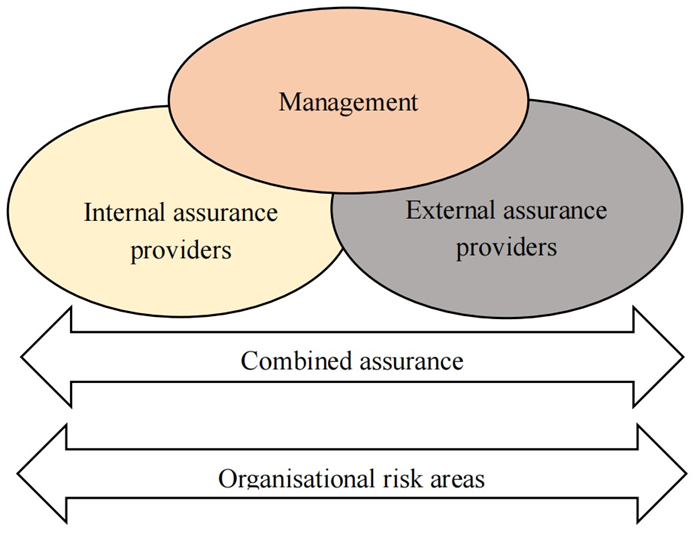

In addition to integrated reporting, which was arguably first introduced by the third King Report on Governance for South Africa (King Ⅲ), King Ⅲ also formally introduced the combined assurance model as a further governance innovation, aimed at enhancing the quality of organisational reporting. Although the combined assurance model is primarily an internal enterprise risk management innovation, designed to incorporate, integrate and optimise all assurance services and functions, it simultaneously enhances the credibility of organisational reporting. Taken as a whole, the combined assurance model enables an effective control environment, supports the integrity of information used for internal decision-making by management, the governing body and its committees; while supporting the integrity of the organisation's external reports. Organisations adopting King Ⅳ, including state-owned enterprises (SOEs), are expected to explain how the provisions of the combined assurance model have been implemented. Explaining conformance, introduces an element of innovation into organisational reporting as envisaged by King Ⅳ, by providing stakeholders with assurance about the veracity of the disclosures contained in the internal and external reports of organisations. This exploratory paper analyses the extent to which South African SOEs have conformed to seven key combined assurance indicators. The disclosures contained in the publicly available annual/integrated reports of South African SOEs, listed in Schedule 2 of the Public Finance Management Act (PFMA), were thematically analysed to fulfil the objective of the study. We found that although the combined assurance related disclosures suggest high levels of adoption by some SOEs, the majority have not provided sufficient information to explain how they have applied combined assurance, if at all. Although their reports appear to provide internal management with some level of assurance about the extent to which risks have been managed, these reports may not necessarily provide external users with confidence that all material risks have been effectively mitigated, within the organisation's risk appetite. This paper discuses implications for policy and practice and concludes by providing avenues for further research.

Citation: Adeyemi Adebayo, Barry Ackers. Adoption of the combined assurance model by South African state-owned enterprises (SOEs)[J]. National Accounting Review, 2023, 5(1): 41-66. doi: 10.3934/NAR.2023004

In addition to integrated reporting, which was arguably first introduced by the third King Report on Governance for South Africa (King Ⅲ), King Ⅲ also formally introduced the combined assurance model as a further governance innovation, aimed at enhancing the quality of organisational reporting. Although the combined assurance model is primarily an internal enterprise risk management innovation, designed to incorporate, integrate and optimise all assurance services and functions, it simultaneously enhances the credibility of organisational reporting. Taken as a whole, the combined assurance model enables an effective control environment, supports the integrity of information used for internal decision-making by management, the governing body and its committees; while supporting the integrity of the organisation's external reports. Organisations adopting King Ⅳ, including state-owned enterprises (SOEs), are expected to explain how the provisions of the combined assurance model have been implemented. Explaining conformance, introduces an element of innovation into organisational reporting as envisaged by King Ⅳ, by providing stakeholders with assurance about the veracity of the disclosures contained in the internal and external reports of organisations. This exploratory paper analyses the extent to which South African SOEs have conformed to seven key combined assurance indicators. The disclosures contained in the publicly available annual/integrated reports of South African SOEs, listed in Schedule 2 of the Public Finance Management Act (PFMA), were thematically analysed to fulfil the objective of the study. We found that although the combined assurance related disclosures suggest high levels of adoption by some SOEs, the majority have not provided sufficient information to explain how they have applied combined assurance, if at all. Although their reports appear to provide internal management with some level of assurance about the extent to which risks have been managed, these reports may not necessarily provide external users with confidence that all material risks have been effectively mitigated, within the organisation's risk appetite. This paper discuses implications for policy and practice and concludes by providing avenues for further research.

| [1] |

Abhishek N, Divyashree MS (2019) Integrated reporting practices in Indian companies. FOCUS: J Int Bus 6: 140–151. https://doi.org/10.17492/focus.v6i1.182825 doi: 10.17492/focus.v6i1.182825

|

| [2] |

Ackers B, Adebayo A (2022) The adoption of integrated reporting by state-owned enterprises (SOEs)—an international comparison. Soc Responsib J 18: 1687–1612. https://doi.org/10.1108/SRJ-05-2021-0194 doi: 10.1108/SRJ-05-2021-0194

|

| [3] |

Ackers B (2017) The evolution of corporate social responsibility assurance—A longitudinal study. Soc Environ Account J 37: 97–117. https://doi.org/10.1080/0969160X.2017.1294097 doi: 10.1080/0969160X.2017.1294097

|

| [4] |

Almquist R, Grossi G, van Helden J, et al. (2013) Public sector governance and accountability. Crit Perspect Account 24: 479–487. https://doi.org/10.1016/j.cpa.2012.11.005 doi: 10.1016/j.cpa.2012.11.005

|

| [5] |

Ampri ANI, Adhariani D (2019) Application of combined assurance as a new approach to integrate internal audit, governance, and risk management: A case study on Indonesia financial service authority. Advances in Economics, Business and Management Research 101: 29–33. https://doi.org/10.2991/iconies-18.2019.5 doi: 10.2991/iconies-18.2019.5

|

| [6] |

Atkins JF, Solomon A, Norton S, et al. (2015) The emergence of integrated private reporting. Meditari Account Res 23: 28–61. https://doi.org/10.1108/MEDAR-01-2014-0002 doi: 10.1108/MEDAR-01-2014-0002

|

| [7] | BDO (2017) Combined assurance in an uncertain world. Available from: https://www.bdo.co.za/en-za/insights/2017/audit/combined-assurance-in-an-uncertain-world. |

| [8] |

Botes V, Sharma U, Botes R, et al (2020) A structured approach to the governance of ethics using the five lines of assurance model. Int J Econ Account 9: 336–352. https://doi.org/10.1504/IJEA.2020.110166 doi: 10.1504/IJEA.2020.110166

|

| [9] |

Bovens M (2010) Two concepts of accountability: Accountability as a virtue and as a Mechanism. West Eur Polit 33: 946–967. https://doi.org/10.1080/01402382.2010.486119 doi: 10.1080/01402382.2010.486119

|

| [10] | Bovens M, Schillemans T, Goodin RE (2014) Public accountability, In: Bovens, M., Goodin, R.E., Schillemans, T. (Eds), The Oxford Handbook of Public Accountability, Oxford: Oxford University Press, 1–20. |

| [11] | CGF Research Institute (2019) Combined assurance: Is your organisation adequately assured? Available from: https://www.cgfresearch.co.za/News-Articles/Articles-Editorials/ArticleId/312/combined-assurance-is-your-organisation-adequately-assured-2019-10-01. |

| [12] |

Chariri A (2019) The patterns of integrated reporting: A comparative study of companies listed on the Johannesburg stock exchanges and Indonesia stock exchanges. Jurnal Reviu Akuntansi dan Keuangan 9: 1–12. https://doi.org/10.22219/jrak.v9i1.8248 doi: 10.22219/jrak.v9i1.8248

|

| [13] | Chikwiri TM, de la Rosa SP (2015) Internal audit's role in embedding governance, risk, and compliance in state-owned companies. So Afr J Account Aud Res 17: 25–39. |

| [14] | Coetzee P, Lubbe D (2011) Internal audit and risk management in South Africa: Adherence to guidance. Acta Acad 43: 29–60. |

| [15] | Daily Maverick (2019) SAA and SA Express fail to land 2018/19 annual report in Parliament. Available from: https://www.dailymaverick.co.za/article/2019-10-02-saa-and-sa-express-fail-to-land-2018-19-annual-report-in-parliament/. |

| [16] | Daly J, Kellehear A, Gliksman M (1997) The public health researcher: A Methodological approach, Oxford University Press, Melbourne. |

| [17] |

De Villiers C, Venter ER, Hsiao PCK (2017) Integrated reporting: background, measurement issues, approaches and an agenda for future research. Account Finance 57: 937–959. https://doi.org/10.1111/acfi.12246 doi: 10.1111/acfi.12246

|

| [18] |

Decaux L, Sarens G (2015) Implementing combined assurance: insights from multiple case studies. Manag Audit J 30: 56–79. https://doi.org/10.1108/MAJ-08-2014-1074 doi: 10.1108/MAJ-08-2014-1074

|

| [19] | Deloitte (2016) King Ⅳ bolder than ever. Available from: https://www2.deloitte.com/za/en/pages/africa-centre-for-corporate-governance/articles/kingiv-report-on-corporate-governance.html. |

| [20] | Devaney L (2016) Good governance? Perceptions of accountability, transparency and effectiveness in Irish food risk governance. Food Policy 62: 1–10. https://doi.org/1016/j.foodpol.2016.04.003. |

| [21] |

Donkor A, Djajadikerta HG, Roni SM (2021) Impacts of combined assurance on integrated, sustainability and financial reporting qualities: Evidence from listed companies in South Africa. Int J Audit 25: 475–507. https://doi.org/10.1111/ijau.12229 doi: 10.1111/ijau.12229

|

| [22] | Ebrahim A, Battilana J, Mair J (2014) The governance of social enterprises: Mission drift and accountability challenges in hybrid organizations. Res Organ Behav 34: 81–100. https://doi.org/1016/j.riob.2014.09.001. |

| [23] | Eccles RG, Krzus MP, Solano C (2019) A Comparative analysis of integrated reporting in ten countries. Available from: http://dx.doi.org/10.2139/ssrn.3345590. |

| [24] | Engelbrecht L, Deegan B (2010) King Ⅲ and "combined assurance", In: Accounting and Auditing. |

| [25] | Forte J, Barac K (2015) Combined assurance: A systematic process. So Afr J Account Aud Res 17: 71–83. |

| [26] |

Gerged AM, Cowton CJ, Beddewela ES (2018) Towards sustainable development in the Arab middle east and north Africa region: A longitudinal analysis of environmental disclosure in corporate annual reports. Bus Strategy Environ 27: 572–587. https://doi.org/10.1002/bse.2021 doi: 10.1002/bse.2021

|

| [27] |

Ghani EK, Jamal J, Puspitasari E, et al. (2018) Factors influencing integrated reporting practices among Malaysian public listed real property companies: A sustainable development effort. Int J Manag Financ Account 10: 144–162. https://doi.org/10.1504/IJMFA.2018.091662 doi: 10.1504/IJMFA.2018.091662

|

| [28] | Guest G, MacQueen K, Namey E (2012) Applied thematic analysis, Sage Publications Inc, Thousand Oaks, CA. |

| [29] |

Hoang H, Phang SY (2020) How does combined assurance affect the reliability of integrated reports and investors' judgments? Eur Account Rev 30: 175–195. https://doi.org/10.1080/09638180.2020.1745659 doi: 10.1080/09638180.2020.1745659

|

| [30] |

Hussain N, Rigoni U, Orij RP (2018) Corporate Governance and Sustainability Performance: Analysis of Triple Bottom Line Performance. J Bus Ethics 149: 411–432. https://doi.org/10.1007/s10551-016-3099-5 doi: 10.1007/s10551-016-3099-5

|

| [31] | Institute of Directors in Southern Africa (IoDSA) (2009) King Report on Governance for South Africa 2009 (King Ⅲ). Available from: https://cdn.ymaws.com/www.iodsa.co.za/resource/resmgr/king_iii/King_Report_on_Governance_fo.pdf. |

| [32] | Institute of Directors in Southern Africa (IoDSA) (2016) King Report on Corporate Governance for South Africa 2016 (King Ⅳ). Available from: https://cdn.ymaws.com/www.iodsa.co.za/resource/collection/684B68A7-B768-465C-8214-E3A007F15A5A/IoDSA_King_IV_Report_-_WebVersion.pdf. |

| [33] |

Keasey K, Wright M (1993) lssues in corporate accountability and governance: An editorial. Account Bus Res 23: 291–303. https://doi.org/10.1080/00014788.1993.9729897 doi: 10.1080/00014788.1993.9729897

|

| [34] | Kılıç M, Kuzey C (2018) Factors influencing sustainability reporting: Evidence from Turkey Available from: http://dx.doi.org/10.2139/ssrn.3098812. |

| [35] |

Klijn E (2008) Complexity Theory and Public Administration: What's New? Key concepts in complexity theory compared to their counterparts in public administration research. Public Manag Rev 10: 299–317. https://doi.org/10.1080/14719030802263954. doi: 10.1080/14719030802263954

|

| [36] | KPMG (2021) Integrated assurance. Available from: https://home.kpmg/za/en/home/services/advisory/risk-consulting/internal-audit-risk/internal-audit-strategic-sourcing/integrated-assurance.html. |

| [37] |

Liu Z, Jubb C, Abhayawansa S (2019) Analysing and evaluating integrated reporting: Insights from applying a normative benchmark. J Intellect Cap 20: 235–263. https://doi.org/10.1108/JIC-02-2018-0031 doi: 10.1108/JIC-02-2018-0031

|

| [38] |

Mackieson P, Shlonsky A, Conolly M (2018) Increasing rigor and reducing bias in qualitative research: A document analysis of parliamentary debates using applied thematic analysis. Qual Soc Work 18: 1–16. https://doi.org/10.1177/1473325018786996 doi: 10.1177/1473325018786996

|

| [39] |

Mansi M, Pandey R, Ghauri E (2017) CSR focus in the mission and vision statements of public sector enterprises: evidence from India. Manag Audit J 32: 356–377. https://doi.org/10.1108/MAJ-01-2016-1307 doi: 10.1108/MAJ-01-2016-1307

|

| [40] |

Maroun W (2019) Exploring the rationale for integrated report assurance. Account Audit Account J 32: 1826–1854. https://doi.org/10.1108/AAAJ-04-2018-3463 doi: 10.1108/AAAJ-04-2018-3463

|

| [41] |

Maroun W, Prinsloo A (2020) Drivers of combined assurance in a sustainable development context: Evidence from integrated reports. Bus Strategy Environ 29: 3702–3719. https://doi.org/10.1002/bse.2606 doi: 10.1002/bse.2606

|

| [42] | Miles M, Huberman A (1994) Qualitative data analysis, Sage Publications, London. |

| [43] | Millichamp A, Taylor J (2018) Auditing (11th ed.), Cengage Learning EMEA. |

| [44] |

Nakib M, Dey PK (2018) The journey towards integrated reporting in Bangladesh. Asian Econ Financ Rev 8: 894–913. https://doi.org/10.18488/journal.aefr.2018.87.894.913 doi: 10.18488/journal.aefr.2018.87.894.913

|

| [45] | Nkonki (2016) Integrated Reporting: A continued journey for public sector entities in South Africa. Available from: http://integratedreportingsa.org/ircsa/wp-content/uploads/2017/05/Nkonki-Public-Sector.pdf. |

| [46] |

Nzewi O, Musokeru P (2014) A Critical Review of the Oversight Role of the Office of the Auditor-General in Financial Accountability. Africa's Public Serv Deliv Perform Rev 2: 36–55. https://doi.org/10.4102/apsdpr.v2i1.42 doi: 10.4102/apsdpr.v2i1.42

|

| [47] | Okhmatovskiy I, Grosman A, Sun P (2021) Hybrid governance of state-owned enterprises, Oxford Handbook of State Capitalism and the Firm. |

| [48] |

Pirson M, Turnbull S (2011) Corporate governance, risk management, and the financial crisis: an information processing view. Corp Gov: An Int Rev 19: 459–470. https://doi.org/10.1111/j.1467-8683.2011.00860.x doi: 10.1111/j.1467-8683.2011.00860.x

|

| [49] |

Pistoni A, Songini L, Bavagnoli F (2018) Integrated reporting quality: An empirical analysis. Corp Soc Responsib Environ Manag 25: 489–507. https://doi.org/10.1002/csr.1474 doi: 10.1002/csr.1474

|

| [50] |

Prinsloo A, Maroun W (2020) An exploratory study on the components and quality of combined assurance in an integrated or a sustainability reporting setting. Sustain Account Manag Policy J 12: 1–29. https://doi.org/10.1108/SAMPJ-05-2019-0205. doi: 10.1108/SAMPJ-05-2019-0205

|

| [51] | PWC (2021) Annual global CEO survey. Available from: https://www.pwc.com/cl/es/publicaciones/pwc-24th-global-ceo-survey.pdf. |

| [52] | PWC (2019) Combined assurance (including governance). Available from: http://www.gardenroute.gov.za/wp-content/uploads/2019/06/PWC-Combined-Assurance.pdf. |

| [53] | PWC (2009) King's counsel: Understanding and unlocking the benefits of sound corporate governance. Available from: https://www.pwc.co.za/en/assets/pdf/executive-guide-to-kingiii.pdf. |

| [54] |

Rivera-Arrubla YA, Zorio-Grima A, García-Benau MA (2017) Integrated reports: Disclosure level and explanatory factors. Soc Responsib J 13: 155–176. https://doi.org/10.1108/SRJ-02-2016-0033 doi: 10.1108/SRJ-02-2016-0033

|

| [55] |

Ruiz-Lozano M, Tirado-Valencia P (2016) Do industrial companies respond to the guiding principles of the Integrated Reporting framework? A preliminary study on the first companies joined to the initiative. Revista de Contabilidad-Spanish Account Rev 19: 252–260. https://doi.org/10.1016/j.rcsar.2016.02.001 11. doi: 10.1016/j.rcsar.2016.02.00111

|

| [56] | Sarens G, Decaux L, Lenz R (2012) Combined assurance: Case studies on a holistic approach to organisational governance. Altamonte Springs, Florida, USA: The Institute of Internal Auditors Research Foundation. |

| [57] | Shortreed J, Fraser J, Purdy G, et al. (2012) The future role of internal audit in (enterprise) risk management, a white paper published on the website of the Manhattanville College. Available from: www.broadleaf.co.nz/pdfs/articles/Future_Role_of_IA_in_ERM.pdf. |

| [58] |

Sierra-García L, Zorio-Grima A, García-Benau MA (2015) Stakeholder engagement, corporate social responsibility and integrated reporting: An exploratory study. Corp Soc Responsib Environ Manag 22: 286–304. https://doi.org/10.1002/csr.1345. doi: 10.1002/csr.1345

|

| [59] | Simnett R, Zhou S, Hoang H (2016) Assurance and Other Credibility Enhancing Mechanisms for Integrated Reporting, In: Mio, C. (eds), Integrated Reporting, London: Palgrave Macmillan, 269–286. |

| [60] |

Smith J, Noble H (2014) Bias in research. Evid Based Nurs 17: 100–101. https://doi.org/10.1136/eb-2014-101946 doi: 10.1136/eb-2014-101946

|

| [61] | South Africa (1999) Public Finance Management Act, no. 1 of 1999. Available from: www.treasury.gov.za/legislation/pfma/act.pdf. |

| [62] | South Africa (2000) Guide for accounting officers. Public Finance Management Act. Available from: http://www.treasury.gov.za/legislation/pfma/guidelines/accounting%20officers%20guide%20to%20the%20pfma.pdf. |

| [63] | South Africa (2002) Protocol on corporate governance in the public sector. Available from: www.gov.za/sites/default/files/gcis_document/201409/corpgov0.pdf. |

| [64] | South Africa (2004) Public Audit Act, no. 25 of 2004. Available from: www.gov.za/sites/default/files/gcis_document/201409/a25-04.pdf. |

| [65] | South Africa (2005) Treasury regulations for departments, trading entities, constitutional institutions and public entities, issued in terms of the PFMA. Available from: www.treasury.gov.za/legislation/pfma/regulations/gazette_27388.pdf. |

| [66] | South Africa (2008) Companies Act, no. 71 of 2008. Available from: www.gov.za/sites/default/files/gcis_document/201409/321214210.pdf. |

| [67] |

Thomas A (2012) Governance at South African state‐owned enterprises: What do annual reports and the print media tell us? Soc Responsib J 8: 448–470. https://doi.org/10.1108/17471111211272057 doi: 10.1108/17471111211272057

|

| [68] | United States of America (USA) Department of State (2021) 2021 Investment Climate Statements. Available from: https://www.state.gov/reports/2021-investment-climate-statements/south-africa/. |

| [69] | Zhou S, Simnett R, Hoang H (2016) Combined assurance as a new assurance approach: is it beneficial to analysts? https://doi.org/10.2139/ssrn.2742010 |

| [70] |

Zhou S, Simnett R, Hoang H (2019) Evaluating combined assurance as a new credibility enhancement technique. Auditing-J Pract Th 38: 235–259. https://doi.org/10.2308/ajpt-52175. doi: 10.2308/ajpt-52175

|

NAR-05-01-004-s001.pdf NAR-05-01-004-s001.pdf |

|

Figures(5) / Tables(4)

Adeyemi Adebayo, Barry Ackers. Adoption of the combined assurance model by South African state-owned enterprises (SOEs)[J]. National Accounting Review, 2023, 5(1): 41-66. doi: 10.3934/NAR.2023004

DownLoad:

DownLoad: