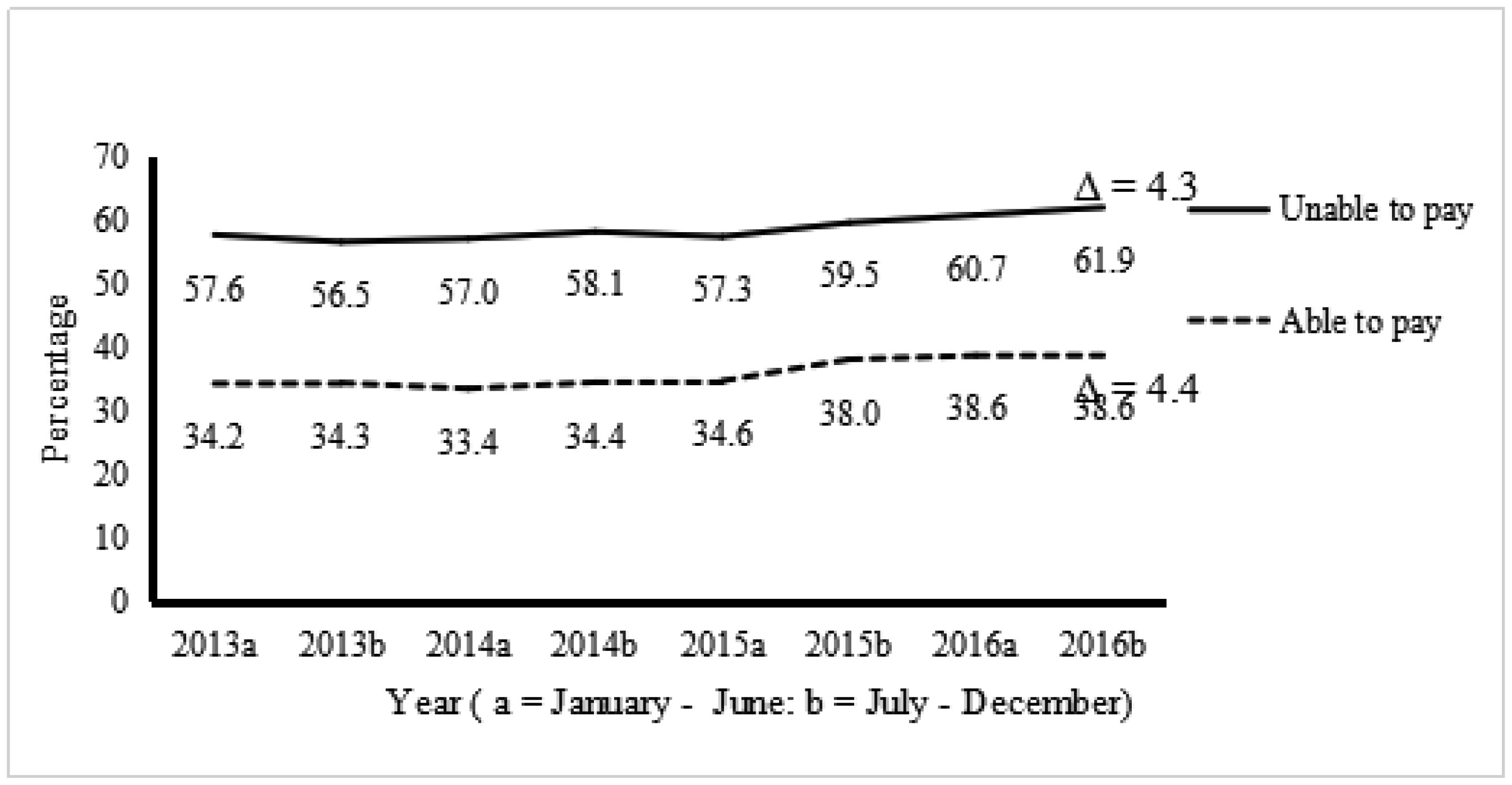

Healthcare affordability is a worry for many Americans. We examine whether the relationship between having problems paying medical bills and mental health problems changed as the Affordable Care Act (ACA) was implemented, which increased health insurance coverage. Data from the 2013–2016 Health Reform Monitoring Survey, a survey of Americans aged 18–64, were used. Using zero-inflated negative binomial regression, adjusted for predisposing, enabling, and need factors, we examined differences in days of mental health symptoms by problems paying medical bills (n = 85,430). From 2013 to 2016, the rates of uninsured and problems paying medical bills decreased from 15.1% to 9.0% and 22.0% to 18.6%, respectively. Having one or more days of mental health symptoms increased from 39.3% to 42.9%. Individuals who reported problems paying medical bills had more days of mental health symptoms (Beta = 0.133, p < 0.001) than those who did not have this problem. Insurance was not significantly associated with days of mental health symptoms. Over the 4-year period, there were not significant differences in days of mental health symptoms by problems paying medical bills or insurance status. Despite improvements in coverage, the relationship between problems paying medical bills and mental health symptoms was not modified.

Citation: Jacqueline C Wiltshire, Kimberly R Enard, Edlin Garcia Colato, Barbara Langland Orban. Problems paying medical bills and mental health symptoms post-Affordable Care Act[J]. AIMS Public Health, 2020, 7(2): 274-286. doi: 10.3934/publichealth.2020023

Healthcare affordability is a worry for many Americans. We examine whether the relationship between having problems paying medical bills and mental health problems changed as the Affordable Care Act (ACA) was implemented, which increased health insurance coverage. Data from the 2013–2016 Health Reform Monitoring Survey, a survey of Americans aged 18–64, were used. Using zero-inflated negative binomial regression, adjusted for predisposing, enabling, and need factors, we examined differences in days of mental health symptoms by problems paying medical bills (n = 85,430). From 2013 to 2016, the rates of uninsured and problems paying medical bills decreased from 15.1% to 9.0% and 22.0% to 18.6%, respectively. Having one or more days of mental health symptoms increased from 39.3% to 42.9%. Individuals who reported problems paying medical bills had more days of mental health symptoms (Beta = 0.133, p < 0.001) than those who did not have this problem. Insurance was not significantly associated with days of mental health symptoms. Over the 4-year period, there were not significant differences in days of mental health symptoms by problems paying medical bills or insurance status. Despite improvements in coverage, the relationship between problems paying medical bills and mental health symptoms was not modified.

| [1] |

Dickman SL, Himmelstein DU, Woolhandler S (2017) Inequality and the health-care system in the USA. Lancet 389: 1431-1441. doi: 10.1016/S0140-6736(17)30398-7

|

| [2] | Collins SR, Bhupal HK, Doty MM (2019) Health insurance coverage eight years after the ACA: Fewer uninsured Americans and shorter coverage gaps, but more underinsured. N Y (Commonw Fund) 1-27. |

| [3] | DiJulio B, Kirzinger A, Wu B, et al. (2019) Data Note: Americans' Challenges with Health Care Costs.Available from: https://www.kff.org/health-costs/poll-finding/data-note-americans-challenges-with-health-care-costs/. |

| [4] |

Cunningham PJ (2015) The share of people with high medical costs increased prior to implementation of the Affordable Care Act. Health Aff (Millwood) 34: 117-124. doi: 10.1377/hlthaff.2014.0216

|

| [5] |

Wiltshire JC, Elder K, Kiefe C, et al. (2016) Medical debt and related financial consequences among older African American and White adults. Am J Public Health 106: 1086-1091. doi: 10.2105/AJPH.2016.303137

|

| [6] |

Richman IB, Brodie M (2014) A National study of burdensome health care costs among non-elderly Americans. BMC Health Serv Res 14: 435-446. doi: 10.1186/1472-6963-14-435

|

| [7] | Hamel L, Norton M, Pollitz K, et al. (2019) The Burden of Medical Debt: Results from the Kaiser Family Foundation/New York Times Medical Bill Survey.Available from: https://kaiserfamilyfoundation.files.wordpress.com/2016/01/8806-the-burden-of-medical-debt-results-from-the-kaiser-family-foundation-new-york-times-medical-bills-survey.pdf. |

| [8] |

Nguyen OK, Higashi RT, Makam AN, et al. (2018) The influence of financial strain on health decision-making. J Gen Int Med 33: 406-408. doi: 10.1007/s11606-017-4296-3

|

| [9] |

Yabroff KR, Zhao JX, Han XS, et al. (2019) Prevalence and correlates of medical financial hardship in the USA. J Gen Int Med 34: 1494-1502. doi: 10.1007/s11606-019-05002-w

|

| [10] | Hamel L, Wu B, Brodie M, et al. (2019) The health care priorities and experiences of California residents. Kaiser Family Foundation.Available from: http://files.kff.org/attachment/Report-The-Health-Care-Priorities-and-Experiences-of-California-Residents. |

| [11] |

Emanuel EJ, Glickman A, Johnson D (2017) Measuring the burden of health care costs on US families the affordability index. J Am Med Assoc 318: 1863-1864. doi: 10.1001/jama.2017.15686

|

| [12] |

Fitzgerald MP, Bias TK, Gurley-Calvez T (2015) The Affordable Care Act and consumer well-being: Knowns and unknowns. J Consumer Aff 51: 27-53. doi: 10.1111/joca.12059

|

| [13] | Karpman M, Long SK (2019) Most Adults with Medical Debt had Health Insurance at the Time the Debt was Incurred.Available from: http://hrms.urban.org/briefs/Most-Adults-with-Medical-Debt-Had-Health-Insurance-at-the-Time-the-Debt-Was-Incurred.html. |

| [14] |

Richardson T, Elliott P, Roberts R (2013) The relationship between personal unsecured debt and mental and physical health: A systematic review and meta-analysis. Clin Psychol Rev 33: 1148-1162. doi: 10.1016/j.cpr.2013.08.009

|

| [15] | Stress in America (2018) Stress in America: Uncertainty about health care.Available from: https://www.apa.org/news/press/releases/stress/2017/uncertainty-health-care.pdf. |

| [16] |

Sweet E, Nandi A, Adam EK, et al. (2013) The high price of debt: Household financial debt and its impact on mental and physical health. Soc Sci Med 91: 94-100. doi: 10.1016/j.socscimed.2013.05.009

|

| [17] |

Zurlo KA, Yoon W, Kim H (2014) Unsecured consumer debt and mental health outcomes in middle-aged and older Americans. J Gerontol B Psychol Sci Soc Sci 69: 461-469. doi: 10.1093/geronb/gbu020

|

| [18] |

Fitch C, Hamilton S, Bassett P, et al. (2011) The relationship between personal debt and mental health: A systematic review. Ment Health Rev J 16: 153-166. doi: 10.1108/13619321111202313

|

| [19] |

Jacobs AW, Hill TD, Burdette AM (2015) Health insurance status and symptoms of psychological distress among low-income urban women. Soc Ment Health 5: 1-15. doi: 10.1177/2156869314549674

|

| [20] | Yelowitz A, Cannon MF (2010) The Massachusetts health plan much pain, little gain. Policy Anal 657: 1-16. |

| [21] | Courtemanche C, Marton J, Ukert B, et al. (2018) Effects of the Affordable Care Act on health care access and self-assessed health after 3 years. Inquiry J Health Car 55. |

| [22] |

Courtemanche C, Marton J, Ukert B, et al. (2018) Early effects of the Affordable Care Act on health care access, risky health behaviors, and self-assessed health. Southern Econ J 84: 660-691. doi: 10.1002/soej.12245

|

| [23] |

Turunen E, Hiilamo H (2014) Health effects of indebtedness: A systematic review. BMC Public Health 14. doi: 10.1186/1471-2458-14-489

|

| [24] |

Andersen RM (1995) Revisiting the behavioral model and access to medical care: Does it matter? J Health Soc Behav 36: 1-10. doi: 10.2307/2137284

|

| [25] |

Andersen RM (2008) National health surveys and the Behavioral Model of Health Services Use. Med Care 46: 647-653. doi: 10.1097/MLR.0b013e31817a835d

|

| [26] |

Banthin JS, Bernard DM (2006) Changes in financial burdens for health care: national estimates for the population younger than 65 years, 1996 to 2003. Jama 296: 2712-2719. doi: 10.1001/jama.296.22.2712

|

| [27] |

Rahimi AR, Spertus JA, Reid KJ, et al. (2007) Financial barriers to health care and outcomes after acute myocardial infarction. Jama 297: 1063-1072. doi: 10.1001/jama.297.10.1063

|

| [28] |

Relyea-Chew A, Hollingworth W, Chan L, et al. (2009) Personal bankruptcy after traumatic brain or spinal cord injury: The role of medical debt. Arch Phys Med Rehabil 90: 413-419. doi: 10.1016/j.apmr.2008.07.031

|

| [29] | Wiltshire JC, Dark T, Brown RL, et al. (2011) Gender differences in financial hardships of medical debt. J Health Care Poor Underserved 22: 371-388. |

| [30] |

Wiltshire JC, Elder K, Allison JJ (2015) Differences in problems paying medical bills between African Americans and Whites from 2007 and 2009: The underlying role of health status. J Racial Ethn Health Disparities 3: 381-388. doi: 10.1007/s40615-015-0197-5

|

| [31] | Holahan J, Long SK (2017) Health Reform Monitoring Survey, First Quarter, United States, 2013.Available from: https://www.icpsr.umich.edu/web/HMCA/studies/35624. |

| [32] |

Long SK, Kenney GM, Zuckerman S, et al. (2014) The Health Reform Monitoring Survey: Addressing data gaps to provide timely insights into the Affordable Care Act. Health Aff (Millwood) 33: 161-167. doi: 10.1377/hlthaff.2013.0934

|

| [33] | Holahan J, Long SK (2019) Health Reform Monitoring Survey, Third Quarter, United States, 2016.Available from: https://www.icpsr.umich.edu/web/HMCA/studies/36842. |

| [34] |

Hardin JW, Hilbe JM (2014) Regression models for count data based on the negative binomial(p) distribution. Stata J 14: 280-291. doi: 10.1177/1536867X1401400203

|

| [35] |

Xu T, Zhu GJ, Han SM (2017) Study of depression influencing factors with zero-inflated regression models in a large-scale population survey. Bmj Open 7: e016471. doi: 10.1136/bmjopen-2017-016471

|

| [36] |

Yang S, Harlow LL, Puggioni G, et al. (2017) A comparison of different methods of zero-inflated data analysis and an application in health surveys. J Mod Appl Stat Meth 16: 518-543. doi: 10.22237/jmasm/1493598600

|

| [37] |

Gunasinghe C, Gazard B, Aschan L, et al. (2018) Debt, common mental disorders and mental health service use. J Ment Health 27: 520-528. doi: 10.1080/09638237.2018.1487541

|

| [38] | Gallup Inc (2019) Healthcare system. Gallup.Available from: https://news.gallup.com/poll/4708/healthcare-system.aspx. |

| [39] | Kirzinger A, Munana C, Wu B, et al. (2019) Data note: Americans' Challenges with Health Care Costs.Available from: https://www.kff.org/report-section/data-note-americans-challenges-with-health-care-costs-appendices/. |

| [40] |

Weissman J, Russell D, Jay M, et al. (2017) Disparities in health care utilization and functional limitations among adults with serious psychological distress, 2006–2014. Psychiatr Serv 68: 653-659. doi: 10.1176/appi.ps.201600260

|

| [41] |

Agarwal R, Mazurenko O, Menachemi N (2017) High-deductible health plans reduce health care cost and utilization, including use of needed preventive services. Health Aff (Millwood) 36: 1762-1768. doi: 10.1377/hlthaff.2017.0610

|

| [42] | Collins SR, Gunja MZ, Doty MM (2017) How well does insurance coverage protect consumers from health care costs? Findings from the Commonwealth Fund Biennial Health Insurance Survey, 2016.Available from: https://nchc.org/wp-content/uploads/2017/11/Collins_NCHC-Forum-10.30.17.pdf. |

| [43] |

Skinner J, Chandra A (2016) The past and future of the Affordable Care Act. Jama J Am Med Assoc 316: 497-499. doi: 10.1001/jama.2016.10158

|

| [44] |

Hidaka BH (2012) Depression as a disease of modernity: Explanations for increasing prevalence. J Affect Disord 140: 205-214. doi: 10.1016/j.jad.2011.12.036

|

| [45] |

Weinberger AH, Gbedemah M, Martinez AM, et al. (2018) Trends in depression prevalence in the USA from 2005 to 2015: Widening disparities in vulnerable groups. Psychol Med 48: 1308-1315. doi: 10.1017/S0033291717002781

|

| [46] |

Miller S, Wherry LR (2017) Health and access to care during the first 2 years of the ACA Medicaid expansions. N Engl J Med 376: 947-956. doi: 10.1056/NEJMsa1612890

|

| [47] |

Courtemanche CJ, Zapata D (2014) Does universal coverage improve health? The Massachusetts experience. J Policy Anal Manage 33: 36-69. doi: 10.1002/pam.21737

|

| [48] |

Van der Wees PJ, Zaslavsky AM, Ayanian JZ (2013) Improvements in health status after Massachusetts health care reform. Milbank Q 91: 663-689. doi: 10.1111/1468-0009.12029

|

| [49] |

Shartzer A, Long SK, Anderson N (2016) Access to care and affordability have improved following Affordable Care Act implementation; Problems remain. Health Aff (Millwood) 35: 161-168. doi: 10.1377/hlthaff.2015.0755

|

| [50] |

Pascale J (2008) Measurement error in health insurance reporting. Inquiry 45: 422-437. doi: 10.5034/inquiryjrnl_45.04.422

|

| [51] |

Schoen C, Osborn R, Squires D, et al. (2013) Access, affordability, and insurance complexity are often worse in The United States compared to ten other countries. Health Aff (Millwood) 32: 2205-2215. doi: 10.1377/hlthaff.2013.0879

|

| [52] |

Wharam JF, Ross-Degnan D, Rosenthal MB (2013) The ACA and high-deductible insurance-strategies for sharpening a blunt instrument. N Engl J Med 369: 1481-1484. doi: 10.1056/NEJMp1309490

|

| [53] |

Vogus TJ, Singer SJ (2016) creating highly reliable accountable care organizations. Med Care Res Rev 73: 660-672. doi: 10.1177/1077558716640413

|

| [54] |

Dine CJ, Masi D, Smith CD (2019) Tools to help overcome barriers to cost-of-care conversations. Ann Intern Med 170: S36-U89. doi: 10.7326/M19-0778

|

| [55] |

Hardee JT, Platt FW, Kasper IK (2005) Discussing health care costs with patients-an opportunity for empathic communication. J Gen Intern Med 20: 666-669. doi: 10.1111/j.1525-1497.2005.0125.x

|

| [56] |

Hunter WG, Hesson A, Davis JK, et al. (2016) Patient-physician discussions about costs: Definitions and impact on cost conversation incidence estimates. BMC Health Serv Res 16: 108-120. doi: 10.1186/s12913-016-1353-2

|

| [57] |

Bradham DD, Garcia D, Galvan A, et al. (2019) Cost-of-care conversations during clinical visits in federally qualified health centers an observational study. Ann Int Med 170: S87-U73. doi: 10.7326/M18-1608

|

| [58] |

Glied S (2019) Options for dialing down from single payer. Am J Public Health 109: 1517-1520. doi: 10.2105/AJPH.2019.305299

|

| [59] |

Petrou P, Samoutis G, Lionis C (2018) Single-payer or a multipayer health system: A systematic literature review. Public Health 163: 141-152. doi: 10.1016/j.puhe.2018.07.006

|

Figures(1) / Tables(2)

Jacqueline C Wiltshire, Kimberly R Enard, Edlin Garcia Colato, Barbara Langland Orban. Problems paying medical bills and mental health symptoms post-Affordable Care Act[J]. AIMS Public Health, 2020, 7(2): 274-286. doi: 10.3934/publichealth.2020023

DownLoad:

DownLoad: