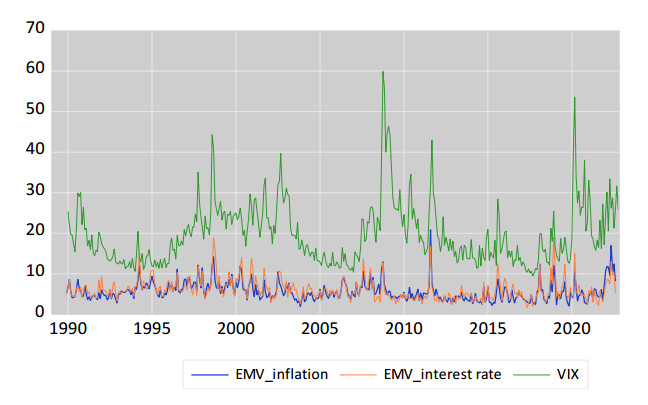

We examine the relation between stock market returns and inflation expectations using data for 20 advanced countries. Evidence reveals that a negative relation presents in each of 18 countries; the exceptions are Brazil and Russia. The uncertainty hypothesis is established via evidence that U.S. inflation positively increases equity market volatility (EMV), which has a negative impact on U.S. and global stock returns. Evidence leads to the conclusion that both expected domestic inflation and EMV have adverse impacts on stock returns. The model is robust with different formations of inflation expectations and whether the test equations are examined using nominal or real stock returns.

Citation: Thomas C. Chiang. Stock returns and inflation expectations: Evidence from 20 major countries[J]. Quantitative Finance and Economics, 2023, 7(4): 538-568. doi: 10.3934/QFE.2023027

We examine the relation between stock market returns and inflation expectations using data for 20 advanced countries. Evidence reveals that a negative relation presents in each of 18 countries; the exceptions are Brazil and Russia. The uncertainty hypothesis is established via evidence that U.S. inflation positively increases equity market volatility (EMV), which has a negative impact on U.S. and global stock returns. Evidence leads to the conclusion that both expected domestic inflation and EMV have adverse impacts on stock returns. The model is robust with different formations of inflation expectations and whether the test equations are examined using nominal or real stock returns.

| [1] |

Al-Khazali OM (2003) Stock prices, inflation, and output: Evidence from the emerging markets. J Emerg Mark Financ 2: 287–314. https://doi.org/10.1177/097265270300200302 doi: 10.1177/097265270300200302

|

| [2] |

Baker SR, Bloom N, Davis SJ, et al. (2022) Policy news and stock market volatility. NBER Working Paper series 25720. https://doi.org/10.3386/w25720 doi: 10.3386/w25720

|

| [3] |

Balduzzi P (1995) Stock Returns, Inflation, and the Proxy Hypothesis: A New Look at the data. Econ Lett 48: 47–53. https://doi.org/10.1016/0165-1765(94)00568-M doi: 10.1016/0165-1765(94)00568-M

|

| [4] |

Bali TG, Engle RF (2010) The intertemporal capital asset pricing model with dynamic conditional correlations. J Monet Econ 57: 377–390. https://doi.org/10.1016/j.jmoneco.2010.03.002 doi: 10.1016/j.jmoneco.2010.03.002

|

| [5] |

Batten JA, Kinateder H, Kinateder PG, et al. (2021) Hedging stocks with oil. Ener Econ 93: 104422 https://doi.org/10.1016/j.eneco.2019.06.007 doi: 10.1016/j.eneco.2019.06.007

|

| [6] |

Batten JA, Boubaker S, Kinateder H, et al. (2023) Volatility impacts on global banks: Insights from the GFC, COVID-19, and the Russia-Ukraine war. J Econ Behav Organ 215: 325–350 https://doi.org/10.1016/j.jebo.2023.09.016 doi: 10.1016/j.jebo.2023.09.016

|

| [7] |

Beladi H, Choudhary MAS, Parai AK (1993) Rational and adaptive expectations in the present value model of hyperinflation. Rev Econ Stat 75: 511–514. https://doi.org/10.2307/2109466 doi: 10.2307/2109466

|

| [8] |

Bessler DA, Yang J (2003) The structure of interdependence in international stock markets. J Int Money Financ 22: 261–287. https://doi.org/10.1016/S0261-5606(02)00076-1 doi: 10.1016/S0261-5606(02)00076-1

|

| [9] | Boudoukh J, Richarson M (1993) Stock Returns and Inflation: A Long-Horizon Perspective. Am Econ Rev 83: 1346–1355. |

| [10] |

Bouri E, Nekhili R, Kinateder H, et al. (2023) Expected inflation and U.S. stock sector indices: A dynamic time-scale tale from inflationary and deflationary crisis periods. Financ Res Let 55: 103845. https://doi.org/10.1016/j.frl.2023.103845 doi: 10.1016/j.frl.2023.103845

|

| [11] |

Caldara D, Iacoviello M (2022) Measuring geopolitical risk. Am Econ Rev 112, 1194–225. https://doi.org/10.1257/aer.20191823 doi: 10.1257/aer.20191823

|

| [12] | Chaudhary M, Marrow B (2022) Inflation Expectations and Stock Returns. http://dx.doi.org/10.2139/ssrn.4154564 |

| [13] | Cheema MA, Faff R, Szulczyk K (2020) The 2008 Global financial crisis and COVID-19 pandemic: How safe are the safe haven assets? Covid Econ 34: 88–115. |

| [14] |

Chen CYH, Chiang TC, Härdle WK (2018) Downside risk and stock returns in the G7 countries: An empirical analysis of their long-run and short-run dynamics. J Bank Financ 93: 21–32. https://doi.org/10.1016/j.jbankfin.2018.05.012 doi: 10.1016/j.jbankfin.2018.05.012

|

| [15] |

Chiang TC (2020) US policy uncertainty and stock returns: evidence in the US and its spillovers to European Union, China, and Japan. J Risk Financ 21: 621–657. https://doi.org/10.1108/JRF-10-2019-0190 doi: 10.1108/JRF-10-2019-0190

|

| [16] |

Chiang TC (2021) Geopolitical risk, economic policy uncertainty and asset returns in Chinese financial markets. China Financ Rev Int 11: 474–501. https://doi.org/10.1108/CFRI-08-2020-0115. doi: 10.1108/CFRI-08-2020-0115

|

| [17] |

Chiang TC (2022) Can gold or silver be used as a hedge against policy uncertainty and COVID-19 in the Chinese market? China Financ Rev Int 12: 571–600. https://doi.org/10.1108/CFRI-12-2021-0232 doi: 10.1108/CFRI-12-2021-0232

|

| [18] |

Chiang TC (2023) Real stock market returns and inflation: Evidence from uncertainty hypotheses. Financ Res Lett 53: 103606. https://doi.org/10.1016/j.frl.2022.103606. doi: 10.1016/j.frl.2022.103606

|

| [19] |

Chiang TC, Jeon BN, Li H (2007) Dynamic correlation analysis of financial contagion: Evidence from Asian markets. J Int Money Financ 26: 1206–1228. https://doi.org/10.1016/j.jimonfin.2007.06.005 doi: 10.1016/j.jimonfin.2007.06.005

|

| [20] |

Chiang TC, Tang Y (2023) Uncertainty and asset prices: evidence at times of COVID-19 and Beyond. China Financ Rev Int 13: 305–308. https://doi.org/10.1108/CFRI-08-2023-278 doi: 10.1108/CFRI-08-2023-278

|

| [21] |

Choudhry T (2001) Inflation and rates of return on stocks: Evidence from high inflation countries. J Int Financ Mark I 11: 75–96. https://doi.org/10.1016/S1042-4431(00)00037-8 doi: 10.1016/S1042-4431(00)00037-8

|

| [22] | Cieslak A, Pflueger C (2023) Inflation and asset returns. National Bureau of Economic Research Working Paper No. 30982. https://doi.org/10.3386/w30982 |

| [23] |

Cifter A (2015) Stock returns, inflation, and real activity in developing countries: A Markov-switching approach. Panoecon 62: 55–76. https://doi.org/10.2298/PAN1501055C doi: 10.2298/PAN1501055C

|

| [24] |

Davis N, Kutan AM (2003) Inflation and output as predictors of stock returns and volatility: International Evidence. Appl Financ Econ 13: 693–700. https://doi.org/10.1080/09603100210139429 doi: 10.1080/09603100210139429

|

| [25] |

Ding Z, Granger CWJ, Engle RF (1993) A long memory property of stock market returns and a new model. J Empir Financ 1: 83–106. https://doi.org/10.1016/0927-5398(93)90006-D doi: 10.1016/0927-5398(93)90006-D

|

| [26] |

Fama E, Schwert G (1977) Asset returns and inflation. J Financ Econ 5: 115–146. https://doi.org/10.1016/0304-405X(77)90014-9 doi: 10.1016/0304-405X(77)90014-9

|

| [27] | Fama EF (1981) Stock returns, real activity, inflation, and money. Am Econ Rev 71: 545–565. |

| [28] | Fisher I (1930) The theory of interest, New York: Mcmillan. |

| [29] |

Gallagher LA, Taylor MP (2002) The stock return–inflation puzzle revisited. Econ Lett 75: 147–156. https://doi.org/10.1016/S0165-1765(01)00613-9 doi: 10.1016/S0165-1765(01)00613-9

|

| [30] |

Geske R, Roll R (1983) The fiscal and monetary linkage between stock returns and inflation. J Financ 38: 1–31. https://doi.org/10.1111/j.1540-6261.1983.tb03623.x doi: 10.1111/j.1540-6261.1983.tb03623.x

|

| [31] |

Glosten L, Jagannathan R, Runkle D (1993) On the relation between the expected value and the volatility of the nominal excess return on stocks. J Financ 48: 1779–1801. https://doi.org/10.1111/j.1540-6261.1993.tb05128.x doi: 10.1111/j.1540-6261.1993.tb05128.x

|

| [32] |

Graham FC (1996) Inflation, real stock returns, and monetary policy. Appl Financ Econ 6: 29–35. https://doi.org/10.1080/096031096334448 doi: 10.1080/096031096334448

|

| [33] |

Gultekin NB (1983) Stock Market Returns and Inflation Forecasts. J Financ 38: 663–673. https://doi.org/10.1111/j.1540-6261.1983.tb02495.x doi: 10.1111/j.1540-6261.1983.tb02495.x

|

| [34] |

Hasan MS (2008) Stock returns, inflation and interest rates in the United Kingdom. Eur J Financ 14: 687–699. https://doi.org/10.1080/13518470802042211 doi: 10.1080/13518470802042211

|

| [35] |

Hoong TB, Ling TY, Hassan S, et al. (2023) Stock Returns and Inflation: a Bibliometric Analysis. Int J Prof Bus Rev 8: e01547–e01547. Available from: https://doi.org/10.26668/businessreview/2023.v8i2.1547 doi: 10.26668/businessreview/2023.v8i2.1547

|

| [36] |

James C, Koreisha S, Partch M (1985) A VARMA analysis of the causal relations among stock returns, real output, and nominal interest rates. J Financ 40: 1375–1384. https://doi.org/10.1111/j.1540-6261.1985.tb02389.x doi: 10.1111/j.1540-6261.1985.tb02389.x

|

| [37] |

Karolyi A (1995) A Multivariate GARCH Models of International Transmissions of Stock Returns and Volatility: The Case of the United States and Canada. J Bus Econ Stat 13: 11–25. https://doi.org/10.1080/07350015.1995.10524575 doi: 10.1080/07350015.1995.10524575

|

| [38] |

Kaul G (1987) Stock Returns and Inflation: The Role of the Monetary Sector. J Financ Econ 18: 253–276. https://doi.org/10.1016/0304-405X(87)90041-9 doi: 10.1016/0304-405X(87)90041-9

|

| [39] |

Kaul G (1990) Monetary Regimes and the Relation between Stock Returns and Inflationary Expectations. J Financ Quant Anal 25: 307–321. https://doi.org/10.2307/2330698 doi: 10.2307/2330698

|

| [40] | Kilian L, Zhou X (2021) The Impact of Rising Oil Prices on U.S. Inflation and Inflation Expectations in 2020–2023. Working Paper 2116. Federal reserve Bank of Dalla. Available from: https://www.dallasfed.org/-/media/documents/research/papers/2021/wp2116.pdf |

| [41] |

Kolluri B, Wahab M (2008) Stock returns and expected inflation: evidence from an asymmetric test specification. Rev Quant Financ Account 30: 371–395. https://doi.org/10.1007/s11156-007-0060-9 doi: 10.1007/s11156-007-0060-9

|

| [42] |

Koutmos G, Booth G (1995) Asymmetric Volatility Transmission in International Stock Markets. J Int Money Financ 14: 747–762. https://doi.org/10.1016/0261-5606(95)00031-3 doi: 10.1016/0261-5606(95)00031-3

|

| [43] |

Kryzanowski L, Rahman AH (2009) Generalized Fama proxy hypothesis: impact of shocks on Phillips curve and relation of stock returns with inflation. Econ Lett 103: 35–137. https://doi.org/10.1016/j.econlet.2009.03.001 doi: 10.1016/j.econlet.2009.03.001

|

| [44] | Kumari J (2011) Stock Returns and Inflation in India: An Empirical Analysis. IUP J Monetary Econ 9: 39–75. |

| [45] |

Li L, Narayan PK, Zheng X (2010) An analysis of inflation and stock returns for the UK. J Int Financ Mark Inst Money 20: 519–532. https://doi.org/10.1016/j.intfin.2010.07.002 doi: 10.1016/j.intfin.2010.07.002

|

| [46] |

Li Q, Yang J, Hsiao C, et al. (2005) The relationship between stock returns and volatility in international stock markets. J Empir Financ 12: 650–665. https://doi.org/10.1016/j.jempfin.2005.03.001 doi: 10.1016/j.jempfin.2005.03.001

|

| [47] |

Lin SC (2009) Inflation and real stock returns revisited. Econ Inquiry 47: 783–795. https://doi.org/10.1111/j.1465-7295.2008.00193.x doi: 10.1111/j.1465-7295.2008.00193.x

|

| [48] |

Liu YA, Hsueh LP, Clayton RJ (1993) A re-examination of the proxy hypothesis. J Financ Res 16: 261–268. https://doi.org/10.1111/j.1475-6803.1993.tb00145.x doi: 10.1111/j.1475-6803.1993.tb00145.x

|

| [49] |

Madadpour S, Asgari M (2019) The puzzling relationship between stocks return and inflation: a review article. Int Rev Econ 66: 115–145. https://doi.org/10.1007/s12232-019-00317-w doi: 10.1007/s12232-019-00317-w

|

| [50] | Majid MSA (2010) Stock Returns, Economic Activity and Inflationary Trends in Malaysia: Evidence from the Post-1997 Asian Financial Turmoil. IUP J Appl Financ 16: 59. |

| [51] |

Marshall DA (1992) Inflation and asset returns in a monetary economy. J Financ 47: 1315–1342. https://doi.org/10.1111/j.1540-6261.1992.tb04660.x doi: 10.1111/j.1540-6261.1992.tb04660.x

|

| [52] |

McCarthy J, Najand M, Seifert B (1990) Empirical tests of the proxy hypothesis. Financ Rev 25: 251–263. https://doi.org/10.1111/j.1540-6288.1990.tb00795.x doi: 10.1111/j.1540-6288.1990.tb00795.x

|

| [53] |

Modigliani F, Cohn RA (1979) Inflation, rational valuation and the market. Financ Anal J 35: 24–44. https://doi.org/10.2469/faj.v35.n2.24 doi: 10.2469/faj.v35.n2.24

|

| [54] |

Nelson C (1976) Inflation and rates of return on common stocks. J Financ 31: 471–483. https://doi.org/10.1111/j.1540-6261.1976.tb01900.x doi: 10.1111/j.1540-6261.1976.tb01900.x

|

| [55] |

Nelson D (1991) Conditional heteroskedasticity in asset returns: An original approach. Econometrica 59: 347–370. https://doi.org/10.2307/2938260 doi: 10.2307/2938260

|

| [56] |

Rapach DE, Strauss JK, Zhou G (2013) International stock return predictability: what is the role of the United States? J Financ 68: 1633–1662. https://doi.org/10.1111/jofi.12041 doi: 10.1111/jofi.12041

|

| [57] | Sarte PDG (1998) Fisher's equation and the inflation risk premium in a simple endowment economy. Econ Q Fed Reserve Bank Richmond, 53–72. Available from: https://www.richmondfed.org/publications/research/economic_quarterly/1998/fall/sarte |

| [58] | Saryal FS (2007) Does Inflation Have an Impact on Conditional Stock Market Volatility?: Evidence from Turkey and Canada. Int Res J Financ Econ 11: 123–133. |

| [59] |

Solnik B (1983) The relation between stock prices and inflationary expectations: The international evidence. J Financ 38: 35–48. https://doi.org/10.1111/j.1540-6261.1983.tb03624.x doi: 10.1111/j.1540-6261.1983.tb03624.x

|

| [60] |

Solnik B, Solnik V (1997) A multi-country test of the Fisher model for stock returns. J Int Financ Mark Inst Money 7: 289–301. https://doi.org/10.1016/S1042-4431(97)00024-3 doi: 10.1016/S1042-4431(97)00024-3

|

| [61] |

Spyrou S (2004) Are stocks a good hedge against inflation? Evidence from emerging markets. Appl Econ 36: 41–48. https://doi.org/10.1080/0003684042000177189 doi: 10.1080/0003684042000177189

|

| [62] | Terry S, Bloom N, Davis S, et al. (2020) COVID-induced economic uncertainty and its consequences. VoxEU Available at: COVID-induced economic uncertainty and its consequences/CEPR. |

| [63] |

Tiwari AK, Adewuyi AO, Awodumi OB, et al. (2022) Relationship between stock returns and inflation : New evidence from the US using wavelet and causality methods. Int J Financ Econ 27: 4515–4540. https://doi.org/10.1002/ijfe.2384 doi: 10.1002/ijfe.2384

|

| [64] | Toyoshima Y, Hamori S (2011) Panel cointegration analysis of the Fisher effect: Evidence from the US, the UK, and Japan. Econ Bulle 31: 2674–2682. |

| [65] |

Tripathi V, Kumar A (2015) Short Run causal relationship between inflation and stock returns - An empirical study of BRICS markets. Asian J Manage Appl Res 5: 1–13. https://doi.org/10.5296/ijafr.v4i2.6671 doi: 10.5296/ijafr.v4i2.6671

|

| [66] |

Tsay RS (1988) Outliers, level shifts, and variance changes in time series. J Forecast 7: 1–20. https://doi.org/10.1002/for.3980070102 doi: 10.1002/for.3980070102

|

| [67] |

Wang Y, Pan Z, Wu C (2018) Volatility spillover from the US to international stock markets: A heterogeneous volatility spillover GARCH model: Volatility spillover from the U.S. to international stock markets. J Forecast 37: 385–400. https://doi.org/10.1002/for.2509 doi: 10.1002/for.2509

|

| [68] |

Wong KF, Wu HJ (2003) Testing Fisher hypothesis in long horizons for G7 and eight Asian countries. Appl Econ Lett 10: 917–923. https://doi.org/10.1080/1350485032000158645 doi: 10.1080/1350485032000158645

|

| [69] |

Yang J, Guo H, Wang Z (2006) International transmission of inflation among G-7 countries: A data-determined VAR analysis. J Bank Financ 30: 2681–2700. https://doi.org/10.1016/j.jbankfin.2005.10.005 doi: 10.1016/j.jbankfin.2005.10.005

|

Figures(1) / Tables(14)

Thomas C. Chiang. Stock returns and inflation expectations: Evidence from 20 major countries[J]. Quantitative Finance and Economics, 2023, 7(4): 538-568. doi: 10.3934/QFE.2023027

DownLoad:

DownLoad: