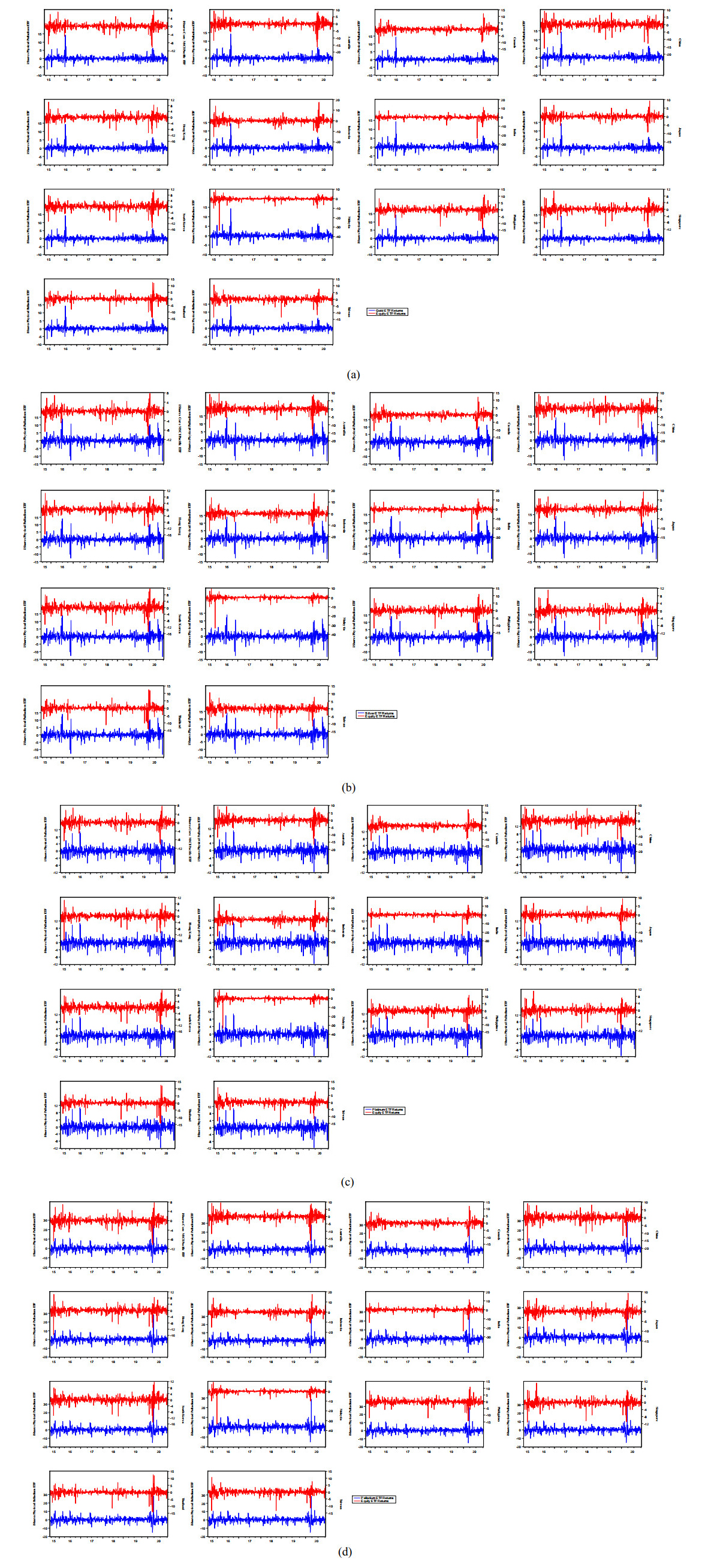

In this study, we exploit the information contained in financial innovations in precious metals for hedging the risks associated with the Asia-Pacific equities during the current pandemic. We measure financial innovations as exchange traded funds (ETFs) for gold, silver, platinum and palladium which contrast with investment in the physical precious metals since the former tracks well the prices of the latter and as well provides cost-effective alternative to invest in the markets without storage costs. Based on the optimal portfolio weights and optimal hedge ratios, we find that gold offers the best hedge (followed by silver, platinum, and palladium) against the risk associated with the Asia-Pacific equities during the COVID-19 pandemic albeit with a lower hedging effectiveness during the pandemic. Overall, including gold ETFs in an Asia-Pacific equity portfolio would provide both a valuable portfolio combination that could improve the risk-adjusted performance of the market in addition to serving as an effective hedge for equity-related risks.

Citation: Abdulsalam Abidemi Sikiru, Afees A. Salisu. Hedging with financial innovations in the Asia-Pacific markets during the COVID-19 pandemic: the role of precious metals[J]. Quantitative Finance and Economics, 2021, 5(2): 352-372. doi: 10.3934/QFE.2021016

In this study, we exploit the information contained in financial innovations in precious metals for hedging the risks associated with the Asia-Pacific equities during the current pandemic. We measure financial innovations as exchange traded funds (ETFs) for gold, silver, platinum and palladium which contrast with investment in the physical precious metals since the former tracks well the prices of the latter and as well provides cost-effective alternative to invest in the markets without storage costs. Based on the optimal portfolio weights and optimal hedge ratios, we find that gold offers the best hedge (followed by silver, platinum, and palladium) against the risk associated with the Asia-Pacific equities during the COVID-19 pandemic albeit with a lower hedging effectiveness during the pandemic. Overall, including gold ETFs in an Asia-Pacific equity portfolio would provide both a valuable portfolio combination that could improve the risk-adjusted performance of the market in addition to serving as an effective hedge for equity-related risks.

| [1] |

Ahmed AD, Huo R (2019) Impacts of China's crash on Asia-Pacific financial integration: volatility interdependence, information transmission and market co-movement. Econ Model 79: 28-46. doi: 10.1016/j.econmod.2018.09.029

|

| [2] |

Al-Maadid A, Caporale GM, Spagnolo F, et al. (2016) Spillovers between food and energy prices and structural breaks. Int Econ 150: 1-18. doi: 10.1016/j.inteco.2016.06.005

|

| [3] |

Arouri MEH, Nguyen DK (2010) Oil prices, stock markets and portfolio investment: evidence from sector analysis in Europe over the last decade. Energ Policy 38: 4528-4539. doi: 10.1016/j.enpol.2010.04.007

|

| [4] |

Arouri MEH, Jouini J, Nguyen DK (2011) Volatility spillovers between oil prices and stock sector returns: implications for portfolio management. J Int Money Financ 30: 1387-1405. doi: 10.1016/j.jimonfin.2011.07.008

|

| [5] | Arunanondchai P, Sukcharoen K, Leatham DJ (2019) Dealing with tail risk in energy commodity markets: futures contracts versus exchange-traded funds. J Commodity Mark 20: 100112. |

| [6] | Baker SR, Bloom N, Davis SJ, et al. (2020) Covid-induced economic uncertainty. NBER Working Paper No. 26983. |

| [7] | Balcilar M, Cerci G, Demirer R (2016) Is there a role for Islamic bonds in global diversification strategies? Manage Financ 42: 656-679. |

| [8] | Baur DG, Lucey BM (2010) Is gold a hedge or a safe haven? Anal Stock Bond Gold Financ Rev 45: 217-229. |

| [9] |

Beckmann J, Berger T, Czudaj R (2018) Gold price dynamics and the role of uncertainty. Quant Financ 19: 663-681. doi: 10.1080/14697688.2018.1508879

|

| [10] | Charupat N, Miu P (2013) Recent developments in exchange-traded fund literature: pricing efficiency, tracking ability: and effects on underlying securities. Manag Financ 39: 427-443. |

| [11] |

Chelley-Steeley P, Park K (2011) Intraday patterns in London listed exchange traded funds. Int Rev Financ Anal 20: 244-251. doi: 10.1016/j.irfa.2011.05.001

|

| [12] | Cheng C, Chen C, Lai H (2018) Revisiting the roles of gold: Does gold ETF matter? N Am J Econ Financ, 100891. |

| [13] |

Chow HK (2017) Volatility spillovers and linkages in Asian stock markets. Emerg Mark Financ Trade 53: 2770-2781. doi: 10.1080/1540496X.2017.1314960

|

| [14] | Conlon T, McGee R (2020) Safe haven or risky hazard? Bitcoing during the COVID-19 bear market. Financ Res Lett 35: 101607. |

| [15] | Corbet S, Larkin C, Lucey B (2020) The contagion effects of the COVID-19 pandemic: evidence from gold and cryptocurrencies. Financ Res Lett 35: 101554. |

| [16] | Dannhauser CD (2017) The impact of innovation: Evidence from corporate bond exchange-traded funds (ETFs). J Financ Econ, 537-560. |

| [17] | Devpura N, Narayan PK (2020) Hourly oil price volatility: the role of COVID-19. Energy Res Lett 1: 13683. |

| [18] | Ferri R (2009) The ETF Book: All You Need to Know About Exchange-Traded Funds, Eds., Hoboken, NJ: Wiley. |

| [19] | Gao S (2001) ETFs "The new generation of investment funds". ETFs Indexing 1: 101-105. |

| [20] |

Harper TJ, Madura J, Schnusenberg O (2006) Performance comparison between exchange-traded funds and closed-end country funds. Int Financ Mark I Money, 104-122. doi: 10.1016/j.intfin.2004.12.006

|

| [21] | Haslem JA (2003) Mutual funds: Risk and Performance Analysis for Decision Making, Eds., Oxford: Blackwell Publishing. |

| [22] | Hehn E (2005) Introduction, In: Hehn, Exchange Traded Funds: Structure, Regulation and Application of a New Fund Class, Eds., Heidelberg: Springer Berlin, 1-6. |

| [23] |

Hengchao Z, Hamid Z (2015) The impact of subprime crisis on Asia-Pacific Islamic stock markets. J Asia-Pac Bus 16: 105-127. doi: 10.1080/10599231.2015.1028304

|

| [24] | Huynh DL (2020) The effect of uncertainty on the precious metals market: new insights from transfer entropy and neural network VAR. Resour Policy 66: 101623. |

| [25] | Iyke B (2020a) COVID-19 The reaction of US oil and gas producers to the pandemic. Energy Res Lett 1: 13912. |

| [26] |

Iyke BN (2020b) The disease outbreak channel of exchange rate return predictability: evidence from COVID-19. Emerg Mark Financ Trade 56: 2277-2297. doi: 10.1080/1540496X.2020.1784718

|

| [27] | Jin J, Yu J, Hu Y, et al. (2019) Which one is more informative in determining price movements of hedging assets? Evidence from Bitcoin, gold and crude oil markets. Phys A 527: 121121. |

| [28] |

Junttila J, Pesonen J, Raatikainen J (2018) Commodity market based hedging against stock market risk in times of financial crisis: the case of crude oil and gold. J Int Finan Mark I Money, 255-280. doi: 10.1016/j.intfin.2018.01.002

|

| [29] |

Kaur P, Singh J (2020) Price formation in Indian gold market: analyzing the role of gold exchange traded funds (ETFs) against spot and futures market. IIMB Manage Rev, 59-74. doi: 10.1016/j.iimb.2019.07.017

|

| [30] |

Kim S (2005) Information leadership in the advanced Asia-Pacific stock markets: return, volatility and volume information spillovers from the US and Japan. J JPN Int Econ 19: 338-365. doi: 10.1016/j.jjie.2004.03.002

|

| [31] | Kraft B (2012) Getting an edge with exchange‐traded funds, In: Trade Your Way to Wealth. |

| [32] |

Kroner KF, Ng VK (1998) Modeling asymmetric comovements of asset returns. Rev Financ Stud 11: 817-844. doi: 10.1093/rfs/11.4.817

|

| [33] |

Kumar D (2014) Return and volatility transmission between gold and stock sectors: application of portfolio management and hedging effectiveness. IIMB Manage Rev 26: 5-16. doi: 10.1016/j.iimb.2013.12.002

|

| [34] |

Latunde T, Akinola LS, Dare DD (2020). Analysis of capital asset pricing model on Deutsche bank energy commodity. Green Financ 2: 20-34. doi: 10.3934/GF.2020002

|

| [35] |

Lau MCK, Vigne SA, Wang S, et al. (2017) Return spillovers between white precious metal ETFs: the role of oil, gold, and global equity. Int Rev Financ Anal 52: 316-332. doi: 10.1016/j.irfa.2017.04.001

|

| [36] |

Lechman E, Marszk A (2015) ICT technologies and financial innovations: The case of exchange traded funds in Brazil, Japan, Mexico, South Korea and the United States. Technol Forecast Soc Change 99: 355-376. doi: 10.1016/j.techfore.2015.01.006

|

| [37] | Lee M, Chiou JS, Wu PS, et al. (2005) Hedging with S & P500 and E-mini S & P500 stock index futures. J Stat Manage Syst 8: 275-294. |

| [38] |

Leung T, Ward B (2015) The golden target: analyzing the tracking performance of leveraged gold ETFs. Stud Econ Financ 32: 278-297. doi: 10.1108/SEF-01-2015-0009

|

| [39] | Li Y, Liang C, Ma F, et al. (2020) The role of the IDEMV in predicting European stock market volatility during the COVID-19 pandemic. Financ Res Lett 36: 101749. |

| [40] |

Lin C (2015) Asia-Pacific stock return predictability and market information flows. Emerg Mark Financ Trade 51: 658-671. doi: 10.1080/1540496X.2015.1046336

|

| [41] | Ling S, McAleer M (2003) Asymptotic theory for a vector ARMA-GARCH model. Econ Theory 19: 280-310. |

| [42] | Liu L (2014) Extreme downside risk spillover from the United States and Japan to Asia-Pacific stock markets. Int Rev Financ Anal 33: 39-48. |

| [43] |

Lypny G, Powalla M (1998) The hedging effectiveness of DAX futures. Eur J Financ 4: 345-355. doi: 10.1080/135184798337227

|

| [44] |

Maghyereh A, Awartani B, Hassan A (2018) Can gold be used as a hedge against the risks of Sharia-compliant securities? Application for Islamic portfolio management. J Asset Manage 19: 394-412. doi: 10.1057/s41260-018-0090-y

|

| [45] |

Marszk A, Lechman E (2018) Tracing financial innovation diffusion and substitution trajectories. Recent evidence on exchange-traded funds in Japan and South Korea. Technol Forecast Soc Change 133: 51-71. doi: 10.1016/j.techfore.2018.03.003

|

| [46] | Naeem M, Umar Z, Ahmed S, et al. (2020) Dynamic dependence between ETFs and crude oil prices by using EGARCH-Copula approach. Phys A 557: 124885. |

| [47] | Narayan PK (2020a) Oil price news and COVID-19-Is there any connection? Energy Res Lett 1: 13176. |

| [48] | Narayan PK (2020b) Did bubble activity intensify during COVID-19? Asian Econ Lett 1. |

| [49] | Narayan PK (2020c) Has COVID-19 changed exchange rate resistance to shocks? Asian Econ Lett 1. |

| [50] | Narayan PK, Devpura N, Wang H (2020) Japanese currency and stock market-What happened during the COVID-19 pandemic? Econ Anal Policy 68: 191-198. |

| [51] | OECD (2020) Coronavirus: The world economy at risk. OECD Interim Economic Assessment. Available from: https://www.oecd.org/berlin/publikationen/Interim-Economic-Assessment-2-March-2020.pdf. |

| [52] | Okorie DI, Lin B (2020) Crude oil price and cryptocurrencies: evidence of volatility connectedness and hedging strategy. Energy Econ 87: 104703. |

| [53] | Olson E, Vivian A, Wohar ME (2019) What is a better cross-hedge for energy: equities or other commodities? Glob Financ J 42: 100417. |

| [54] |

Ozdurak C, Ulusoy V (2020) Price discovery in crude oil markets: Intraday volatility interactions between crude oil futures and energy exchange traded funds. Int J Energy Econ Policy 10: 402-413. doi: 10.32479/ijeep.9014

|

| [55] | Qin M, Zhang YC, Su CW (2020) The essential role of pandemics: A fresh insight into the oil market. Energy Res Lett 1. |

| [56] |

Reboredo JC, Naifar N (2017) Do Islamic bond (sukuk) prices reflect financial and policy uncertainty? A quantile regression approach. Emerg Mark Financ Trade 53: 1535-1546. doi: 10.1080/1540496X.2016.1256197

|

| [57] |

Sakarya B, Ekinci A (2020) Exchange-traded funds and FX volatility: Evidence from Turkey. Cent Bank Rev 20: 205-211. doi: 10.1016/j.cbrev.2020.06.002

|

| [58] | Salisu AA, Obiora K (2021) COVID-19 pandemic and the crude oil market risk: hedging options with non-energy financial innovations. Financ Innov 7: 34. |

| [59] | Salisu AA, Ogbonna AE (2021) The return volatility of cryptocurrencies during the COVID-19 pandemic: assessing the news effect. Glob Financ J [In press]. |

| [60] | Salisu AA, Vo XV, Lucey B (2021) Gold and US sectoral stocks during COVID-19 pandemic. Res Int Bus Financ 57: 101424. |

| [61] |

Salisu AA, Akanni LO (2020) Constructing a global fear index for the COVID-19 Pandemic. Emerg Mark Financ Trade 56: 2310-2331. doi: 10.1080/1540496X.2020.1785424

|

| [62] | Salisu AA, Vo XV (2020) Predicting stock returns in the presence of COVID-19: the role of health news. Int Rev Financ Anal 71: 101546. |

| [63] |

Salisu, AA, Mobolaji H (2013) Modeling returns and volatility transmission between oil price and US-Nigeria exchange rate. Energy Econ 39: 169-176. doi: 10.1016/j.eneco.2013.05.003

|

| [64] |

Salisu AA, Ebuh GU, Usman N (2020) Revisiting oil-stock nexus during COVID-19 pandemic: some preliminary results. Int Rev Econ Financ 69: 280-294. doi: 10.1016/j.iref.2020.06.023

|

| [65] | Salisu A, Adediran I (2020) Uncertainty due to infectious diseases and energy market volatility. Energy Res Lett 1. |

| [66] |

Salisu AA, Ndako UB, Oloko TF (2019) Assessing the inflation hedging of gold and palladium in OECD countries. Res Policy 62: 357-377. doi: 10.1016/j.resourpol.2019.05.001

|

| [67] |

Salisu AA, Oloko TF (2015) Modeling oil price-US stock nexus: a VARMA-BEKK-AGARCH approach. Energy Econ 50: 1-12. doi: 10.1016/j.eneco.2015.03.031

|

| [68] | Salisu AA, Vo XV, Lawal A (2020) Hedging oil price risk with gold during COVID-19 pandemic. Res Policy 70: 101897. |

| [69] | Salisu AA, Sikiru AA (2020) Pandemics and the Asia-Pacific Islamic stocks. Asian Econ Lett 1. |

| [70] | Sikiru AA, Salisu AA (2021) Hedging against risks associated with travel and tourism stocks during COVID‐19 pandemic: the role of gold. Int J Financ Econ [In press]. |

| [71] |

Selmi R, Mensi W, Hammoudeh S, et al. (2018) Is bitcoin a hedge, a safe haven or a diversifier for oil price movements? A comparison with gold. Energy Econ 74: 787-801. doi: 10.1016/j.eneco.2018.07.007

|

| [72] |

Shahzad SJH, Aloui C, Jammazi R, et al. (2019) Are Islamic bonds a good safe haven for stocks? Implications for portfolio management in a time-varying regime-switching copula framework. Appl Econ 51: 219-238. doi: 10.1080/00036846.2018.1494376

|

| [73] | Sharma SS (2020) A Note on the Asian market volatility during the COVID-19 pandemic. Asian Econ Lett 1. |

| [74] | Shrydeh N, Shahateet M, Mohammad S, et al. (2019) The hedging effectiveness of gold against US stocks in a post-financial crisis era. Cogent Econ Financ 7. |

| [75] |

Sukcharoen K, Choi H, Leatham DJ (2015) Optimal gasoline hedging strategies using futures contracts and exchange-traded-funds. Appl Econ 47: 3482-3498. doi: 10.1080/00036846.2015.1016210

|

| [76] | Tari MJ (2010) Exchange‐traded funds (ETFs). Encyclopedia Quant Financ. |

| [77] |

Urom C, Abid I, Guesmi K, et al. (2020) Quantile spillovers and dependence between bitcoin, equities and strategic commodities. Econ Model 93: 230-258. doi: 10.1016/j.econmod.2020.07.012

|

| [78] |

Yang MJ, Lai YC (2009) An out-of-sample comparative analysis of hedging performance of stock index futures: dynamic versus static hedging. Appl Financ Econ 19: 1059-1072. doi: 10.1080/09603100802112284

|

Figures(1) / Tables(5)

Abdulsalam Abidemi Sikiru, Afees A. Salisu. Hedging with financial innovations in the Asia-Pacific markets during the COVID-19 pandemic: the role of precious metals[J]. Quantitative Finance and Economics, 2021, 5(2): 352-372. doi: 10.3934/QFE.2021016

DownLoad:

DownLoad: