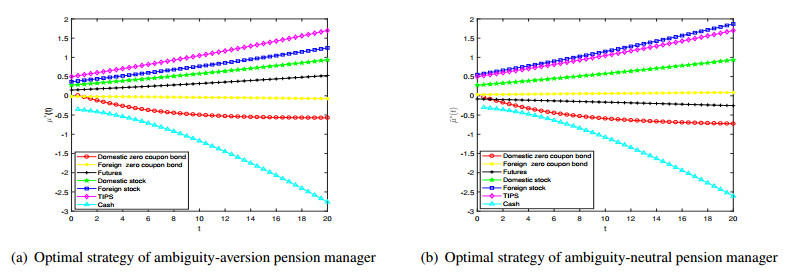

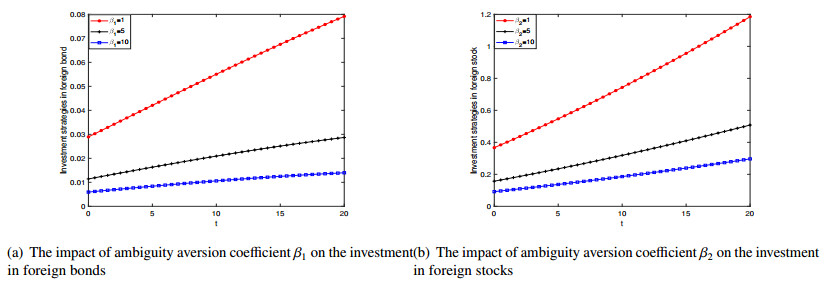

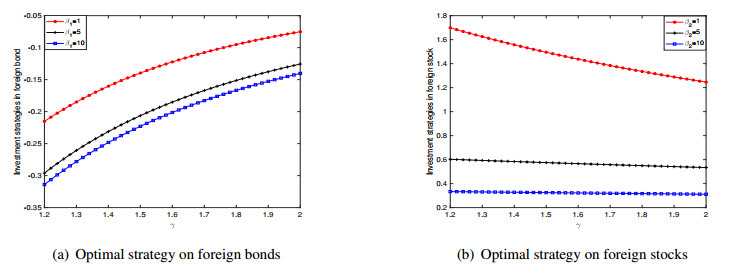

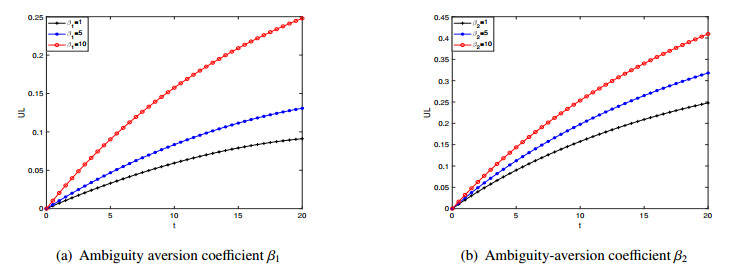

This paper studies the optimal portfolio decisions of participants in defined contribution (DC) pension plans who are able to invest their wealth in transnational securities. More specifically, pension participants can allocate their investments across cash, bonds, domestic stocks, foreign stocks, inflation-indexed instruments, and exchange rate futures. Furthermore, we assume that pension managers face ambiguity regarding the distribution of foreign asset prices. In this context, by employing dynamic programming and the "relative entropy penalty" method, the paper derives robust optimal portfolio strategies for DC pension plan participants, accompanied by a verification theorem. Additionally, we explore two specific scenarios: the optimal investment strategy for pension managers under ambiguity neutrality, and the utility loss incurred by ambiguity-averse fund managers who misapply the optimal investment strategy. Our analysis is illustrated through numerical examples.

Citation: Aimin Song, Pingping Zhao, Xiaoyan Shi. Transnational investment strategies for DC pension plan under inflation and model ambiguity[J]. Electronic Research Archive, 2025, 33(10): 6445-6475. doi: 10.3934/era.2025284

This paper studies the optimal portfolio decisions of participants in defined contribution (DC) pension plans who are able to invest their wealth in transnational securities. More specifically, pension participants can allocate their investments across cash, bonds, domestic stocks, foreign stocks, inflation-indexed instruments, and exchange rate futures. Furthermore, we assume that pension managers face ambiguity regarding the distribution of foreign asset prices. In this context, by employing dynamic programming and the "relative entropy penalty" method, the paper derives robust optimal portfolio strategies for DC pension plan participants, accompanied by a verification theorem. Additionally, we explore two specific scenarios: the optimal investment strategy for pension managers under ambiguity neutrality, and the utility loss incurred by ambiguity-averse fund managers who misapply the optimal investment strategy. Our analysis is illustrated through numerical examples.

| [1] |

Y. Gao, X. Rong, R. Ti, Optimal management of the collective defined contribution pension plan with long-term care insurance, N. Am. Actuarial J., 31 (2025), 1–29. https://doi.org/10.1080/10920277.2025.2532073 doi: 10.1080/10920277.2025.2532073

|

| [2] |

D. Doreleijers, C. Hambel, Dynamic portfolio choice with regret aversion and rejoicing, Finance Res. Lett., 84 (2025), 107762. https://doi.org/10.1016/j.frl.2025.107762 doi: 10.1016/j.frl.2025.107762

|

| [3] |

D. Li, J. Bi, M. Hu, Alpha robust mean variance investment strategy for DC pension plan with uncertainty about jump-diffusion risk, RAIRO Oper. Res., 55 (2021), S2983–S2997. https://doi.org/10.1051/ro/2020132 doi: 10.1051/ro/2020132

|

| [4] |

P. Wang, Z. Li, J. Sun, Robust portfolio choice for a DC pension plan with inflation risk and mean reverting risk premium under ambiguity, Optimization, 70 (2021), 191–224. https://doi.org/10.1080/02331934.2019.1679812 doi: 10.1080/02331934.2019.1679812

|

| [5] |

L. Wang, B. Jia, Equilibrium investment strategies for a defined contribution pension plan with random risk aversion, Insur. Math. Econ., 125 (2025), 103140. https://doi.org/10.1016/j.insmatheco.2025.103140 doi: 10.1016/j.insmatheco.2025.103140

|

| [6] |

Y. Dong, H. Zheng, Optimal investment with S shaped utility and trading and value at risk constraints: An application to defined contribution pension plan, Eur. J. Oper. Res., 281 (2020), 341–356. https://doi.org/10.1016/J.EJOR.2019.08.034 doi: 10.1016/J.EJOR.2019.08.034

|

| [7] | H. Levy, M. Sarnat, International diversification of investment portfolios, Am. Econ. Rev., 60 (1970), 668–675. |

| [8] |

P. Jorion, Asset allocation with hedged and unhedged foreign stocks and bonds, J. Portfolio Manage., 15 (1989), 49–54. https://doi.org/10.3905/JPM.1989.409221 doi: 10.3905/JPM.1989.409221

|

| [9] |

C. Guo, X. Zhuo, C. Constantinescu, O. M. Pamen, Optimal reinsurance-investment strategy under risks of interest rate, exchange rate and inflation, Methodol. Comput. Appl. Probab., 20 (2018), 1477–1502. https://doi.org/10.1007/S11009-018-9630-7 doi: 10.1007/S11009-018-9630-7

|

| [10] | E. Anderson, L. P. Hansen, T. Sargent, Robustness, detection and the price of risk, Manuscr., Stanford, (2000), 19. |

| [11] |

R. Uppal, T. Wang, Model misspecification and underdiversification, J. Finance, 58 (2002), 2465–2486. https://doi.org/10.2139/SSRN.294201 doi: 10.2139/SSRN.294201

|

| [12] |

P. J. Maenhout, Robust portfolio rules and asset pricing, Rev. Financ. Stud., 17 (2004), 951–983. https://doi.org/10.2307/3598055 doi: 10.2307/3598055

|

| [13] |

K. Peijnenburg, Life-cycle asset allocation with ambiguity aversion and learning, J. Financ. Quant. Anal., 53 (2018), 1963–1994. https://doi.org/10.1017/S0022109017001144 doi: 10.1017/S0022109017001144

|

| [14] |

Y. Ait-Sahalia, F. Matthys, Robust consumption and portfolio policies when asset prices can jump, J. Econ. Theory, 179 (2019), 1–56. https://doi.org/10.1016/J.JET.2018.09.006 doi: 10.1016/J.JET.2018.09.006

|

| [15] |

G. Guan, Z. Liang, Robust optimal reinsurance and investment strategies for an AAI with multiple risks, Insur. Math. Econ., 89 (2019), 63–78. https://doi.org/10.1016/J.INSMATHECO.2019.09.004 doi: 10.1016/J.INSMATHECO.2019.09.004

|

| [16] |

D. Kostopoulos, S. Meyer, C. Uhr, Ambiguity about volatility and investor behavior, J. Financ. Econ., 145 (2022), 277–296. https://doi.org/10.1016/j.jfineco.2021.07.004 doi: 10.1016/j.jfineco.2021.07.004

|

| [17] |

I. Baltas, L. Dopierala, K. Kolodziejczyk, M. Szczepanski, G. W. Weber, A. N. Yannacopoulos, Optimal management of defined contribution pension funds under the effect of inflation, mortality and uncertainty, Eur. J. Oper. Res., 298 (2022), 1162–1174. https://doi.org/10.1016/j.ejor.2021.08.038 doi: 10.1016/j.ejor.2021.08.038

|

| [18] |

S. Meyer, U. Charline, Ambiguity and private investors' behavior after forced fund liquidations, J. Financ. Econ., 156 (2024), 103849–103851. https://doi.org/10.1016/j.jfineco.2024.103849 doi: 10.1016/j.jfineco.2024.103849

|

| [19] |

G. Deelstra, M. Grasselli, P. F. Koehl, Optimal investment strategies in the presence of a minimum guarantee, Insur. Math. Econ., 33 (2003), 189–207. https://doi.org/10.1016/S0167-6687(03)00153-7 doi: 10.1016/S0167-6687(03)00153-7

|

| [20] |

N. W. Han, M. W. Hung, Optimal asset allocation for DC pension plans under inflation, Insur. Math. Econ., 51 (2012), 172–181. https://doi.org/10.1016/J.INSMATHECO.2012.03.003 doi: 10.1016/J.INSMATHECO.2012.03.003

|

| [21] |

J. F. Boulier, S. Huang, G. Taillard, Optimal management under stochastic interest rates: the case of a protected defined contribution pension fund, Insur. Math. Econ., 28 (2001), 173–189. https://doi.org/10.1016/S0167-6687(00)00073-1 doi: 10.1016/S0167-6687(00)00073-1

|

| [22] |

A. Lioui, P. Poncet, Optimal currency risk hedging, J. Int. Money Finance, 21 (2002), 241–264. https://doi.org/10.1016/S0261-5606(01)00045-6 doi: 10.1016/S0261-5606(01)00045-6

|

| [23] |

K. I. Amin, R. A. Jarrow, Pricing foreign currency options under stochastic interest rates, J. Int. Money Finance, 10 (1991), 310–329. https://doi.org/10.1016/0261-5606(91)90013-A doi: 10.1016/0261-5606(91)90013-A

|

| [24] |

G. Guan, Z. Liang, Optimal management of DC pension plan in a stochastic interest rate and stochastic volatility framework, Insur. Math. Econ., 57 (2014), 58–66. https://doi.org/10.1016/J.INSMATHECO.2014.05.004 doi: 10.1016/J.INSMATHECO.2014.05.004

|

| [25] |

P. Wang, Z. Li, Robust optimal investment strategy for an AAM of DC pension plans with stochastic interest rate and stochastic volatility, Insur. Math. Econ., 80 (2018), 67–83. https://doi.org/10.1016/J.INSMATHECO.2018.03.003 doi: 10.1016/J.INSMATHECO.2018.03.003

|

| [26] |

E. Bayraktar, Y. Zhang, Minimizing the probability of lifetime ruin under ambiguity aversion, SIAM J. Control Optim., 53 (2015), 58–90. https://doi.org/10.1137/140955999 doi: 10.1137/140955999

|

| [27] |

B. Liu, M. Zhou, Robust portfolio selection for individuals: Minimizing the probability of lifetime ruin, J. Ind. Manage. Optim., 13 (2021), 937–942. https://doi.org/10.3934/JIMO.2020005 doi: 10.3934/JIMO.2020005

|

| [28] |

C. R. Flor, L. S. Larsen, Robust portfolio choice with stochastic interest rates, Ann. Finance, 10 (2014), 243–265. https://doi.org/10.1007/s10436-013-0234-5 doi: 10.1007/s10436-013-0234-5

|

| [29] |

M. Escobar, S. Ferrando, A. Rubtsov, Robust portfolio choice with derivative trading under stochastic volatility, J. Banking Finance, 61 (2015), 142–157. https://doi.org/10.1016/j.jbankfin.2015.08.033 doi: 10.1016/j.jbankfin.2015.08.033

|

| [30] |

N. Branger, L. S. Larsen, C. Munk, Robust portfolio choice with ambiguity and learning about return predictability, J. Banking Finance, 37 (2013), 1397–1411. https://doi.org/10.1016/j.jbankfin.2012.05.009 doi: 10.1016/j.jbankfin.2012.05.009

|

| [31] | M. Taksar, X. D. Zeng, A general stochastic volatility model and optimal portfolio with explicit solutions, in Working Paper, 2009. |

| [32] | H. Kraft, Optimal Portfolios with Stochastic Interest Rates and Defaultable Assets, Springer Science and Business Media, 2004. |

Figures(5) / Tables(1)

Aimin Song, Pingping Zhao, Xiaoyan Shi. Transnational investment strategies for DC pension plan under inflation and model ambiguity[J]. Electronic Research Archive, 2025, 33(10): 6445-6475. doi: 10.3934/era.2025284

DownLoad:

DownLoad: