1016/j.respol.2018.07.003

|

| [63] |

Okada K, Samreth S (2012) The effect of foreign aid on corruption: A quantile regression approach. Econ Lett 115: 240–243. doi: 10.1016/j.econlet.2011.12.051

|

| [64] | Olley G, Pakes A (1992) The Dynamics of Productivity in The Telecommunications Equipment Industry. Econometrica 64. |

| [65] |

Orhangazi O (2008) Financialisation and Capital Accumulation in the Non-Financial Corporate Sector. Cambridge J Econ 32: 863–886. doi: 10.1093/cje/ben009

|

| [66] |

Palia D, Lichtenberg F (1999) Managerial Ownership and Firm Performance: A Re-Examination Using Productivity Measurement. J Corp Financ 5: 323–339. doi: 10.1016/S0929-1199(99)00009-7

|

| [67] | Pavitt K (1982) R & D, patenting and innovative activities: A statistical exploration. Res Pol 11: 33–51. |

| [68] | Pozzolo AF, Schivardi F, Nucci F (2005) Is Firm's Productivity Related to its Financial Structure? Evidence from Microeconomic Data. Rivista Politica Econ 95: 269–290. |

| [69] |

Pushner G (1995) Equity ownership structure, leverage, and productivity: Empirical evidence from Japan. Pacific Basin Financ J 3: 241–255. doi: 10.1016/0927-538X(95)00003-4

|

| [70] |

Qamruzzaman M, Wei J (2018) Investigation of the asymmetric relationship between financial innovation, banking sector development, and economic growth. Quant Financ Econ 2: 952–980. doi: 10.3934/QFE.2018.4.952

|

| [71] |

Qamruzzaman M, Wei J (2019) Do financial inclusion, stock market development attract foreign capital flows in developing economy: a panel data investigation. Quant Financ Econ 3: 88–108. doi: 10.3934/QFE.2019.1.88

|

| [72] | Radzievska S (2016) Global Crisis, financialization and technological development. Int Econ Pol 1: 124–154. |

| [73] |

Reed W (2015) On the Practice of Lagging Variables to Avoid Simultaneity. Oxford Bull Econ Statist 77: 897–905. doi: 10.1111/obes.12088

|

| [74] | Ren SG, Zheng JJ, Liu DH, et al. (2019) Does Emissions Trading System Improve Firm' s Total Factor Productivity-Evidence from Chinese Listed Companies. China Ind Econ, 5–23. |

| [75] | Rossman P, Greenfield G (2006) Financialization: New Routes to Profit, New Challenges for Trade Unions. Labour Education, The Quarterly Review of the ILO Bureau for Workers' Activities 1: 55–62. |

| [76] | Sawyer M (2013) What Is Financialization? Int J Polit Economy 42: 5–18. |

| [77] | Seo HJ, Kim H, Kim Y (2012) Financialization and the Slowdown in Korean Firms' R & D Investment. Asian Econ Pap 11: 35–49. |

| [78] | Seo HJ, Kim H, Kim J (2016) Does Shareholder Value Orientation or Financial Market Liberalization Slow Down Korean Real Investment? Rev Radical Polit Econ 48: 633–660. |

| [79] |

Sheu HJ, Yang CY (2005) Insider Ownership Structure and Firm Performance: A Productivity Perspective Study in Taiwan's Electronics Industry. Corp Gov 13: 326–337. doi: 10.1111/j.1467-8683.2005.00426.x

|

| [80] | Shibai L (2010) On over-financialization and the US financial crisis. Economist 6. |

| [81] |

Sleuwaegen L, Goedhuys M (2002) Growth of firms in developing countries, evidence from Cote d'Ivoire. J Dev Econ 68: 117–135. doi: 10.1016/S0304-3878(02)00008-1

|

| [82] | Song J, Lu Y (2015) U-shape relationship between non-currency financial assets and operating profit: Evidence from financialization of Chinese listed non-financial corporates. J Finan Res 6: 111–127. |

| [83] | Sterlacchini A (1989) R & D, Innovations, and Total Factor Productivity Growth in British Manufacturing. Appl Econ 21: 1549–1562. |

| [84] | Stockhammer E (2010) Financialization and the global economy. PERI Working Paper No. 240. |

| [85] |

Stucki T, Woerter M (2019) Competitive Pressure and Diversification into Green R & D. Rev Ind Organ 55: 301–325. doi: 10.1007/s11151-018-9656-6

|

| [86] | Sulaiman N (2012) An Input-Output Analysis of the Total Factor Productivity Growth of the Malaysian Manufacturing Sector, 1983–2005. J Ekonomi Malaysia 46: 147–155. |

| [87] | Sun L (2018) Quantifying the Effects of Financialization and Leverage in China. Chinese Economy 51: 1–18. |

| [88] | Tabb WK (2013) The international spread of financialization, In: The Handbook of the Political Economy of Financial Crises; Wolfson, M., Epstein, G., Eds.; Oxford University Press: New York, NY, USA, 526–539. |

| [89] |

Tori D, Onaran O (2018) The effects of financialization on investment: Evidence from firm-level data for the UK. Cambridge J Econ 42: 1393–1416. doi: 10.1093/cje/bex085

|

| [90] | Tripathy N (2019) Does measure of financial development matter for economic growth in India? Quant Financ Econ 3: 508–525. |

| [91] | Tsionas M, Mallick S (2019) A Bayesian Semiparametric Approach to Stochastic Frontiers and Productivity. Eur J Oper Res 274. |

| [92] |

Wang YY (2015) The rise of the "shareholding state": financialization of economic management in China. Socioecon Rev 13: 603–625. doi: 10.1093/ser/mwv016

|

| [93] |

Wooldridge J (2009) On Estimating Firm-Level Production Functions Using Proxy Variables to Control for Unobservable. Econ Lett 104: 112–114. doi: 10.1016/j.econlet.2009.04.026

|

| [94] |

Wurgler J (2000) Financial Markets and The Allocation of Capital. J Finan Econ 58: 187–214. doi: 10.1016/S0304-405X(00)00070-2

|

| [95] | Xi X, Zhou J, Gao X, et al. (2020) Impact of the global mineral trade structure on national economies based on complex network and panel quantile regression analyses. Resour Conserv Recycl 154. |

| [96] |

Xu MR, Albitar K, Li ZH (2020) Does corporate financialization affect EVA? Early evidence from China. Green Financ 2: 392–408. doi: 10.3934/GF.2020021

|

| [97] |

Yan D, Kong Y, Ren X, et al. (2019) The determinants of urban sustainability in Chinese resource-based cities: A panel quantile regression approach. Sci Total Environ 686: 1210–1219. doi: 10.1016/j.scitotenv.2019.05.386

|

| [98] | Zhang D, Liu D (2017) Determinants of the capital structure of Chinese non-listed enterprises: Is TFP efficient? Econ Systems 41: 179–202. |

| [99] | Zheng ZL, Gao X, Ruan XL (2019) Does economic financialization lead to the alienation of enterprise investment behavior? Evidence from China. Phys A 536. |

| [100] |

Zhu J, Ye K, Tucker J, et al. (2016) Board hierarchy, independent directors, and firm value: Evidence from China. J Corp Financ 41: 262–279. doi: 10.1016/j.jcorpfin.2016.09.009

|

| [101] |

Zhu ZH, Huang F (2012) The effect of R & D investment on firms financial performance: Evidence from Chinese listed IT firms. Modern Economy 3: 915–919. doi: 10.4236/me.2012.38114

|

Figures(3) / Tables(9)

Siming Liu, Xiaoyan Shen, Tianpei Jiang, Pierre Failler. Impacts of the financialization of manufacturing enterprises on total factor productivity: empirical examination from China's listed companies[J]. Green Finance, 2021, 3(1): 59-89. doi: 10.3934/GF.2021005

DownLoad:

DownLoad: