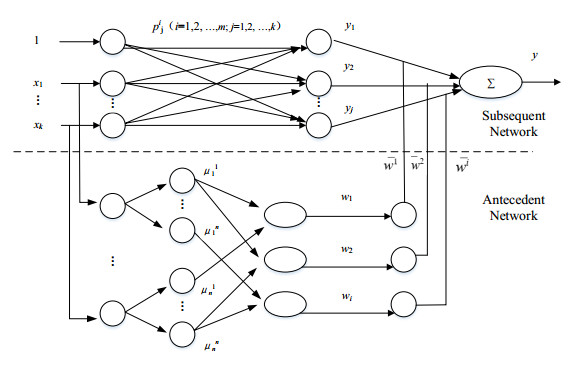

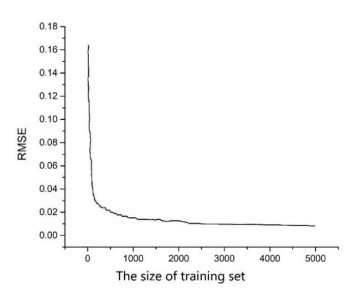

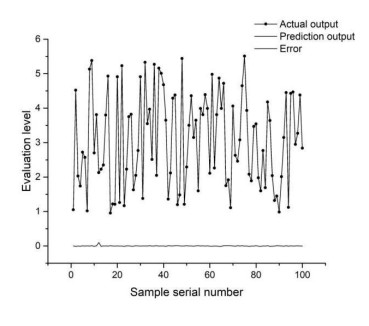

In China, farmers' loan difficulties have become a major problem restricting increases in farmers' incomes and the economic development of rural areas. The existing studies of the management and control of farmers' credit risk have mostly been pre-management, which cannot efficiently prevent and reduce the occurrence of farmers' credit risk in time. This paper uses the T-S neural network model to build a farmers' credit risk early warning system so that formal financial institutions can predict the occurrence of and changes in the farmers' credit risks in a timely manner and quickly undertake countermeasures to reduce losses. After training and testing, a model with a higher degree of fit is used to analyze the credit level of farmers in Shaanxi Province from 2016 to 2018. The results demonstrate that the credit level of farmers in this area is continuously improving, in agreement with the actual situation. The results also show that the prediction accuracy of the T-S fuzzy neural network is high, verifying the rationality of the selection of test samples.

Citation: Hui Wang. Model and application of farmers' credit risk early warning system based on T-S fuzzy neural network application[J]. Mathematical Biosciences and Engineering, 2022, 19(8): 7886-7898. doi: 10.3934/mbe.2022368

In China, farmers' loan difficulties have become a major problem restricting increases in farmers' incomes and the economic development of rural areas. The existing studies of the management and control of farmers' credit risk have mostly been pre-management, which cannot efficiently prevent and reduce the occurrence of farmers' credit risk in time. This paper uses the T-S neural network model to build a farmers' credit risk early warning system so that formal financial institutions can predict the occurrence of and changes in the farmers' credit risks in a timely manner and quickly undertake countermeasures to reduce losses. After training and testing, a model with a higher degree of fit is used to analyze the credit level of farmers in Shaanxi Province from 2016 to 2018. The results demonstrate that the credit level of farmers in this area is continuously improving, in agreement with the actual situation. The results also show that the prediction accuracy of the T-S fuzzy neural network is high, verifying the rationality of the selection of test samples.

| [1] | B. F. Shi, J. Wang, Credit rating model of farmers' microloans based on ELECTRE Ⅲ, J. Sys. Manag., 27 (2018), 854–862. |

| [2] |

N. A. Jatto, T. O. Obalola, E. O. Okebiorun, Reasons for delay in repayment of agricultural loan by farmers in Kwara State, Nigeria, Asian J. Agri. Exten. Eco. Soc., 31 (2019), 1–4. https://doi.org/10.9734/ajaees/2019/v31i230126 doi: 10.9734/ajaees/2019/v31i230126

|

| [3] |

L. Li, Z. Y. Zhang, An empirical analysis of the impact of farmers' quality on farmers' credit—Based on the data of 16,101 farmers' loans in "agricultural staging", J. China Agri. Univer., 24 (2019), 206–216. https://doi.org/10.11841/j.issn.1007-4333.2019.01.24 doi: 10.11841/j.issn.1007-4333.2019.01.24

|

| [4] | Y. P. Zhang, Research on the financial needs of rural households under the background of land ownership confirmation: Time differences, influencing factors and default risks, Finan. Theo. Prac., 9 (2020), 35–41. |

| [5] | Y. J. Ma, R. Kong, Research on credit risk measurement of farmers' formal financing based on stepwise discriminant analysis method, Guangdong Agri. Sci., 20 (2011), 218–220. |

| [6] | H. Wang, J. Wang, An empirical study on credit risk evaluation of farmers—Based on the principle of improved fuzzy clustering without weight value, Jiangsu Agri. Sci., 48 (2020), 301–307. |

| [7] | Y. Wang, Research on credit risk assessment of Chinese farmers' micro-loans—Based on fuzzy comprehensive evaluation model, Southwest Finan., 8 (2010), 60–62. |

| [8] | J. J. Wu, K. Zhang, Research on the rating model of new rural youth users—Based on fuzzy comprehensive evaluation model, Finan. Theory Prac., 5 (2011), 45–48. |

| [9] | L. Chang, F. Liang, Y. Jiang, X. P. Xiong, The application of probabilistic neural network in the credit evaluation of farmers, Wuhan Finan., 11 (2009), 45–47. |

| [10] |

S. Y. Chen, G. H. Fang, X. F. Huang, Y. H. Zhang, Water quality prediction model of a water diversion project based on the improved artificial be colony back propagation neural network. Water, 10 (2018), 806. https://doi.org/10.3390/w10060806 doi: 10.3390/w10060806

|

| [11] |

J. B. Yu, S. J. Wang, L. F. Xi, Evolving artificial neural networks using an improved PSO and DPSO, Neurocomputing, 71 (2008), 1054–1060. https://doi.org/10.1016/j.neucom.2007.10.013 doi: 10.1016/j.neucom.2007.10.013

|

| [12] |

C. Yang, S. J. Lv, F. Gao, Water pollution evaluation in lakes based on factor analysis-fuzzy neural network, Chem. Engi. Tran., 66 (2018), 613–618. https://doi.org/10.1016/j.cej.2017.09.183 doi: 10.1016/j.cej.2017.09.183

|

| [13] | S. Cong, Neural network theory and application for MATLAB toolbox (3rd edition), Hefei, China, University of Science and Technology of China Press, 2009. |

| [14] | F. Shi, X. C. Wang, L. Yu, L. Yang, MATLAB neural network was used to analyze 30 cases, Beijing China: Beihang University Press, 2010. |

| [15] | Q. L. Pei, Y. Yu, X. Y. Zhuang, Application research on safety risk early warning of subway deep foundation pit based on BIM technology, Cons. Tech., 50 (2021), 4–6. |

| [16] | C. Yang, Y. K. Guo, L. X. Zheng, C. G. Li, H. F. Jing, Construction of training samples of TS fuzzy neural network model and its application in water quality evaluation of Mingcui Lake, Res. Prog. Hydrodyn., 35 (2020), 356–366. |

| [17] | Standard & poor's Ratings Services, S&P's study of China's top corpotates highlights their significant financial risk, Standard & Poor's Ratings Services, September 13, 2012,175–199. |

| [18] | Agricultural Bank of China, Administrative Measures for the Credit Rating Evaluation of Agricultural Bank of China's "Agriculture, Rural Areas and Farmers", Agricultural Bank of China, 2008. |

| [19] | Industrial and Commercial Bank of China, Notice on Printing and Distributing the "Measures for the Credit Rating of Small Business Corporate Clients of Industrial and Commercial Bank of China", Industrial and Commercial Bank of China, ICBC, No. 78. |

| [20] | Postal Savings Bank of China, Credit Rating Form of Rural Households of Postal Savings Bank of China, Postal Savings Bank of China, 2009. |

| [21] | D. Wang, The inhibitory effect of farm household classification management on microfinance default risk: mechanism and empirical evidence, Wuhan Finan., 8 (2020), 79–84. |

| [22] | Z. C. Zhao, G. T. Chi, X. P. Bai, Mining the key default characteristics of farmers based on the least significant difference method, Syst. Eng. Theo. Prac., 40 (2020), 2339–2351. |

| [23] | J. G. Zou, M. X. Li, Research on farmer credit enhancement from the perspective of agricultural supply chain finance, Theo. Prac. Finan. Eco., 40 (2019), 32–38. |

Figures(6) / Tables(2)

Hui Wang. Model and application of farmers' credit risk early warning system based on T-S fuzzy neural network application[J]. Mathematical Biosciences and Engineering, 2022, 19(8): 7886-7898. doi: 10.3934/mbe.2022368

DownLoad:

DownLoad: