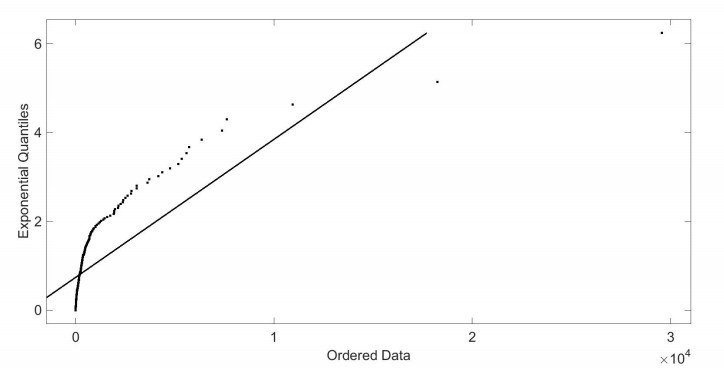

Catastrophe reinsurance is an important way to prevent and resolve catastrophe risks. As a consequence, the pricing of catastrophe reinsurance becomes a core problem in catastrophic risk management field. Due to the severity of catastrophe loss, the Peak Over Threshold (POT) model in extreme value theory (EVT) is extensively applied to capture the tail characteristics of catastrophic loss distribution. However, there is little research available on the pricing formula of catastrophe excess of loss (Cat XL) reinsurance when the catastrophe loss is modeled by POT. In the context of POT model, we distinguish three different relations between retention and threshold, and then prove the explicit pricing formula respectively under the standard deviation premium principle. Furthermore, we fit POT model to the earthquake loss data in China during 1990–2016. Finally, we give the prices of earthquake reinsurance for different retention cases. The computational results illustrate that the pricing formulas obtained in this paper are valid and can provide basis for the pricing of Cat XL reinsurance contracts.

Citation: Wen Chao. Pricing catastrophe reinsurance under the standard deviation premium principle[J]. AIMS Mathematics, 2022, 7(3): 4472-4484. doi: 10.3934/math.2022249

Catastrophe reinsurance is an important way to prevent and resolve catastrophe risks. As a consequence, the pricing of catastrophe reinsurance becomes a core problem in catastrophic risk management field. Due to the severity of catastrophe loss, the Peak Over Threshold (POT) model in extreme value theory (EVT) is extensively applied to capture the tail characteristics of catastrophic loss distribution. However, there is little research available on the pricing formula of catastrophe excess of loss (Cat XL) reinsurance when the catastrophe loss is modeled by POT. In the context of POT model, we distinguish three different relations between retention and threshold, and then prove the explicit pricing formula respectively under the standard deviation premium principle. Furthermore, we fit POT model to the earthquake loss data in China during 1990–2016. Finally, we give the prices of earthquake reinsurance for different retention cases. The computational results illustrate that the pricing formulas obtained in this paper are valid and can provide basis for the pricing of Cat XL reinsurance contracts.

| [1] |

K. Antonio, R. Plat, Micro-level stochastic loss reserving for general insurance, Scand. Actuar. J., 2014 (2014), 113–145. http://dx.doi.org/10.2139/ssrn.1620446 doi: 10.2139/ssrn.1620446

|

| [2] |

A. A. Balkema, L. de Haan, Residual life time at great age, Ann. Probab., 2 (1974), 792–804. http://dx.doi.org/10.1214/aop/1176996548 doi: 10.1214/aop/1176996548

|

| [3] |

W. Chao, Valuing multirisks catastrophe reinsurance based on the Cox-Ingersoll-Ross (CIR) model, Discrete Dyn. Nat. Soc., 2021 (2021), 1–8. http://dx.doi.org/10.1155/2021/8818486 doi: 10.1155/2021/8818486

|

| [4] |

W. Chao, H. W. Zhou, Multiple-event catastrophe bond pricing based on Cox-Ingersoll-Ross model, Discrete Dyn. Nat. Soc., 2018 (2018), 1–9. http://dx.doi.org/10.1155/2018/5068480 doi: 10.1155/2018/5068480

|

| [5] |

S. H. Cox, H. W. Pedersen, Catastrophe risk bonds, N. Am. Actuar. J., 4 (2000), 56–82. http://dx.doi.org/10.1080/10920277.2000.10595938 doi: 10.1080/10920277.2000.10595938

|

| [6] | C. D. Daykin, T. Pentikäinen, M. Pesonen, Practical risk theory for actuaries, London: Chapman and Hall, 1994. |

| [7] |

M. Egami, V. R. Young, Indifference prices of structured catastrophe (CAT) bonds, Insur. Math. Econ., 42 (2008), 771–778. http://dx.doi.org/10.1016/j.insmatheco.2007.08.004 doi: 10.1016/j.insmatheco.2007.08.004

|

| [8] |

E. Ekheden, O. Hössjer, Pricing catastrophe risk in life (re)insurance, Scand. Actuar. J., 4 (2014), 352–367. http://dx.doi.org/10.1080/03461238.2012.695747 doi: 10.1080/03461238.2012.695747

|

| [9] | P. Embrechts, C. Klüppelberg, T. Mikosch, Modeling extremal events for insurance and finance, Berlin: Springer, 1997. http://dx.doi.org/10.1007/978-3-642-33483-2 |

| [10] |

S. Finken, C. Laux, Catastrophe bonds and reinsurance: The competitive effect of information-insensitive triggers, J. Risk Insur., 76 (2009), 579–605. http://dx.doi.org/10.1111/j.1539-6975.2009.01317.x doi: 10.1111/j.1539-6975.2009.01317.x

|

| [11] |

M. N. Giuricich, K. Burnecki, Modelling of left-truncated heavy-tailed data with application to catastrophe bond pricing, Phys. A: Stat. Mech. Appl., 525 (2019), 498–513. http://dx.doi.org/10.1016/j.physa.2019.03.073 doi: 10.1016/j.physa.2019.03.073

|

| [12] | M. Harbitz, Catastrophe covers in life assurance, In: Transactions of international congress of actuaries, 3 (1992), 109–119. http://dx.doi.org/10.1016/0167-6687(94)90441-3 |

| [13] |

W. K. Härdle, B. L. Cabrera, Calibrating CAT bonds for Mexican earthquakes, J. Risk Insur., 77 (2010), 625–650. http://dx.doi.org/10.1111/j.1539-6975.2010.01355.x doi: 10.1111/j.1539-6975.2010.01355.x

|

| [14] |

N. Karagiannis, H. Assa, A. A. Pantelous, C. G. Turvey, Modelling and pricing of catastrophe risk bonds with a temperature-based agricultural application, Quant. Finance, 16 (2016), 1949–1959. http://dx.doi.org/10.1080/14697688.2016.1211791 doi: 10.1080/14697688.2016.1211791

|

| [15] |

M. Leppisaari, Modeling catastrophic deaths using EVT with a microsimulation approach to reinsurance pricing, Scand. Actuar. J., 2016 (2016), 113–145. http://dx.doi.org/10.1080/03461238.2014.910833 doi: 10.1080/03461238.2014.910833

|

| [16] | J. Liu, Y. Li, Empirical study on earthquake losses distribution and CAT bond pricing in China (in Chinese), Finance Trade Res., 20 (2009), 82–88. |

| [17] |

Z. G. Ma, C. Q. Ma, S. T. Xiao, Pricing zero-coupon catastrophe bonds using EVT with doubly stochastic poisson arrivals, Discrete Dyn. Nat. Soc., 2017 (2017), 1–14. http://dx.doi.org/10.1155/2017/3279647 doi: 10.1155/2017/3279647

|

| [18] |

P. Nowak, M. Romaniuk, Pricing and simulations of catastrophe bonds, Insur. Math. Econ., 52 (2013), 18–28. http://dx.doi.org/10.1016/j.insmatheco.2012.10.006 doi: 10.1016/j.insmatheco.2012.10.006

|

| [19] |

J. Pickands, The two-dimensional possion process and external process, J. Appl. Probab., 8 (1971), 745–756. http://dx.doi.org/10.1017/s0021900200114640 doi: 10.1017/s0021900200114640

|

| [20] |

J. Pickands, Statistical inference using extreme order statistics, Ann. Stat., 3 (1975), 119–131. http://dx.doi.org/10.1214/aos/1176343003 doi: 10.1214/aos/1176343003

|

| [21] |

M. Pigeon, K. Antonio, M. Denuit, Individual loss reserving with the multivariate skew normal framework, Astin Bull., 43 (2013), 399–428. http://dx.doi.org/10.1017/asb.2013.20 doi: 10.1017/asb.2013.20

|

| [22] |

J. Shao, A. Papaioannou, A. Pantelous, Pricing and simulating catastrophe risk bonds in a Markov-dependent environment, Appl. Math. Comput., 309 (2017), 68–84. http://dx.doi.org/10.1016/j.amc.2017.03.041 doi: 10.1016/j.amc.2017.03.041

|

| [23] | P. Strickler, Rückversicherung des kumulrisikos in der lebensversicherung, In: XVI International Congress of Actuaries in Brussels, 1 (1960), 666–679. |

| [24] |

D. A. Trottier, V. S. Lai, Reinsurance or CAT bond? How to optimally combine both, J. Fixed Income Fall, 27 (2017), 65–87. http://dx.doi.org/10.3905/jfi.2017.27.2.065 doi: 10.3905/jfi.2017.27.2.065

|

| [25] |

H. Q. Xiao, S. W. Meng, EVT and its application to pricing of catastrophe reinsurance (in Chinese), J. Appl. Stat. Manage., 32 (2013), 240–246. http://dx.doi.org/10.13860/j.cnki.sltj.2013.02.003 doi: 10.13860/j.cnki.sltj.2013.02.003

|

| [26] |

V. R. Young, Pricing in an incomplete market with an affine term stucture, Math. Finance, 14 (2004), 359–381. http://dx.doi.org/10.1111/j.0960-1627.2004.00195.x doi: 10.1111/j.0960-1627.2004.00195.x

|

| [27] |

A. A. Zimbidis, N. E. Frangos, A. A. Pantelous, Modeling earthquake risk via extreme value theory and pricing the respective catastrophe bonds, ASTIN Bull.: J. IAA, 37 (2007), 163–183. http://dx.doi.org/10.2143/AST.37.1.2020804 doi: 10.2143/AST.37.1.2020804

|

Figures(4) / Tables(3)

Wen Chao. Pricing catastrophe reinsurance under the standard deviation premium principle[J]. AIMS Mathematics, 2022, 7(3): 4472-4484. doi: 10.3934/math.2022249

DownLoad:

DownLoad: