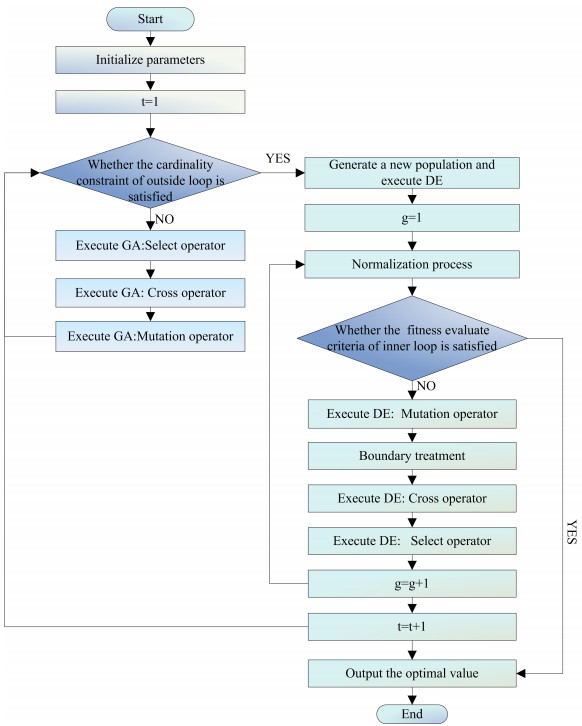

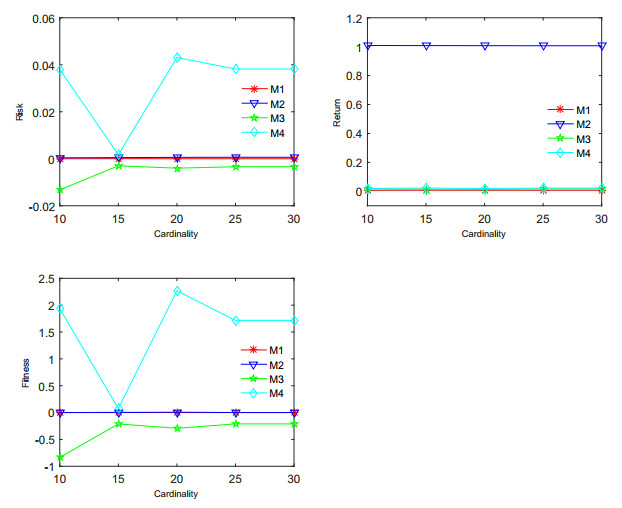

This paper introduces the idea of fractional programming in a portfolio model and builds four fractional programming portfolio optimization models based on various risk measures in a fuzzy environment, with the aim of addressing the complexity of historical data of real securities markets and the fundamental form of existing portfolio models. The four models build on the mean–variance(MV) model by adding a number of useful limitations, such as restrictions on short selling, proportionate investment boundary restrictions, and portfolio cardinality constraints, to better suit the requirements of genuine currency-related stock markets. For the portfolio optimization problem, which is a 0-1 mixed-integer fractional programming problem, a dual-loop hybrid heuristic algorithm is proposed. This algorithm incorporates the constraints of the model into the algorithm, thereby avoiding the drawbacks of the penalty function method. The empirical analysis part uses historical data to simulate investments and compare portfolio strategies under various risk metrics in order to show how well the models perform. The numerical results of the four models are also compared, showing that the models are suitable for different investors and that they are consistent with actual stock market conditions.

Citation: Chenyang Hu, Yuelin Gao, Eryang Guo. Fractional portfolio optimization based on different risk measures in fuzzy environment[J]. AIMS Mathematics, 2025, 10(4): 8331-8363. doi: 10.3934/math.2025384

This paper introduces the idea of fractional programming in a portfolio model and builds four fractional programming portfolio optimization models based on various risk measures in a fuzzy environment, with the aim of addressing the complexity of historical data of real securities markets and the fundamental form of existing portfolio models. The four models build on the mean–variance(MV) model by adding a number of useful limitations, such as restrictions on short selling, proportionate investment boundary restrictions, and portfolio cardinality constraints, to better suit the requirements of genuine currency-related stock markets. For the portfolio optimization problem, which is a 0-1 mixed-integer fractional programming problem, a dual-loop hybrid heuristic algorithm is proposed. This algorithm incorporates the constraints of the model into the algorithm, thereby avoiding the drawbacks of the penalty function method. The empirical analysis part uses historical data to simulate investments and compare portfolio strategies under various risk metrics in order to show how well the models perform. The numerical results of the four models are also compared, showing that the models are suitable for different investors and that they are consistent with actual stock market conditions.

| [1] | H. Markowitz, Portfolio selection, J. Financ., 7 (1952), 77–91. https://doi.org/10.1111/j.1540-6261.1952.tb01525.x |

| [2] |

L. Plachel, A unified model for regularized and robust portfolio optimization, J. Econ. Dyn. Control, 109 (2019), 103779. https://doi.org/10.1016/j.jedc.2019.103779 doi: 10.1016/j.jedc.2019.103779

|

| [3] |

W. Wang, W. Li, N. Zhang, K. Liu, Portfolio formation with preselection using deep learning from long-term financial data, Expert Syst. Appl., 143 (2020), 113042. https://doi.org/10.1016/j.eswa.2019.113042 doi: 10.1016/j.eswa.2019.113042

|

| [4] |

W. Chen, H. Zhang, M. K. Mehlawat, L. Jia, Mean–Cvariance portfolio optimization using machine learning-based stock price prediction, Appl. Soft Comput., 100 (2021), 106943. https://doi.org/10.1016/j.asoc.2020.106943 doi: 10.1016/j.asoc.2020.106943

|

| [5] |

Y. Ma, R. Han, W. Wang, Portfolio optimization with return prediction using deep learning and machine learning, Expert Syst. Appl., 165 (2021), 113973. https://doi.org/10.1016/j.eswa.2020.113973 doi: 10.1016/j.eswa.2020.113973

|

| [6] | L. A. Zadel, Fuzzy sets, Information and Control, 8 (1965), 338–353. https://doi.org/10.1016/S0019-9958(65)90241-X |

| [7] |

B. Wang, Y. Li, S. Wang, J. Watada, A multi-objective portfolio selection model with fuzzy value-at-risk ratio, IEEE Trans. Fuzzy Syst., 26 (2018), 3673–3687. https://doi.org/10.1109/TFUZZ.2018.2842752 doi: 10.1109/TFUZZ.2018.2842752

|

| [8] |

E. Vercher, J. D. Bermdez, Portfolio optimization using a credibility mean-absolute semi-deviation model, Expert Syst. Appl., 42 (2015), 7121–7131. https://doi.org/10.1016/j.eswa.2015.05.020 doi: 10.1016/j.eswa.2015.05.020

|

| [9] |

H.-Q. Li, Z.-H. Yi, Portfolio selection with coherent Investor's expectations under uncertainty, Expert Syst. Appl., 133 (2019), 49–58. https://doi.org/10.1016/j.eswa.2019.05.008 doi: 10.1016/j.eswa.2019.05.008

|

| [10] |

W. Guo, W.-G. Zhang, X. Chen, Portfolio selection models considering fuzzy preference relations of decision makers, IEEE Trans. Syst. Man Cyber.: Syst., 54 (2024), 2254–2265. https://doi.org/10.1109/TSMC.2023.3342038 doi: 10.1109/TSMC.2023.3342038

|

| [11] |

P. K. Mandal, M. Thakur, G. Mittal, Credibilistic portfolio optimization with higher-order moments using coherent triangular fuzzy numbers, Appl. Soft Comput., 151 (2024), 111155. https://doi.org/10.1016/j.asoc.2023.111155 doi: 10.1016/j.asoc.2023.111155

|

| [12] | Y. Zaychenko, H. Zaychenko, Fuzzy portfolio optimization problem under uncertainty and its solution, In: 2020 IEEE 15th international conference on computer sciences and information technologies (CSIT), IEEE, Zbarazh, Ukraine, 23–26 September 2020, 1–6. https://doi.org/10.1109/CSIT49958.2020.9322025 |

| [13] |

J. K. Pahade, M. Jha, Credibilistic variance and skewness of trapezoidal fuzzy variable and mean-Cvarianc-Cskewness model for portfolio selection, Results Appl. Math., 11 (2021), 100159. https://doi.org/10.1016/j.rinam.2021.100159 doi: 10.1016/j.rinam.2021.100159

|

| [14] |

S. Kaur, A. Singh, A. Aggarwal, Mean–Variance optimal portfolio selection integrated with support vector and fuzzy support vector machines, Journal of Fuzzy Extension and Applications, 5 (2024), 434–468. https://doi.org/10.22105/jfea.2024.453926.1453 doi: 10.22105/jfea.2024.453926.1453

|

| [15] |

M. A. Moghadam, S. B. Ebrahimi, D. Rahmani, A constrained multi-period robust portfolio model with behavioral factors and an interval semi-absolute deviation, J. Comput. Appl. Math., 374 (2020), 112742. https://doi.org/10.1016/j.cam.2020.112742 doi: 10.1016/j.cam.2020.112742

|

| [16] |

W. Yue, Y. Wang, H. Xuan, Fuzzy multi-objective portfolio model based on semi-variance–semi-absolute deviation risk measures, Soft Comput., 23 (2019), 8159–8179. https://doi.org/10.1007/s00500-018-3452-y doi: 10.1007/s00500-018-3452-y

|

| [17] |

J. K. Pahade, M. Jha, A hybrid fuzzy-SCOOT algorithm to optimize possibilistic mean semi-absolute deviation model for optimal portfolio selection, Int. J. Fuzzy Syst., 24 (2022), 1958–1973. https://doi.org/10.1007/s40815-022-01251-w doi: 10.1007/s40815-022-01251-w

|

| [18] |

S. Banihashemi, S. Navidi, Portfolio performance evaluation in Mean-CVaR framework: a comparison with non-parametric methods value at risk in Mean-VaR analysis, Operations Research Perspectives, 4 (2017), 21–28. https://doi.org/10.1016/j.orp.2017.02.001 doi: 10.1016/j.orp.2017.02.001

|

| [19] |

H. Babazadeh, A. Esfahanipour, A novel multi period mean-VaR portfolio optimization model considering practical constraints and transaction cost, J. Comput. Appl. Math., 361 (2019), 313–342. https://doi.org/10.1016/j.cam.2018.10.039 doi: 10.1016/j.cam.2018.10.039

|

| [20] |

C. Jiang, X. Ding, Q. Xu, Y. Tong, A TVM-Copula-MIDAS-GARCH model with applications to VaR-based portfolio selection, North Amer. J. Econ. Financ., 51 (2020), 101074. https://doi.org/10.1016/j.najef.2019.101074 doi: 10.1016/j.najef.2019.101074

|

| [21] |

Z. Kang, L. Zhao, J. Sun, The optimal portfolio of a-maxmin mean-VaR problem for investors, Physica A, 526 (2019), 120778. https://doi.org/10.1016/j.physa.2019.04.014 doi: 10.1016/j.physa.2019.04.014

|

| [22] |

R. Sehgal, A. Sharma, R. Mansini, Worst-case analysis of Omega-VaR ratio optimization model, Omega, 114 (2023), 102730. https://doi.org/10.1016/j.omega.2022.102730 doi: 10.1016/j.omega.2022.102730

|

| [23] |

A. Peña, L. M. Sepúlveda-Cano, J. D. Gonzalez-Ruiz, N. J. Marín-Rodríguez, S. Botero-Botero, Deep fuzzy credibility surfaces for integrating external databases in the estimation of operational value at risk, Sci, 6 (2024), 74. https://doi.org/10.3390/sci6040074 doi: 10.3390/sci6040074

|

| [24] |

M. S. Strub, D. Li, X. Cui, J. Gao, Discrete-time mean-CVaR portfolio selection and time-consistency induced term structure of the CVaR, J. Econ. Dyn. Control, 108 (2019), 103751. https://doi.org/10.1016/j.jedc.2019.103751 doi: 10.1016/j.jedc.2019.103751

|

| [25] |

T. Bodnar, M. Lindholm, V. Niklasson, E. Thorsén, Bayesian portfolio selection using VaR and CVaR, Appl. Math. Comput., 427 (2022), 127120. https://doi.org/10.1016/j.amc.2022.127120 doi: 10.1016/j.amc.2022.127120

|

| [26] |

S. Benati, E. Conde, A relative robust approach on expected returns with bounded CVaR for portfolio selection, Eur. J. Oper. Res., 296 (2022), 332–352. https://doi.org/10.1016/j.ejor.2021.04.038 doi: 10.1016/j.ejor.2021.04.038

|

| [27] |

K. Su, Y. Yao, C. Zheng, W. Xie, A novel hybrid strategy for crude oil future hedging based on the combination of three minimum-CVaR models, Int. Rev. Econ. Financ., 83 (2023), 35–50. https://doi.org/10.1016/j.iref.2022.08.019 doi: 10.1016/j.iref.2022.08.019

|

| [28] |

M.-F. Leung, J. Wang, H. Che, Cardinality-constrained portfolio selection via two-timescale duplex neurodynamic optimization, Neural Networks, 153 (2022), 399–410. https://doi.org/10.1016/j.neunet.2022.06.023 doi: 10.1016/j.neunet.2022.06.023

|

| [29] |

M.-F. Leung, J. Wang, Cardinality-constrained portfolio selection based on collaborative neurodynamic optimization, Neural Networks, 145 (2022), 68–79. https://doi.org/10.1016/j.neunet.2021.10.007 doi: 10.1016/j.neunet.2021.10.007

|

| [30] |

J. He, A fuzzy portfolio model with cardinality constraints based on differential evolution algorithms, Int. J. Data Warehous. Min., 20 (2024), 1–14. https://doi.org/10.4018/IJDWM.341268 doi: 10.4018/IJDWM.341268

|

| [31] | Z. X. Loke, S. L. Goh, J. Likoh, A self-adaptive step-size search algorithm for the cardinality constrained portfolio optimisation problem, In: 2024 20th IEEE international colloquium on signal processing & its applications (CSPA), IEEE, Langkawi, Malaysia, 01–02 March 2024,292–297. https://doi.org/10.1109/CSPA60979.2024.10525478 |

| [32] |

D. Deliktas, O. Ustun, Multi-objective genetic algorithm based on the fuzzy MULTIMOORA method for solving the cardinality constrained portfolio optimization, Appl. Intell., 53 (2023), 14717–14743. https://doi.org/10.1007/s10489-022-04240-6 doi: 10.1007/s10489-022-04240-6

|

| [33] |

H. Zhao, Z.-G. Chen, Z.-H. Zhan, S. Kwong, J. Zhang, Multiple populations co-evolutionary particle swarm optimization for multi-objective cardinality constrained portfolio optimization problem, Neurocomputing, 430 (2021), 58–70. https://doi.org/10.1016/j.neucom.2020.12.022 doi: 10.1016/j.neucom.2020.12.022

|

| [34] |

W. Chen, Y. Wang, P. Gupta, M. K. Mehlawat, A novel hybrid heuristic algorithm for a new uncertain mean-variance-skewness portfolio selection model with real constraints, Appl. Intell., 48 (2018), 2996–3018. https://doi.org/10.1007/s10489-017-1124-8 doi: 10.1007/s10489-017-1124-8

|

| [35] |

C. B. Kalayci, O. Polat, M. A. Akbay, An efficient hybrid metaheuristic algorithm for cardinality constrained portfolio optimization, Swarm Evol. Comput., 54 (2020), 100662. https://doi.org/10.1016/j.swevo.2020.100662 doi: 10.1016/j.swevo.2020.100662

|

| [36] |

W. Yue, Y. Wang, C. Dai, An evolutionary algorithm for multiobjective fuzzy portfolio selection models with transaction cost and liquidity, Math. Probl. Eng., 2015 (2015), 569415. https://doi.org/10.1155/2015/569415 doi: 10.1155/2015/569415

|

| [37] | X. Meng, X. Zhou, Multi-period fuzzy portfolio selection model with cardinality constraints, In: 2019 16th international conference on service systems and service management (ICSSSM), IEEE, 13–15 July 2019, Shenzhen, China, 1–6. https://doi.org/10.1109/ICSSSM.2019.8887735 |

| [38] |

C. Carlsson, R. Fullér, On possibilistic mean value and variance of fuzzy numbers, Fuzzy Set. Syst., 122 (2001), 315–326. https://doi.org/10.1016/S0165-0114(00)00043-9 doi: 10.1016/S0165-0114(00)00043-9

|

| [39] |

R. Fisher, The analysis of variance with various binomial transformations, Biometrics, 10 (1954), 130–139. https://doi.org/10.2307/3001667 doi: 10.2307/3001667

|

| [40] | D. Dubois, H. Prade, Possibility theory, In: Granular, fuzzy, and soft computing, New York, NY: Springer, 2023. 859–876. https://doi.org/10.1007/978-1-0716-2628-3_413 |

| [41] |

B. Wang, S. Wang, J. Watada, Fuzzy-portfolio-selection models with value-at-risk, IEEE Trans. Fuzzy Syst., 19 (2011), 758–769. https://doi.org/10.1109/TFUZZ.2011.2144599 doi: 10.1109/TFUZZ.2011.2144599

|

| [42] | J. Peng, Value at risk and tail value at risk in uncertain environment, In: Proceedings of the 8th international conference on information and management sciences, Kunming, China, July 20–28, 2009,787–793. |

| [43] |

A. G. Quaranta, A. Zaffaroni, Robust optimization of conditional value at risk and portfolio selection, J. Bank Financ., 32 (2008), 2046–2056. https://doi.org/10.1016/j.jbankfin.2007.12.025 doi: 10.1016/j.jbankfin.2007.12.025

|

| [44] |

J. Xue, B. Shen, A novel swarm intelligence optimization approach: sparrow search algorithm, Syst. Sci. Control Eng., 8 (2020), 22–34. https://doi.org/10.1080/21642583.2019.1708830 doi: 10.1080/21642583.2019.1708830

|

| [45] | R. Eberhart, J. Kennedy, A new optimizer using particle swarm theory, In: MHS'95. Proceedings of the sixth international symposium on micro machine and human science, IEEE, Nagoya, Japan, 04–06 October 1995, 39–43. https://doi.org/10.1109/MHS.1995.494215 |

| [46] | J. H. Holland, Genetic algorithms, Sci. Amer., 267 (1992), 66–73. |

| [47] | K. V. Price, R. M. Storn, J. A. Lampinen, The differential evolution algorithm, In: Differential evolution: a practical approach to global optimization, Berlin, Heidelberg: Springer, 2005, 37–134. https://doi.org/10.1007/3-540-31306-0_2 |

Figures(3) / Tables(12)

Chenyang Hu, Yuelin Gao, Eryang Guo. Fractional portfolio optimization based on different risk measures in fuzzy environment[J]. AIMS Mathematics, 2025, 10(4): 8331-8363. doi: 10.3934/math.2025384

DownLoad:

DownLoad: