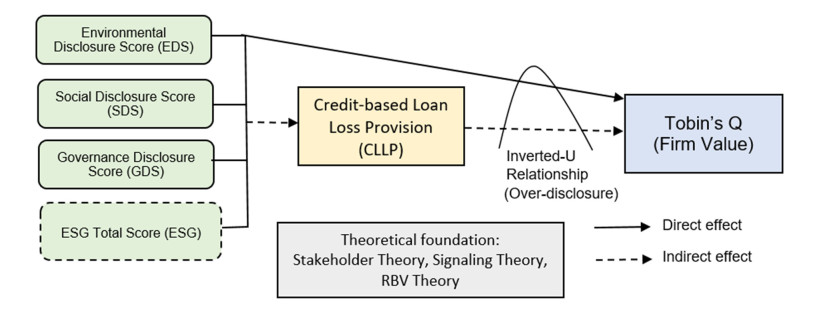

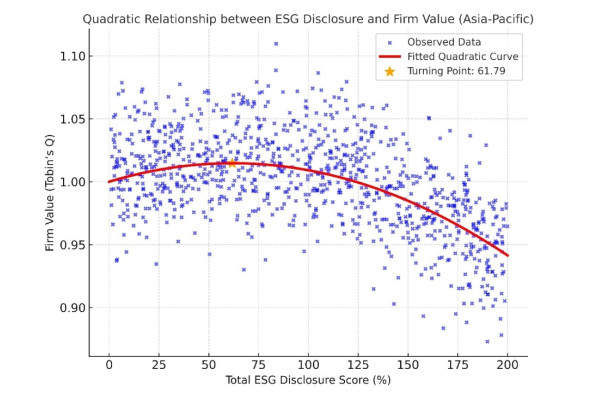

In this study, we investigated the relationship between Environmental, Social, and Governance (ESG) disclosure and firm value in the Asia-Pacific banking sector, based on panel data from 249 publicly listed banks across 18 countries over the period 2009–2023. Under increasing regulatory and market pressures, ESG transparency is often adopted without sufficient internal risk governance, raising concerns of symbolic compliance and greenwashing. To address this gap, we introduced Credit-based Loan Loss Provision (CLLP) as a novel mediating mechanism that captures the integration of ESG into prudential credit risk management. Using a fixed-effects panel regression and a two-stage least squares (2SLS) approach, our findings revealed that ESG disclosure exerts a significantly negative direct effect on firm value, as measured by Tobin's Q, particularly in the absence of credible risk governance. However, when mediated by CLLP, ESG disclosure, across environmental disclosure scores (EDS), social disclosure scores (SDS), and governance disclosure scores (GDS) dimensions, positively and significantly influences firm value. Moreover, a nonlinear analysis revealed an inverted U-shaped relationship, indicating that while moderate ESG disclosure enhances firm value, excessive disclosure may reduce it. These results underscore the importance of aligning ESG reporting with internal risk controls to ensure credibility and market value. The study contributes to the theoretical discourse by reinforcing stakeholder, signaling, legitimacy, and resource-based view perspectives. It offers practical implications for regulators and banking institutions aiming to enhance the quality of ESG disclosure and its integration into risk-based frameworks for sustainable finance.

Citation: Netti Natarida Marpaung, Sugeng Wahyudi, Irene Rini Demi Pangestuti. Green banking in transition: ESG disclosure, credit risk governance, and firm value in an institutionally diverse Asia-Pacific dataset[J]. Green Finance, 2025, 7(4): 689-716. doi: 10.3934/GF.2025026

In this study, we investigated the relationship between Environmental, Social, and Governance (ESG) disclosure and firm value in the Asia-Pacific banking sector, based on panel data from 249 publicly listed banks across 18 countries over the period 2009–2023. Under increasing regulatory and market pressures, ESG transparency is often adopted without sufficient internal risk governance, raising concerns of symbolic compliance and greenwashing. To address this gap, we introduced Credit-based Loan Loss Provision (CLLP) as a novel mediating mechanism that captures the integration of ESG into prudential credit risk management. Using a fixed-effects panel regression and a two-stage least squares (2SLS) approach, our findings revealed that ESG disclosure exerts a significantly negative direct effect on firm value, as measured by Tobin's Q, particularly in the absence of credible risk governance. However, when mediated by CLLP, ESG disclosure, across environmental disclosure scores (EDS), social disclosure scores (SDS), and governance disclosure scores (GDS) dimensions, positively and significantly influences firm value. Moreover, a nonlinear analysis revealed an inverted U-shaped relationship, indicating that while moderate ESG disclosure enhances firm value, excessive disclosure may reduce it. These results underscore the importance of aligning ESG reporting with internal risk controls to ensure credibility and market value. The study contributes to the theoretical discourse by reinforcing stakeholder, signaling, legitimacy, and resource-based view perspectives. It offers practical implications for regulators and banking institutions aiming to enhance the quality of ESG disclosure and its integration into risk-based frameworks for sustainable finance.

| [1] |

Agarwala N, Jana S, Sahu TN (2024) ESG disclosures and corporate performance: A non-linear and disaggregated approach. J Clean Prod 437: 140517. https://doi.org/10.1016/j.jclepro.2023.140517 doi: 10.1016/j.jclepro.2023.140517

|

| [2] |

Atif M, Ali S (2021) Environmental, social and governance disclosure and default risk. Bus Strat Environ 30: 3937–3959. https://doi.org/10.1002/bse.2850 doi: 10.1002/bse.2850

|

| [3] |

Avci SB, Sungu-Esen G (2022) Country-level sustainability and cross-border banking flows. Sustain Account Manag Policy J 13: 626–652. https://doi.org/10.1108/SAMPJ-07-2021-0273 doi: 10.1108/SAMPJ-07-2021-0273

|

| [4] |

Aydoğmuş M, Gülay G, Ergun K (2022) Impact of ESG performance on firm value and profitability. Borsa Istanb Rev 22: S119–S127. https://doi.org/10.1016/j.bir.2022.11.006 doi: 10.1016/j.bir.2022.11.006

|

| [5] |

Bancu A (2024) A meta-analysis of ESG disclosure and company's economic performance. Proc Int Conf Bus Excell 18: 2042–2056. https://doi.org/10.2478/picbe-2024-0173 doi: 10.2478/picbe-2024-0173

|

| [6] |

Barney J (1991) Firm Resources and Sustained Competitive Advantage. J Manag 17: 99–120. https://doi.org/10.1177/014920639101700108 doi: 10.1177/014920639101700108

|

| [7] | Basel Committee (2022) Basel Committee issues principles for the effective management and supervision of climate-related financial risks. Available from: https://www.bis.org/press/p220615.htm. |

| [8] |

Bătae OM, Dragomir VD, Feleagă L (2021) The relationship between environmental, social, and financial performance in the banking sector: A European study. J Clean Prod 290: 125791. https://doi.org/10.1016/j.jclepro.2021.125791 doi: 10.1016/j.jclepro.2021.125791

|

| [9] |

Berg F, Kölbel JF, Rigobon R (2022) Aggregate Confusion: The Divergence of ESG Ratings. Rev Finance 26: 1315–1344. https://doi.org/10.1093/rof/rfac033 doi: 10.1093/rof/rfac033

|

| [10] |

Billor N, Hadi AS, Velleman PF (2000) BACON: blocked adaptive computationally efficient outlier nominators. Comput Stat Data Anal 34: 279–298. https://doi.org/10.1016/S0167-9473(99)00101-2 doi: 10.1016/S0167-9473(99)00101-2

|

| [11] |

Boudriga A, Boulila Taktak N, Jellouli S (2009) Banking supervision and nonperforming loans: A cross‐country analysis. J Financ Econ Policy 1: 286–318. https://doi.org/10.1108/17576380911050043 doi: 10.1108/17576380911050043

|

| [12] |

Bramati CM, Croux C (2007) Robust estimators for the fixed effects panel data model. Econom J 10: 521–540. https://doi.org/10.1111/j.1368-423X.2007.00220.x doi: 10.1111/j.1368-423X.2007.00220.x

|

| [13] |

Breusch TS, Pagan AR (1980) The Lagrange Multiplier Test and its Applications to Model Specification in Econometrics. Rev Econ Stud 47: 239. https://doi.org/10.2307/2297111 doi: 10.2307/2297111

|

| [14] |

Bruno E, Iacoviello G, Giannetti C (2024) Bank credit loss and ESG performance. Finance Res Lett 59: 104719. https://doi.org/10.1016/j.frl.2023.104719 doi: 10.1016/j.frl.2023.104719

|

| [15] |

Butt MN, Baig AS, Seyyed FJ (2023) Tobin's Q approximation as a metric of firm performance: An empirical evaluation. J Strateg Mark 31: 532–548. https://doi.org/10.1080/0965254X.2021.1947875 doi: 10.1080/0965254X.2021.1947875

|

| [16] |

Cantero-Saiz M, Sanfilippo-Azofra S, Torre-Olmo B, et al. (2025) ESG and bank profitability: The moderating role of country sustainability in developing and developed economies. Green Financ 7: 288–331. https://doi.org/10.3934/GF.2025011 doi: 10.3934/GF.2025011

|

| [17] |

Carè R, Lehner O, Weber O (2024) Editorial overview: Climate finance, risks, and accounting. Curr Opin Environ Sustain 70: 101473. https://doi.org/10.1016/j.cosust.2024.101473 doi: 10.1016/j.cosust.2024.101473

|

| [18] | CFA Institute (2019) ESG disclosures in Asia Pacific: A review of ESG disclosure regimes for listed companies in selected markets. Available from: www.cfainstitute.org. |

| [19] |

Chairani C, Siregar SV (2021) The effect of enterprise risk management on financial performance and firm value: The role of environmental, social and governance performance. Meditari Account Res 29: 647–670. https://doi.org/10.1108/MEDAR-09-2019-0549 doi: 10.1108/MEDAR-09-2019-0549

|

| [20] |

Cheng B, Ioannou I, Serafeim G (2014) Corporate social responsibility and access to finance. Strateg Manag J 35: 1–23. https://doi.org/10.1002/smj.2131 doi: 10.1002/smj.2131

|

| [21] |

Cheng R, Kim H, Ryu D (2024) ESG performance and firm value in the Chinese market. Invest Anal J 53: 1–15. https://doi.org/10.1080/10293523.2023.2218124 doi: 10.1080/10293523.2023.2218124

|

| [22] |

de Silva Lokuwaduge CS, De Silva KM (2022) ESG Risk Disclosure and the Risk of Green Washing. Australas Bus Acc Finance J 16: 146–159. https://doi.org/10.14453/aabfj.v16i1.10 doi: 10.14453/aabfj.v16i1.10

|

| [23] |

Delmas MA, Burbano VC (2011) The Drivers of Greenwashing. Calif Manag Rev 54: 64–87. https://doi.org/10.1525/cmr.2011.54.1.64 doi: 10.1525/cmr.2011.54.1.64

|

| [24] |

Dhaliwal DS, Li OZ, Tsang A, et al. (2011) Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting. Account Rev 86: 59–100. https://doi.org/10.2308/accr.00000005 doi: 10.2308/accr.00000005

|

| [25] |

Ding L, Cui Z, Li J (2024) Risk management and corporate ESG performance: The mediating effect of financial performance. Financ Res Lett 69: 106274. https://doi.org/10.1016/j.frl.2024.106274 doi: 10.1016/j.frl.2024.106274

|

| [26] |

Drukker DM (2003) Testing for Serial Correlation in Linear Panel-data Models. Stata J 3: 168–177. https://doi.org/10.1177/1536867X0300300206 doi: 10.1177/1536867X0300300206

|

| [27] |

Duan K, Qin C, Ma S, et al. (2025) Impact of ESG disclosure on corporate sustainability. Financ Res Lett 78: 107134. https://doi.org/10.1016/j.frl.2025.107134 doi: 10.1016/j.frl.2025.107134

|

| [28] |

Eriandani R, Winarno WA (2024) ESG Risk and Firm Value: The Role of Materiality in Sustainability Reporting. Qual Innov Prosper 28: 16–34. https://doi.org/10.12776/qip.v28i2.2019 doi: 10.12776/qip.v28i2.2019

|

| [29] |

Ersoy E, Swiecka B, Grima S, et al. (2022) The Impact of ESG Scores on Bank Market Value? Evidence from the U.S. Banking Industry. Sustainability 14: 9527. https://doi.org/10.3390/su14159527 doi: 10.3390/su14159527

|

| [30] | European Commission (2019) Regulation (EU) 2019/2088 on sustainability-related disclosures in the financial services sector. Available from: https://eur-lex.europa.eu/eli/reg/2019/2088/oj. |

| [31] |

Fatemi A, Glaum M, Kaiser S (2018) ESG performance and firm value: The moderating role of disclosure. Glob Finance J 38: 45–64. https://doi.org/10.1016/j.gfj.2017.03.001 doi: 10.1016/j.gfj.2017.03.001

|

| [32] | Financial Stability Board (2017) Recommendations of the task force on climate-related financial disclosures. Available from: https://www.fsb.org/2017/06/task-force-publishes-recommendations-on-climate-related-financial-disclosures. |

| [33] | Freeman RE (1984) Strategic Management: A Stakeholder Approach. Cambridge University Press. |

| [34] |

Gunarathne ADN, Lee K, Hitigala Kaluarachchilage PK (2021) Institutional pressures, environmental management strategy, and organizational performance: The role of environmental management accounting. Bus Strat Environ 30: 825–839. https://doi.org/10.1002/bse.2656 doi: 10.1002/bse.2656

|

| [35] |

Halunga AG, Orme CD, Yamagata T (2017) A heteroskedasticity robust Breusch–Pagan test for Contemporaneous correlation in dynamic panel data models. J Econom 198: 209–230. https://doi.org/10.1016/j.jeconom.2016.12.005 doi: 10.1016/j.jeconom.2016.12.005

|

| [36] |

Hao X, Tian T, Dong L, et al. (2025) Unmasking greenwashing in ESG disclosure: Insights from evolutionary game analysis. Ann Oper Res 1–29. https://doi.org/10.1007/s10479-025-06538-3 doi: 10.1007/s10479-025-06538-3

|

| [37] |

Helfaya A, Aboud A, Amin E (2023) An examination of corporate environmental goals disclosure, sustainability performance and firm value – An Egyptian evidence. J Int Account Audit Tax 52: 100561. https://doi.org/10.1016/j.intaccaudtax.2023.100561 doi: 10.1016/j.intaccaudtax.2023.100561

|

| [38] |

Ioannou I, Serafeim G (2015) The impact of corporate social responsibility on investment recommendations: Analysts' perceptions and shifting institutional logics. Strategic Manag J 36: 1053–1081. https://doi.org/10.1002/smj.2268 doi: 10.1002/smj.2268

|

| [39] |

Jiraporn P, Jiraporn N, Boeprasert A, et al. (2014) Does Corporate Social Responsibility (CSR) Improve Credit Ratings? Evidence from Geographic Identification. Financ Manag 43: 505–531. https://doi.org/10.1111/fima.12044 doi: 10.1111/fima.12044

|

| [40] |

Krasodomska J, Eisenschmidt K (2025) "G" and ESG Strategy Integration and Disclosure: Exploring the Governance‐Related Factors That Influence Companies' Decision‐Making. Corp Soc Responsib Environ Manag 32: 2681–2696. https://doi.org/10.1002/csr.3091 doi: 10.1002/csr.3091

|

| [41] |

Liang H, Renneboog L (2017) On the Foundations of Corporate Social Responsibility. J Finance 72: 853–910. https://doi.org/10.1111/jofi.12487 doi: 10.1111/jofi.12487

|

| [42] |

Liu Z (2024) The impact of ESG information disclosure on audit quality (Review). Finance Econ 1: 95–102. https://doi.org/10.61173/y8vn9y49 doi: 10.61173/y8vn9y49

|

| [43] |

Marquis C, Qian C (2014) Corporate Social Responsibility Reporting in China: Symbol or Substance? Organ Sci 25: 127–148. https://doi.org/10.1287/orsc.2013.0837 doi: 10.1287/orsc.2013.0837

|

| [44] | Migliorelli M, Dessertine P (2020) Sustainability and financial risks. Springer. https://doi.org/10.1007/978-3-030-54530-7 |

| [45] |

Nguyen KQT (2025) Macro-economic factors affect capital adequacy ratio at Vietnamese commercial banks. Int J Procurement Manag 22: 152–171. https://doi.org/10.1504/IJPM.2025.144003 doi: 10.1504/IJPM.2025.144003

|

| [46] | OECD (2020) OECD business and finance Outlook 2020. https://doi.org/10.1787/eb61fd29-en |

| [47] | OECD (2023) Sustainable finance in Asia. https://doi.org/10.1787/bde9ec0d-en |

| [48] |

Ozili PK (2023) Bank loan loss provisioning for sustainable development: The case for a sustainable or green loan loss provisioning system. J Sustain Finance Invest, 1–13. https://doi.org/10.1080/20430795.2022.2163847 doi: 10.1080/20430795.2022.2163847

|

| [49] |

Pasamar S, Bornay-Barrachina M, Morales-Sánchez R (2023) Institutional pressures for sustainability: A triple bottom line approach. Eur J Manag Bus Econ 34: 460–484. https://doi.org/10.1108/EJMBE-07-2022-0241 doi: 10.1108/EJMBE-07-2022-0241

|

| [50] | Ramsey JB (1969) Tests for Specification Errors in Classical Linear Least-Squares Regression Analysis. J R Stat Soc 31: 350–371. http://www.jstor.org/stable/2984219 |

| [51] |

Salem MRM, Shahimi S, Alma'amun S (2024) Does Mediation Matter in Explaining the Relationship between ESG and Bank Financial Performance? A Scoping Review. J Risk Financ Manag 17: 350. https://doi.org/10.3390/jrfm17080350 doi: 10.3390/jrfm17080350

|

| [52] |

Singhania M, Gupta D (2024) Impact of Environmental, Social and Governance (ESG) disclosure on firm risk: A meta‐analytical review. Corp Soc Responsib Environ Manag 31: 3573–3613. https://doi.org/10.1002/csr.2725 doi: 10.1002/csr.2725

|

| [53] |

Spence M (1973) Job Market Signaling. Q J Econ 87: 355. https://doi.org/10.2307/1882010 doi: 10.2307/1882010

|

| [54] | Stock JH, Yogo M (2005) Testing for Weak Instruments in Linear IV Regression. Identification and Inference for Econometric Models. Cambridge University Press. https://doi.org/10.1017/CBO9780511614491.006 |

| [55] |

Suchman MC (1995) Managing Legitimacy: Strategic and Institutional Approaches. Acad Manage Rev 20: 571–610. https://doi.org/10.5465/amr.1995.9508080331 doi: 10.5465/amr.1995.9508080331

|

| [56] |

Sullivan JH, Warkentin M, Wallace L (2021) So many ways for assessing outliers: What really works and does it matter? J Bus Res 132: 530–543. https://doi.org/10.1016/j.jbusres.2021.03.066 doi: 10.1016/j.jbusres.2021.03.066

|

| [57] |

Tamasiga P, Onyeaka H, Bakwena M, et al. (2024) Beyond compliance: Evaluating the role of environmental, social and governance disclosures in enhancing firm value and performance. SN Bus Econ 4: 118. https://doi.org/10.1007/s43546-024-00714-6 doi: 10.1007/s43546-024-00714-6

|

| [58] |

Teng X, Ge Y, Wu KS, et al. (2022) Too little or too much? Exploring the inverted U-shaped nexus between voluntary environmental, social and governance and corporate financial performance. Front Environ Sci 10: 969721. https://doi.org/10.3389/fenvs.2022.969721 doi: 10.3389/fenvs.2022.969721

|

| [59] |

Testa F, Boiral O, Iraldo F (2018) Internalization of Environmental Practices and Institutional Complexity: Can Stakeholders Pressures Encourage Greenwashing? J Bus Ethics 147: 287–307. https://doi.org/10.1007/s10551-015-2960-2 doi: 10.1007/s10551-015-2960-2

|

| [60] |

Thompson CG, Kim RS, Aloe AM, et al. (2017) Extracting the Variance Inflation Factor and Other Multicollinearity Diagnostics from Typical Regression Results. Basic Appl Soc Psychol 39: 81–90. https://doi.org/10.1080/01973533.2016.1277529 doi: 10.1080/01973533.2016.1277529

|

| [61] | UNEP FI (2024) Responsible Banking – Priorities and Blueprint for a Sustainable Future. United Nations Environment Programme Finance Initiative. Available from: https://www.unepfi.org/industries/banking/responsible-banking-priorities-and-blueprint-for-a-sustainable-future/. |

| [62] | UNDP (2024) Asia In Focus: ESG Investing And The Business And Human Rights Agenda. Business and Human Rights, United Nations Development Programme (UNDP) C. Available from: https://www.undp.org/sites/g/files/zskgke326/files/2024-06/final_esg_investment_in_asia_report.pdf. |

| [63] |

Windmeijer F (2025) The robust F-statistic as a test for weak instruments. J Econom 247: 105951. https://doi.org/10.1016/j.jeconom.2025.105951 doi: 10.1016/j.jeconom.2025.105951

|

| [64] | Wooldridge JM (2010) Econometric Analysis of Cross Section and Panel Data. The MIT Press. Available from: http://www.jstor.org/stable/j.ctt5hhcfr. |

| [65] |

Xiao Z, Wang Y, Guo D (2022) Will Greenwashing Result in Brand Avoidance? A Moderated Mediation Model. Sustainability 14: 7204. https://doi.org/10.3390/su14127204 doi: 10.3390/su14127204

|

| [66] |

Xu W, Li M, Xu S (2023) Unveiling the "Veil" of information disclosure: Sustainability reporting "greenwashing" and "shared value." PLoS One 18: e0279904. https://doi.org/10.1371/journal.pone.0279904 doi: 10.1371/journal.pone.0279904

|

| [67] |

Zaleski PA (2024) A useful interpretation of firm level Tobin's q. Manag Decis Econ 45: 5381–5389. https://doi.org/10.1002/mde.4332 doi: 10.1002/mde.4332

|

Figures(2) / Tables(16)

Netti Natarida Marpaung, Sugeng Wahyudi, Irene Rini Demi Pangestuti. Green banking in transition: ESG disclosure, credit risk governance, and firm value in an institutionally diverse Asia-Pacific dataset[J]. Green Finance, 2025, 7(4): 689-716. doi: 10.3934/GF.2025026

DownLoad:

DownLoad: