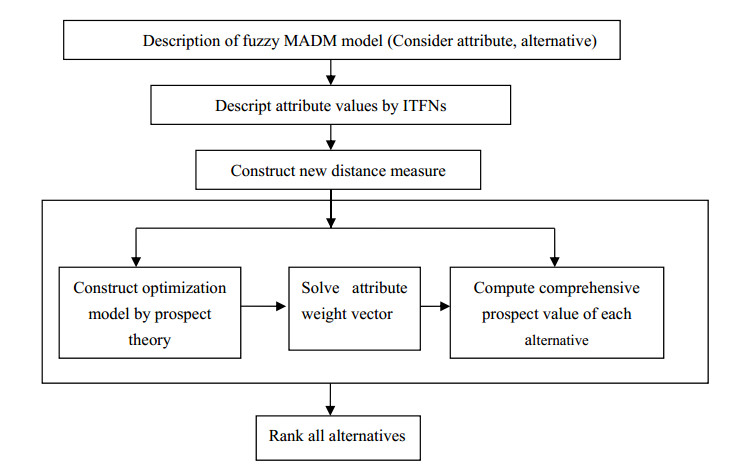

The aim of this paper is to develop a new decision making method considering decision makers' psychological behavior for multi-attribute decision making problem under intuitionistic trapezoidal fuzzy environment. We first put forward a new distance measure of intuitionistic trapezoidal fuzzy numbers. Then combining with cumulative prospect theory, we develop a novel decision making method, which can consider risk attitude of decision makers. Finally, an example is given to demonstrate the effectiveness and practicability of the proposed method.

Citation: Haiping Ren, Laijun Luo. A novel distance of intuitionistic trapezoidal fuzzy numbers and its-based prospect theory algorithm in multi-attribute decision making model[J]. Mathematical Biosciences and Engineering, 2020, 17(4): 2905-2922. doi: 10.3934/mbe.2020163

The aim of this paper is to develop a new decision making method considering decision makers' psychological behavior for multi-attribute decision making problem under intuitionistic trapezoidal fuzzy environment. We first put forward a new distance measure of intuitionistic trapezoidal fuzzy numbers. Then combining with cumulative prospect theory, we develop a novel decision making method, which can consider risk attitude of decision makers. Finally, an example is given to demonstrate the effectiveness and practicability of the proposed method.

| [1] |

G. Kou, P. Yang, Y. Peng, F. Xiao, Y. Chen, F. E. Alsaadic, Evaluation of feature selection methods for text classification with small datasets using multiple criteria decision-making methods, Appl. Soft Comput., 86 (2020), 105836. doi: 10.1016/j.asoc.2019.105836

|

| [2] |

G. Kou, D. Ergu, C. S. Lin, Y. Chen, Pairwise comparison matrix in multiple criteria decision making, Technol. Econ. Dev. Econ., 22 (2016), 738-765. doi: 10.3846/20294913.2016.1210694

|

| [3] |

G. Kou, Y. Q. Lu, Y. Peng, Y. Shi, Evaluation of classification algorithms using MCDM and rank correlation, Int. J. Inf. Tech. Decis., 11 (2012), 197-225. doi: 10.1142/S0219622012500095

|

| [4] | R. Joshi, S. Kumar, An exponential Jensen fuzzy divergence measure with applications in multiple attribute decision-making, Math. Probl. Eng., 2018 (2018), 4342098. |

| [5] |

G. Kou, Y. Peng, G. X. Wang, Evaluation of clustering algorithms for financial risk analysis using MCDM methods, Inform. Sciences, 275 (2014), 1-12 doi: 10.1016/j.ins.2014.02.137

|

| [6] |

H. Garg, K. Kumar, Distance measures for connection number sets based on set pair analysis and its applications to decision-making process, Appl. Intell., 48 (2018), 3346-3359. doi: 10.1007/s10489-018-1152-z

|

| [7] |

L. A. Zadeh, Fuzzy Sets, Inform. Control, 8 (1965), 338-353. doi: 10.1016/S0019-9958(65)90241-X

|

| [8] |

T. Jie, F. Meng, A consistency-based method to decision making with triangular fuzzy multiplicative preference relations, Int. J. Fuzzy Syst., 19 (2017), 1317-1332. doi: 10.1007/s40815-017-0333-y

|

| [9] |

A. Ebrahimnejad, J. L. Verdegay, H. Garg, Signed distance ranking based approach for solving bounded interval-valued fuzzy numbers linear programming problems, Int. J. Intell. Syst., 34 (2019), 2055-2076. doi: 10.1002/int.22130

|

| [10] |

K. T. Atanassov, Intuitionistic fuzzy sets, Fuzzy Set. Syst., 20 (1986), 87-96. doi: 10.1016/S0165-0114(86)80034-3

|

| [11] |

K. T. Atanassov, G. Gargov, Interval valued intuitionistic fuzzy sets, Fuzzy Set. Syst., 31 (1989), 343-349. doi: 10.1016/0165-0114(89)90205-4

|

| [12] | H. Garg, An improved cosine similarity measures for intuitionistic fuzzy sets and their applications to decision-making process, Hacet. J. Math. Stat., 47 (2018), 1585-1601. |

| [13] |

M. I. Ali, F. Feng, T. Mahmood, I. Mahmood, H. Faizan, A graphical method for ranking Atanassov's intuitionistic fuzzy values using the uncertainty index and entropy, Int. J. Intell. Syst., 34 (2019), 2692-2712. doi: 10.1002/int.22174

|

| [14] |

F. Feng, M. Liang, H. Fujita, R. R.Yager, X. Y. Liu, Lexicographic orders of intuitionistic fuzzy values and their relationships, Mathematics, 7 (2019), 166. doi: 10.3390/math7020166

|

| [15] |

P. Liu, Multiple attribute group decision making method based on interval-valued intuitionistic fuzzy power heronian aggregation operators, Comput. Ind. Eng., 108 (2017), 199-212. doi: 10.1016/j.cie.2017.04.033

|

| [16] |

H. Garg, K. Kumar, A novel exponential distance and its based TOPSIS method for interval-valued intuitionistic fuzzy sets using connection number of SPA theory, Artif. Intell. Rev., 53 (2020), 595-624. doi: 10.1007/s10462-018-9668-5

|

| [17] |

H. Garg, K. Kumar, Novel distance measures for cubic intuitionistic fuzzy sets and their applications to pattern recognitions and medical diagnosis, Granul. Comput., 5 (2020), 169-184. doi: 10.1007/s41066-018-0140-3

|

| [18] | A. Si, S. Das, S. Kar, An approach to rank picture fuzzy numbers for decision making problems, Decis. Ma-Appl. Manage. Eng., 2 (2019), 54-64. |

| [19] |

F. Liu, A. W. Guan, V. Lukovac, M. Vukić, A multicriteria model for the selection of the transport service provider: A single valued neutrosophic DEMATEL multicriteria model, Decis. Ma-Appl. Manage. Eng., 1 (2018), 121-130. doi: 10.31181/dmame1801121r

|

| [20] |

J. H. Hu, L. Pan, Y. Yang, H. W. Chen, A group medical diagnosis model based on intuitionistic fuzzy soft sets, Appl. Soft Comput., 77 (2019), 453-466. doi: 10.1016/j.asoc.2019.01.041

|

| [21] | F. Feng, H. Fujita, M. I. Ali, R. R. Yager, X. Liu, Another view on generalized intuitionistic fuzzy soft sets and related multiattribute decision making methods, IEEE T. Fuzzy Syst., 27 (2018), 474-488. |

| [22] |

H. Garg, R. Arora, Generalized and group-based generalized intuitionistic fuzzy soft sets with applications in decision-making, Appl. Intell., 48 (2018), 343-356. doi: 10.1007/s10489-017-0981-5

|

| [23] |

T. M. Athira, J. Sunil, H. Garg, Entropy and distance measures of Pythagorean fuzzy soft sets and their applications, J. Intell. Fuzzy Syst., 37 (2019), 4071-4084. doi: 10.3233/JIFS-190217

|

| [24] |

P. D. Liu, H. Gao, J. H. Ma, Novel green supplier selection method by combining quality function deployment with partitioned Bonferroni mean operator in interval type-2 fuzzy environment, Inform. Sciences, 490 (2019), 292-316. doi: 10.1016/j.ins.2019.03.079

|

| [25] |

P. D. Liu, P. Wang, Multiple-attribute decision-making based on archimedean Bonferroni operators of q-rung orthopair fuzzy numbers, IEEE T. Fuzzy Syst., 27 (2019), 834-848. doi: 10.1109/TFUZZ.2018.2826452

|

| [26] | P. D. Liu, S. Y. Ma, P. Wang, Multiple-attribute group decision-making based on q-rung orthopair fuzzy power Maclaurin symmetric mean operators, IEEE Trans. Syst. Man Cybern. Syst., 2018 (2018). |

| [27] |

M. H. Shu, C. H. Cheng, J. R. Chang, Using intuitionistic fuzzy sets for fault-tree analysis on printed circuit board assembly, Microelectron. Reliab., 46 (2006), 2139-2148. doi: 10.1016/j.microrel.2006.01.007

|

| [28] | J. Q. Wang, Z. Zhang, Programming method of multicriteria decision making based on intuitionistic fuzzy number with incomplete certain information, Control Decis., 23 (2008), 1145-1152. |

| [29] | J. Q. Wang, Z. Zhang, Aggregation operators on intuitionistic trapezoidal fuzzy number and its application to multi-criteria decision making problems, J. Syst. Eng. Electron., 20 (2009), 321-326. |

| [30] |

J. Ye, Expected value method for intuitionistic trapezoidal fuzzy multicriteria decision-making problems, Expert Syst. Appl., 38 (2011), 11730-11734. doi: 10.1016/j.eswa.2011.03.059

|

| [31] |

J. Yuan, C. Li, A new method for multi-attribute decision making with intuitionistic trapezoidal fuzzy random variable, Int. J. Fuzzy Syst., 19 (2017), 15-26. doi: 10.1007/s40815-016-0184-y

|

| [32] |

D. Kahneman, A. Tversky, Prospect theory: an analysis of decision under risk, Econometrica, 47 (1979), 263-292. doi: 10.2307/1914185

|

| [33] |

P. D. Liu, Y. Li, An extended MULTIMOORA method for probabilistic linguistic multi-criteria group decision-making based on prospect theory, Comput. Ind. Eng., 136 (2019), 528-545. doi: 10.1016/j.cie.2019.07.052

|

| [34] |

A. Tversky, D. Kahneman, Advances in prospect theory: cumulative representation of uncertainty, J. Risk Uncertainty, 5 (1992), 297-323. doi: 10.1007/BF00122574

|

| [35] | Z. S. Chen, S. H. Xiong, Y. L. Li, G. S. Qian, Approach for intuitionistic trapezoidal fuzzy random prospect decision making based on the combination of parameter estimation and score functions, J. Syst. Eng. Electron., 37 (2015), 851-862. |

| [36] | Q. G. Ma, Hesitant fuzzy multi-attribute group decision-making method based on prospect theory, Comput. Eng. Appl., 51 (2015), 249-253. |

| [37] |

S. Z. Zeng, W. H. Su, J. Chen, Fuzzy decision making with induced heavy aggregation operators and distance measures, J. Intell. Fuzzy Syst., 26 (2014), 127-135. doi: 10.3233/IFS-120720

|

| [38] |

P. Grzegorzewski, Metrics and orders in space of fuzzy numbers, Fuzzy Set. Syst., 97 (1998), 83-94 doi: 10.1016/S0165-0114(96)00322-3

|

| [39] |

A. I. Ban, L. Coroianu, Nearest interval, triangular and trapezoidal approximation of a fuzzy number preserving ambiguity, Int. J. Approx. Reason., 53 (2012), 805-836 doi: 10.1016/j.ijar.2012.02.001

|

| [40] |

U. Sharma, S. Aggarwal, Solving fully fuzzy multi-objective linear programming problem using nearest interval approximation of fuzzy number and interval programming, Int. J. Fuzzy Syst., 20 (2018), 488-499. doi: 10.1007/s40815-017-0336-8

|

| [41] |

R. Joshi, S. Kumar, Jensen-Tsalli's intuitionistic fuzzy divergence measure and its applications in medical analysis and pattern recognition, Int. J. Uncertain. Fuzz., 27 (2019), 145-169. doi: 10.1142/S0218488519500077

|

Figures(1) / Tables(6)

Haiping Ren, Laijun Luo. A novel distance of intuitionistic trapezoidal fuzzy numbers and its-based prospect theory algorithm in multi-attribute decision making model[J]. Mathematical Biosciences and Engineering, 2020, 17(4): 2905-2922. doi: 10.3934/mbe.2020163

DownLoad:

DownLoad: