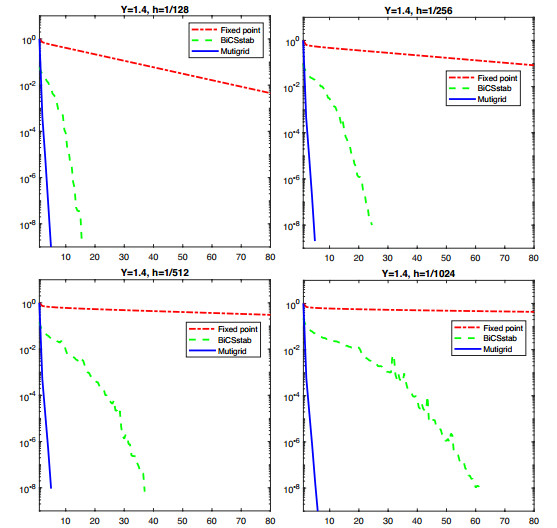

We propose a fast multigrid method for solving the discrete partial integro-differential equations (PIDEs) arising from pricing European options when the underlying asset is driven by an infinite activity Lévy process. We consider the CGMY model whose kernel singularity gets worse when the parameter Y approaches two. Due to the integral term, the discretization matrix is dense. In order to obtain an efficient multigrid method, we apply a fixed point iteration as a smoother for multigrid. In each smoothing step, we only need to solve a sparse matrix corresponding to the differential operator and compute a matrix-vector product involving the integral operator by a fast Fourier transform (FFT). We prove that the fixed point iteration smoother is effective reducing the high frequency components. Moreover, we also prove a two-grid convergence of the multigrid method by a local mode analysis. We demonstrate the effectiveness of the multigrid method by solving the option pricing equation under the CGMY model with finite and infinite variation processes.

Citation: Justin W. L. Wan. Multigrid method for pricing European options under the CGMY process[J]. AIMS Mathematics, 2019, 4(6): 1745-1767. doi: 10.3934/math.2019.6.1745

We propose a fast multigrid method for solving the discrete partial integro-differential equations (PIDEs) arising from pricing European options when the underlying asset is driven by an infinite activity Lévy process. We consider the CGMY model whose kernel singularity gets worse when the parameter Y approaches two. Due to the integral term, the discretization matrix is dense. In order to obtain an efficient multigrid method, we apply a fixed point iteration as a smoother for multigrid. In each smoothing step, we only need to solve a sparse matrix corresponding to the differential operator and compute a matrix-vector product involving the integral operator by a fast Fourier transform (FFT). We prove that the fixed point iteration smoother is effective reducing the high frequency components. Moreover, we also prove a two-grid convergence of the multigrid method by a local mode analysis. We demonstrate the effectiveness of the multigrid method by solving the option pricing equation under the CGMY model with finite and infinite variation processes.

| [1] | R. Cont, P. Tankov, Financial Modelling With Jump Processes, Chapman & Hall/CRC Press, 2003. |

| [2] |

P. Carr, H. Geman, D. B. Madan, et al. The fine structure of asset returns: An empirical investigation, J. Bus., 75 (2002), 305-332. doi: 10.1086/338705

|

| [3] |

P. Carr, H. Geman, D. B. Madan, et al. Stochastic volatility for Lévy processes, Math. Financ., 13 (2003), 345-382. doi: 10.1111/1467-9965.00020

|

| [4] | E. Eberlein, Application of generalized hyperbolic Lévy motion to finance, In: O. BarndorffNielsen, S. Resnick, T. Mikosch, editors, Lévy Processes - Theory and Application, Birkhäuser, Boston, 2001, 319-337. |

| [5] |

D. B. Madan, P. Carr, E. Change, The Variance Gamma process and option pricing, Rev. Financ., 2 (1998), 79-105. doi: 10.1023/A:1009703431535

|

| [6] | D. Madan, Financial modeling with discontinuous price processes, In: O. Barndorff-Nielsen, S. Resnick, T. Mikosch, editors, Lévy Processes - Theory and Application, Birkhäuser, Boston, 2001. |

| [7] | W. Schoutens, Lévy Processes in Finance: Pricing Financial Derivatives, Wiley, New York, 2003. |

| [8] |

D. B. Madan, E. Seneta, The Variance Gamma (VG) model for share market returns, J. Bus., 63 (1990), 511-524. doi: 10.1086/296519

|

| [9] |

A. Almendral, C. W. Oosterlee, On American options under the Variance Gamma process, Appl. Math. Financ., 14 (2007), 131-152. doi: 10.1080/13504860600724885

|

| [10] |

Y. D'Halluin, P. Forsyth, G. Labahn, A penalty method for American options with jump-diffusion processes, Numer. Math., 97 (2004), 321-352. doi: 10.1007/s00211-003-0511-8

|

| [11] | A. Hirsa, D. B. Madan, Pricing American options under Variance Gamma, J. Comput. Financ., 7 (2004), 63-80. |

| [12] |

Y. d'Halluin, P. A. Forsyth, K. Vetzal, Robust numerical methods for contingent claims under jump diffusion processes, IMA J. Numer. Anal., 25 (2005), 87-112. doi: 10.1093/imanum/drh011

|

| [13] | A. Almendral, Numerical valuation of American options under the CGMY process, In: A. Kyprianou, W. Schoutens, P. Wilmott, editors, Exotic Option Pricing and Advanced Lévy Models, Wiley, UK, 2005. |

| [14] |

R. Cont, E. Voltchkova, A finite difference scheme for option pricing in jump diffusion and exponential Lévy models, SIAM J. Numer. Anal., 43 (2005), 1596-1626. doi: 10.1137/S0036142903436186

|

| [15] |

H. Geman, Pure jump Lévy processes for asset price modeling, J. Bank. Financ., 26 (2002), 1297-1316. doi: 10.1016/S0378-4266(02)00264-9

|

| [16] |

A. M. Matache, P. A. Nitsche, C. Schwab, Wavelet Galerkin pricing of American options on Lévy driven assets, Quant. Financ., 5 (2005), 403-424. doi: 10.1080/14697680500244478

|

| [17] |

S. Levendorskiĭ, O. Kudryavtsev, V. Zherder, The relative efficiency of numerical methods for pricing American options under Lévy processes, J. Comput. Financ., 9 (2005), 69-97. doi: 10.21314/JCF.2005.157

|

| [18] |

A. Almendral, C. W. Oosterlee, Numerical valuation of options with jumps in the underlying, Appl. Numer. Math., 53 (2005), 1-18. doi: 10.1016/j.apnum.2004.08.037

|

| [19] |

I. R. Wang, J. W. L. Wan, P. A. Forsyth, Robust numerical valuation of European and American options under the CGMY process, J. Comput. Financ., 10 (2007), 31-69. doi: 10.21314/JCF.2007.169

|

| [20] |

A. Brandt, Multi-level adaptive solutions to boundary-value problems, Math. Comput., 31 (1977), 333-390. doi: 10.1090/S0025-5718-1977-0431719-X

|

| [21] | W. Hackbusch, Multi-Grid Methods and Applications, Springer-Verlag, Berlin, 1985. |

| [22] |

T. F. Chan, W. L. Wan, Robust multigrid methods for elliptic linear systems, J. Comput. Appl. Math., 123 (2000), 323-352. doi: 10.1016/S0377-0427(00)00411-8

|

| [23] |

W. P. Tang, W. L. Wan, Sparse approximate inverse smoother for multi-grid, SIAM J. Matrix Anal. Appl., 21 (2000), 1236-1252. doi: 10.1137/S0895479899339342

|

| [24] |

G. Wittum, On the robustness of ilu smoothing, SIAM J. Sci. Stat. Comput., 10 (1989), 699-717. doi: 10.1137/0910043

|

| [25] |

R. E. Alcouffe, A. Brandt, Jr. J. E. Dendy, et al. The multi-grid method for the diffusion equation with strongly discontinuous coefficients, SIAM J. Sci. Stat. Comput., 2 (1981), 430-454. doi: 10.1137/0902035

|

| [26] |

Jr. J. E. Dendy, Black box multigrid, J. Comput. Phys., 48 (1982), 366-386. doi: 10.1016/0021-9991(82)90057-2

|

| [27] |

A. Reusken, Multigrid with matrix-dependent transfer operators for a singular perturbation problem, Computing, 50 (1993), 199-211. doi: 10.1007/BF02243811

|

| [28] | W. L. Wan, T. F. Chan, B. Smith, An energy-minimizing interpolation for robust multigrid, SIAM J. Sci. Comput., 21 (2000), 1632-1649. |

| [29] |

R. E. Bank, J. Wan, Z. Qu, Kernel preserving multigrid methods for convection-diffusion equations, SIAM J. Matrix Anal. Appl., 27 (2006), 1150-1171. doi: 10.1137/040619533

|

| [30] |

J. Bey, G. Wittum, Downwind numbering: Robust multigrid for convection-diffusion problems, Appl. Numer. Math., 23 (1997), 177-192. doi: 10.1016/S0168-9274(96)00067-0

|

| [31] |

C. W. Oosterlee, F. J. Gaspar, T. Washio, et al. Multigrid line smoothers for high order upwind discretization of convection-dominated problems, J. Comput. Phys., 139 (1998), 274-307. doi: 10.1006/jcph.1997.5854

|

| [32] |

I. Yavneh, Coarse-grid correction for nonelliptic and singular perturbation problems, SIAM J. Sci. Comput., 19 (1998), 1682-1699. doi: 10.1137/S1064827596310998

|

| [33] | A. Jameson, Solution of the Euler equations for two dimensional transonic flow by a multigrid method, Appl. Math. Comput., 13 (1983), 327-355. |

| [34] | P. W. Hemker, G. M. Johnson, Multigrid approaches to the Euler equations, In: S. McCormick, editor, Multigrid Methods, SIAM, 1987, 57-72. |

| [35] | J. W. L. Wan, A. Jameson, Monotonicity preserving multigrid time stepping schemes for conservation laws, Comput. Visual. Sci., 11 (2007), 41-58. |

| [36] | C. W. Oosterlee, On multigrid for linear complementarity problems with application to Americanstyle options, ETNA, 15 (2003), 165-185. |

| [37] |

N. Clarke, K. Parrott, Multigrid for American option pricing with stochastic volatility, Appl. Math. Financ., 6 (1999), 177-195. doi: 10.1080/135048699334528

|

| [38] |

C. Reisinger, G. Wittum, On multigrid for anisotropic equations and variational inequalities "pricing multi-dimensional European and American options", Comput. Visual. Sci., 7 (2004), 189-197. doi: 10.1007/s00791-004-0149-9

|

| [39] |

H. B. Zubair, C. W. Oosterlee, R. Wienands, Multigrid for high-dimensional elliptic partial differential equations on non-equidistant grids, SIAM J. Sci. Comput., 29 (2007), 1613-1636. doi: 10.1137/060665695

|

| [40] |

M. Falcone, R. Ferretti, Convergence analysis for a class of high-order semi-Lagrangian avection schemes, SIAM J. Numer. Anal., 35 (1998), 909-940. doi: 10.1137/S0036142994273513

|

| [41] |

R. W. Lee, Option pricing by transform methods: Extensions, unification, and error control, J. Comput. Financ., 7 (2004), 51-86. doi: 10.21314/JCF.2004.121

|

| [42] | F. Fang, C. W. Oosterlee, A novel pricing method for European options based on Fourier-cosine series expansions, SIAM J. Sci. Comput., 31 (2008), 826-848. |

Figures(1) / Tables(7)

Justin W. L. Wan. Multigrid method for pricing European options under the CGMY process[J]. AIMS Mathematics, 2019, 4(6): 1745-1767. doi: 10.3934/math.2019.6.1745

DownLoad:

DownLoad: