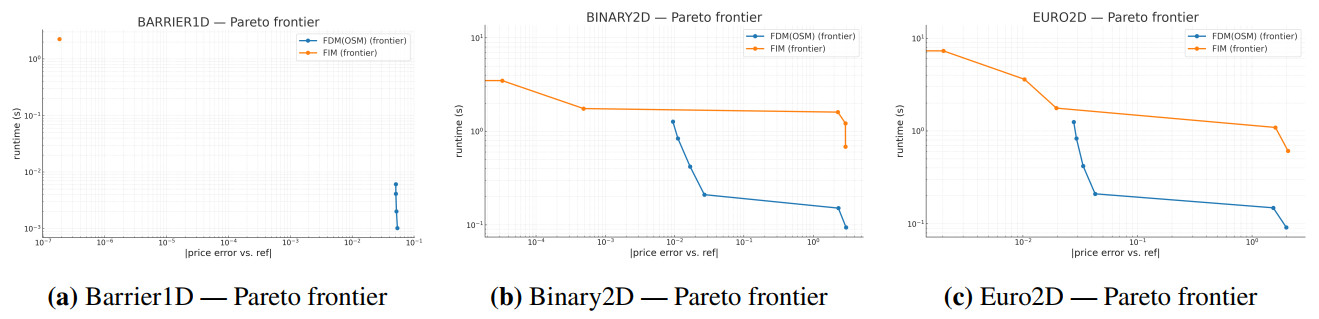

This study introduces the finite integration method (FIM) as a robust numerical approach for pricing equity-linked notes (ELNs). The FIM extends its application beyond vanilla options, effectively addressing the complexities of continuous boundaries and binary payoffs associated with ELNs. We present a comprehensive framework for ELN pricing, including detailed explanations of product structures and a step-by-step description of the FIM methodology. To assess the performance of the FIM, we conduct a comparative analysis against the implicit FDM. Numerical results demonstrate that the FIM outperforms the FDM in terms of reduced pricing errors and more precise hedge parameters (Greeks). We evaluated both one-dimensional barrier options and two-dimensional binary options. Additionally, we proposed an FIM algorithm for pricing a two-dimensional step-down ELN with a knock-in barrier feature. Monte Carlo simulations(MCS) are used as benchmarks to validate the convergence and accuracy of the FIM. The results confirm that the FIM is a robust and practical method for derivative valuation and risk management. Furthermore, the flexibility of the FIM framework allows it to accommodate various complex payoff structures, making it a valuable tool for pricing structured derivatives.

Citation: Yejin Kim, Wooyeol Jeong, Sungchul Lee. A finite integration method for pricing and hedging path-dependent structured derivatives[J]. AIMS Mathematics, 2025, 10(10): 24294-24316. doi: 10.3934/math.20251077

This study introduces the finite integration method (FIM) as a robust numerical approach for pricing equity-linked notes (ELNs). The FIM extends its application beyond vanilla options, effectively addressing the complexities of continuous boundaries and binary payoffs associated with ELNs. We present a comprehensive framework for ELN pricing, including detailed explanations of product structures and a step-by-step description of the FIM methodology. To assess the performance of the FIM, we conduct a comparative analysis against the implicit FDM. Numerical results demonstrate that the FIM outperforms the FDM in terms of reduced pricing errors and more precise hedge parameters (Greeks). We evaluated both one-dimensional barrier options and two-dimensional binary options. Additionally, we proposed an FIM algorithm for pricing a two-dimensional step-down ELN with a knock-in barrier feature. Monte Carlo simulations(MCS) are used as benchmarks to validate the convergence and accuracy of the FIM. The results confirm that the FIM is a robust and practical method for derivative valuation and risk management. Furthermore, the flexibility of the FIM framework allows it to accommodate various complex payoff structures, making it a valuable tool for pricing structured derivatives.

| [1] |

F. Black, M. Scholes, The pricing of options and corporate liabilities, J. Polit. Econ., 81 (1973), 637–654. https://doi.org/10.1086/260062 doi: 10.1086/260062

|

| [2] |

R. C. Merton, Theory of rational option pricing, Bell J. Econ. Manag. Sci., 4 (1973), 141–183. https://doi.org/10.1098/rspb.1973.0010 doi: 10.1098/rspb.1973.0010

|

| [3] |

J. C. Cox, S. A. Ross, M. Rubinstein, Option pricing: A simplified approach, J. Financ. Econ., 7 (1979), 229–263. https://doi.org/10.1016/0304-405X(79)90015-1 doi: 10.1016/0304-405X(79)90015-1

|

| [4] |

F. Soleymani, B. N. Saray, Pricing the financial Heston–Hull–White model with arbitrary correlation factors via an adaptive FDM, Comput. Math. Appl., 77 (2019), 1107–1123. https://doi.org/10.1016/j.camwa.2018.10.047 doi: 10.1016/j.camwa.2018.10.047

|

| [5] | M. L. Mao, W. S. Wang, T. H. Tian, L. H. Wang, Adaptive option pricing based on a posteriori error estimates for fully discrete finite difference methods, J. Comput. Appl. Math., 460 (2025). https://doi.org/10.1016/j.cam.2024.116407 |

| [6] |

J. Persson, L. von Sydow, Pricing american options using a space-time adaptive finite difference method, Math. Comput. Simulat., 80 (2010), 1922–1935. https://doi.org/10.1016/j.matcom.2010.02.008 doi: 10.1016/j.matcom.2010.02.008

|

| [7] |

J. C. Ndogmo, D. B. Ntwiga, High-order accurate implicit methods for barrier option pricing, Appl. Math. Comput., 218 (2011), 2210–2224. https://doi.org/10.1016/j.amc.2011.07.037 doi: 10.1016/j.amc.2011.07.037

|

| [8] |

P. P. Boyle, Y. Tian, An explicit finite difference approach to the pricing of barrier options, Appl. Math. Financ., 5 (1998), 17–43. https://doi.org/10.1353/imag.2003.0128 doi: 10.1353/imag.2003.0128

|

| [9] |

J. Jeon, S. Y. Choi, J. H. Yoon, Analytic valuation of european continuous-installment barrier options, J. Comput. Appl. Math., 363 (2020), 392–412. https://doi.org/10.1016/j.cam.2019.06.021 doi: 10.1016/j.cam.2019.06.021

|

| [10] |

Y. C. Hong, S. Lee, T. G. Li, Numerical method of pricing discretely monitored barrier option, J. Comput. Appl. Math., 278 (2015), 149–161. https://doi.org/10.1016/j.cam.2014.08.022 doi: 10.1016/j.cam.2014.08.022

|

| [11] |

J. Lyu, E. Park, S. Kim, W. Lee, C. Lee, S. Yoon, et al., Optimal non-uniform finite difference grids for the Black–Scholes equations, Math. Comput. Simul., 182 (2021), 690–704. https://doi.org/10.1016/j.matcom.2020.12.002 doi: 10.1016/j.matcom.2020.12.002

|

| [12] |

J. F. Yang, G. L. Li, On sparse grid interpolation for american option pricing with multiple underlying assets, J. Comput. Appl. Math., 464 (2025), 116544. https://doi.org/10.1016/j.cam.2025.116544 doi: 10.1016/j.cam.2025.116544

|

| [13] | M. Briani, L. Caramellino, A. Zanette, A hybrid tree/finite-difference approach for Heston–Hull–White-type models, J. Comput. Financ., 21 (2017), 1–45. |

| [14] |

S. O'Sullivan, C. O'Sullivan, On the acceleration of explicit finite difference methods for option pricing, Quant. Financ., 11 (2011), 1177–1191. https://doi.org/10.1080/14697680903055570 doi: 10.1080/14697680903055570

|

| [15] | D. S. Attipoe, A. Tambue, Convergence of the mimetic finite difference and fitted mimetic finite difference method for options pricing, Appl. Math. Comput., 401 (2021). https://doi.org/10.1016/j.amc.2021.126060 |

| [16] |

P. Roul, V. M. K. P. Goura, A compact finite difference scheme for fractional Black-Scholes option pricing model, Appl. Numer. Math., 166 (2021), 40–60. https://doi.org/10.1016/j.apnum.2021.03.017 doi: 10.1016/j.apnum.2021.03.017

|

| [17] |

H. Lim, S. Lee, G. Kim, Efficient pricing of bermudan options using recombining quadratures, J. Comput. Appl. Math., 271 (2014), 195–205. https://doi.org/10.1016/j.cam.2014.04.007 doi: 10.1016/j.cam.2014.04.007

|

| [18] | M. Huang, G. Luo, A simple and efficient numerical method for pricing discretely monitored early-exercise options, Appl. Math. Comput., 422 (2022). https://doi.org/10.1016/j.amc.2022.126985 |

| [19] |

C. Lee, J. Lyu, E. Park, W. Lee, S. Kim, D. Jeong, et al., Super-fast computation for the three-asset equity-linked securities using the finite difference method, Mathematics, 8 (2020), 307. https://doi.org/10.12946/rg28/307-309 doi: 10.12946/rg28/307-309

|

| [20] | J. P. Fouque, C. H. Han, Y. Z. Lai, Variance reduction for MC/QMC methods to evaluate option prices, In: Recent Advances in Financial Engineering, World Scientific, Singapore, 2009, 27–48. https://doi.org/10.1142/7301 |

| [21] | P. Jäckel, Monte Carlo methods in finance, John Wiley & Sons, Chichester, UK, 2002. |

| [22] |

C. Joy, P. P. Boyle, K. S. Tan, Quasi-Monte Carlo methods in numerical finance, Manag. Sci., 42 (1996), 926–938. https://doi.org/10.1287/mnsc.42.6.926 doi: 10.1287/mnsc.42.6.926

|

| [23] | M. H. Shi, Y. Y. Huang, X. F. Li, Y. L. Lei, J. J. Du, Monte Carlo method in stock trading research based on accelerated diffusion theory with jumps, Physica A, 672 (2025). https://doi.org/10.1016/j.physa.2025.130667 |

| [24] |

V. D. Doan, A. Gaikwad, M. Bossy, F. Baude, I. Stokes-Rees, Parallel pricing algorithms for multi-dimensional bermudan/american options using Monte Carlo methods, Math. Comput. Simulat., 81 (2010), 568–577. https://doi.org/10.1016/j.matcom.2010.08.005 doi: 10.1016/j.matcom.2010.08.005

|

| [25] |

Z. J. He, X. Q. Wang, An integrated quasi-Monte Carlo method for handling high dimensional problems with discontinuities in financial engineering, Comput. Econ., 57 (2020), 693–718. https://doi.org/10.1007/s10614-020-09976-2 doi: 10.1007/s10614-020-09976-2

|

| [26] |

H. W. Teng, M. H. Kang, On accelerating Monte Carlo integration using orthogonal projections, Methodol. Comput. Appl., 24 (2021), 1143–1168. https://doi.org/10.1007/s11009-021-09893-3 doi: 10.1007/s11009-021-09893-3

|

| [27] |

A. D. Andricopoulos, M. Widdicks, P. W. Duck, D. P. Newton, Universal option valuation using quadrature methods, J. Financ. Econ., 67 (2003), 447–471. https://doi.org/10.1016/S0304-405X(02)00257-X doi: 10.1016/S0304-405X(02)00257-X

|

| [28] | D. S. Attipoe, A. Tambue, Novel numerical techniques based on mimetic finite difference method for pricing two dimensional options, Results Appl. Math., 13 (2022). https://doi.org/10.1016/j.rinam.2021.100229 |

| [29] |

S. Kozpınar, M. Uzunca, B. Karasözen, Pricing european and american options under Heston model using discontinuous galerkin finite elements, Math. Comput. Simulat., 177 (2020), 568–587. https://doi.org/10.1016/j.matcom.2020.05.022 doi: 10.1016/j.matcom.2020.05.022

|

| [30] |

Y. M. Lu, Y. D. Lyuu, Very fast algorithms for implied barriers and moving-barrier options pricing, Math. Comput. Simulat., 205 (2023), 251–271. https://doi.org/10.1016/j.matcom.2022.09.018 doi: 10.1016/j.matcom.2022.09.018

|

| [31] | S. E. Fadugba, Homotopy analysis method and its applications in the valuation of european call options with time-fractional Black-Scholes equation, Chaos Soliton. Fract., 141 (2020). https://doi.org/10.1016/j.chaos.2020.110351 |

| [32] | S. M. Nuugulu, F. Gideon, K. C. Patidar, A robust numerical scheme for a time-fractional Black-Scholes partial differential equation describing stock exchange dynamics, Chaos Soliton. Fract., 145 (2021). https://doi.org/10.1016/j.chaos.2021.110753 |

| [33] |

J. R. Liang, J. Wang, W. J. Zhang, W. Y. Qiu, F. Y. Ren, Option pricing of a bi-fractional Black–Merton–Scholes model with the hurst exponent h in [1/2, 1], Appl. Math. Lett., 23 (2010), 859–863. https://doi.org/10.1016/j.aml.2010.03.022 doi: 10.1016/j.aml.2010.03.022

|

| [34] |

M. Rezaei, A. R. Yazdanian, A. Ashrafi, S. M. Mahmoudi, Numerical pricing based on fractional Black–Scholes equation with time-dependent parameters under the cev model: Double barrier options, Comput. Math. Appl., 90 (2021), 104–111. https://doi.org/10.1016/j.camwa.2021.02.021 doi: 10.1016/j.camwa.2021.02.021

|

| [35] | J. H. Chen, X. F. Li, Y. Z. Shao, Numerical analysis of fractional order Black–Scholes option pricing model with band equation method, J. Comput. Appl. Math., 451 (2024). https://doi.org/10.1016/j.cam.2024.115998 |

| [36] | J. Cho, Y. Kim, S. Lee, An accurate and stable numerical method for option hedge parameters, Appl. Math. Comput., 430 (2022). https://doi.org/10.1016/j.amc.2022.127276 |

| [37] |

J. Cho, D. Yang, Y. Kim, S. Lee, An operator splitting method for multi-asset options with the Feynman-Kac formula, Comput. Math. Appl., 135 (2023), 93–101. https://doi.org/10.1016/j.camwa.2023.01.019 doi: 10.1016/j.camwa.2023.01.019

|

| [38] | M. N. Özişik, H. R. B. Orlande, M. J. Colaço, R. M. Cotta, Finite difference methods in heat transfer, CRC Press, 2 Eds., 2017. https://doi.org/10.1201/9781315121475 |

| [39] | P. Glasserman, Monte Carlo methods in financial engineering, Springer, New York, 2003. |

| [40] | E. G. Haug, The complete guide to option pricing formulas, McGraw-Hill, New York, 2 Eds., 2007. |

Figures(9) / Tables(3)

Yejin Kim, Wooyeol Jeong, Sungchul Lee. A finite integration method for pricing and hedging path-dependent structured derivatives[J]. AIMS Mathematics, 2025, 10(10): 24294-24316. doi: 10.3934/math.20251077

DownLoad:

DownLoad: