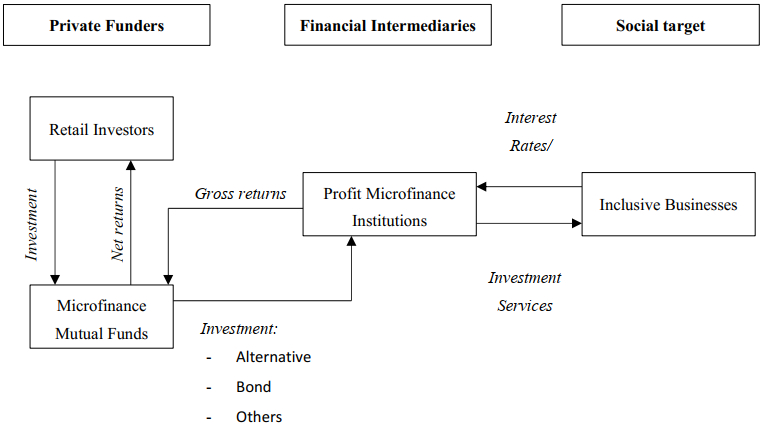

Mutual funds could contribute to sustainable development by investing in microfinance institutions that provide microloans to microfirms with difficulties accessing financial services, such as loans, savings, and insurance from traditional banks. To increase their assets and support microfinance institutions, fund managers need to understand the factors that investors use to make their investment decisions. For microfinance investors, fund financial attributes could signal that microfinance institutions provide support to microentrepreneurs that improve their corporate financial performance. This would satisfy the social preferences of fund investors. Therefore, our research question is: Are investors considering past financial performance to select one specific microfinance mutual fund? To answer this question, we analysed the behaviour of microfinance mutual fund investors regarding past financial performance in different states of the economy. To this end, we collected information on 65 microfinance mutual funds domiciled in Austria, Japan, Liechtenstein, and Luxembourg. These mutual funds invested in global or emerging global markets from 2015 to 2021. For this sample, we implemented Petersen's method, which clusters standard errors by fund and year. These results indicated that microfinance mutual fund investors consider high annual raw returns, fund age, and ethical certifications when making investment decisions and withdrawing money from them during crises such as the COVID-19 pandemic. Conversely, microfinance fund investors do not react to past risk-adjusted returns, total risk, fund size, fund expenses, or fund flows.

Citation: Carmen-Pilar Martí-Ballester, Buket Erden. Fund performance—flow relationship for microfinance mutual funds[J]. Quantitative Finance and Economics, 2025, 9(3): 573-601. doi: 10.3934/QFE.2025020

Mutual funds could contribute to sustainable development by investing in microfinance institutions that provide microloans to microfirms with difficulties accessing financial services, such as loans, savings, and insurance from traditional banks. To increase their assets and support microfinance institutions, fund managers need to understand the factors that investors use to make their investment decisions. For microfinance investors, fund financial attributes could signal that microfinance institutions provide support to microentrepreneurs that improve their corporate financial performance. This would satisfy the social preferences of fund investors. Therefore, our research question is: Are investors considering past financial performance to select one specific microfinance mutual fund? To answer this question, we analysed the behaviour of microfinance mutual fund investors regarding past financial performance in different states of the economy. To this end, we collected information on 65 microfinance mutual funds domiciled in Austria, Japan, Liechtenstein, and Luxembourg. These mutual funds invested in global or emerging global markets from 2015 to 2021. For this sample, we implemented Petersen's method, which clusters standard errors by fund and year. These results indicated that microfinance mutual fund investors consider high annual raw returns, fund age, and ethical certifications when making investment decisions and withdrawing money from them during crises such as the COVID-19 pandemic. Conversely, microfinance fund investors do not react to past risk-adjusted returns, total risk, fund size, fund expenses, or fund flows.

| [1] |

Abrar A, Hasan I, Kabir R (2023) What makes the difference? Microfinance versus commercial banks. Borsa Istanbul Rev 23: 759–778. https://doi.org/10.1016/j.bir.2023.03.007 doi: 10.1016/j.bir.2023.03.007

|

| [2] |

Alda M, Muñoz F, Vargas M (2020) Socially responsible mutual fund exit decisions. Bus Ethics 29: 82–97. https://doi.org/10.1111/beer.12253 doi: 10.1111/beer.12253

|

| [3] |

Alves C, Mendes V (2011) Does performance explain mutual fund flows in small markets? The case of Portugal. Port Econ J 10: 129–147. https://doi.org/10.1007/s10258-010-0060-x doi: 10.1007/s10258-010-0060-x

|

| [4] |

Arellano M, Bover O (1995) Another look at the instrumental variable estimation of error-components models. J Econometrics 68: 29–51. https://doi.org/10.1016/0304-4076(94)01642-D doi: 10.1016/0304-4076(94)01642-D

|

| [5] |

Aziz A, Iqbal J, Murtza MH, et al. (2024) Effect of COVID-19 pandemic on women entrepreneurial sustainability: the role of Islamic microfinance institutions. J Econom Adm Sci 40: 819–836. https://doi.org/10.1108/JEAS-08-2021-0166 doi: 10.1108/JEAS-08-2021-0166

|

| [6] |

Bachmann K, Meyer J, Krauss A (2024) Investment Motives and Performance Expectations of Impact Investors. J Behav Exp Finance 42: 100911. https://doi.org/10.1016/j.jbef.2024.100911 doi: 10.1016/j.jbef.2024.100911

|

| [7] |

Ben-David I, Li J, Rossi A, et al. (2022) What do mutual fund investors really care about? Rev Financ Stud 35: 1723–1774. https://doi.org/10.1093/rfs/hhab081 doi: 10.1093/rfs/hhab081

|

| [8] |

Benson KL, Humphrey JE (2008) Socially responsible investment funds: Investor reaction to current and past returns. J Bank Financ 32: 1850–1859. https://doi.org/10.1016/j.jbankfin.2007.12.013 doi: 10.1016/j.jbankfin.2007.12.013

|

| [9] |

Berk JB, Green RC (2004) Mutual fund flows and performance in rational markets. J Polit Econ 112: 1269–1295. https://doi.org/10.1086/424739 doi: 10.1086/424739

|

| [10] | Blundell R, Bond S (1998) GMM estimation with persistent panel data: an application to production functions: The Institute for Fiscal Studies Working Paper Series No. W99/4. |

| [11] |

Bollen NP (2007) Mutual fund attributes and investor behavior. J Financ Quant Anal 42: 683–708. https://doi.org/10.1016/j.jbankfin.2016.10.009 doi: 10.1016/j.jbankfin.2016.10.009

|

| [12] |

Brickell K, Picchioni F, Natarajan N, et al. (2020) Compounding crises of social reproduction: Microfinance, over-indebtedness and the COVID-19 pandemic. World Dev 136: 105087. https://doi.org/10.1016/j.worlddev.2020.105087 doi: 10.1016/j.worlddev.2020.105087

|

| [13] |

Ceccarelli M, Ramelli S, Wagner AF (2024) Low carbon mutual funds. Rev Financ 28: 45–74. https://doi.org/10.1093/rof/rfad015 doi: 10.1093/rof/rfad015

|

| [14] |

Chevalier J, Ellison G (1997) Risk taking by mutual funds as a response to incentives. J Polit Econ 105: 1167–1200. https://doi.org/10.1086/516389 doi: 10.1086/516389

|

| [15] |

Chung H, Lee HH, Tsai PC (2012) Are green fund investors really socially responsible? Rev Pac Basin Financ 15: 1250023. https://doi.org/10.1142/S0219091512500233 doi: 10.1142/S0219091512500233

|

| [16] |

Ciccone J, Marchiori L, Morhs R (2022) The flowperformance relationship of global investment funds. J Int Money Finance 127: 102690. https://doi.org/10.1016/j.jimonfin.2022.102690 doi: 10.1016/j.jimonfin.2022.102690

|

| [17] |

Constantinou D, Ashta A (2011) Financial crisis: Lessons from microfinance. Strateg Chang 20: 187–203. https://doi.org/10.1002/jsc.895 doi: 10.1002/jsc.895

|

| [18] |

Czura K, Englmaier F, Ho H, et al. (2022) Microfinance loan officers before and during Covid-19: Evidence from India. World Dev 152: 105812. https://doi.org/10.1016/j.worlddev.2022.105812 doi: 10.1016/j.worlddev.2022.105812

|

| [19] |

Daugaard D (2020) Emerging new themes in environmental, social and governance investing: a systematic literature review. Account Finance 60: 1501–1530. https://doi.org/10.1111/acfi.12479 doi: 10.1111/acfi.12479

|

| [20] |

Daher L, Le Saout E (2013) Microfinance and financial performance. Strateg Chang 22: 31–45. https://doi.org/10.1002/jsc.1920 doi: 10.1002/jsc.1920

|

| [21] |

Daher L, Le Saout E (2015) The determinants of the financial performance of microfinance institutions: impact of the global financial crisis. Strateg Chang 24: 131–148. https://10.1002/jsc.2002 doi: 10.1002/jsc.2002

|

| [22] |

Del Guercio D, Reuter J (2014) Mutual fund performance and the incentive to generate alpha. J Financ 69: 1673–1704. https://doi.org/10.1111/jofi.12048 doi: 10.1111/jofi.12048

|

| [23] | Dorfleitner G, Leidl M, Priberny C (2014) Explaining failures of microfinance institutions. Social Science Research Network: SSRN. |

| [24] |

Dorfleitner G, Priberny C, Röhe M (2017a) Why do microfinance institutions fail socially? A global empirical examination. Finance Res Lett 22: 81–89. https://doi.org/10.1016/j.frl.2016.12.027 doi: 10.1016/j.frl.2016.12.027

|

| [25] |

Dorfleitner G, Röhe M, Renier N (2017b) The access of microfinance institutions to debt capital: An empirical investigation of microfinance investment vehicles. Q Rev Econ Fin 65: 1–15. https://doi.org/10.1016/j.qref.2016.06.005 doi: 10.1016/j.qref.2016.06.005

|

| [26] |

Eddleston KA, Ladge JJ, Mitteness C, et al. (2016) Do you see what I see? Signaling effects of gender and firm characteristics on financing entrepreneurial ventures. Entrep Theory Pract 40: 489–514. https://doi.org/10.1111/etap.12117 doi: 10.1111/etap.12117

|

| [27] |

El Ghoul S, Karoui A (2021). What is its name (green)? Effects of greening fund names on fund flows, turnover, and performance. Finance Res Lett 39: 101620. https://doi.org/10.1016/j.frl.2020.101620 doi: 10.1016/j.frl.2020.101620

|

| [28] |

El Ghoul S, Karoui A (2017) Does corporate social responsibility affect mutual fund performance and flows?. J Bank Financ 77: 53–63. https://doi.org/10.1016/j.jbankfin.2016.10.009 doi: 10.1016/j.jbankfin.2016.10.009

|

| [29] |

Elton EJ, Gruber MJ, Das S, et al. (1993) Efficiency with costly information: A reinterpretation of evidence from managed portfolios. Rev Financ Stud 6: 1-22. https://doi.org/10.1093/rfs/6.1.1 doi: 10.1093/rfs/6.1.1

|

| [30] | Eurosif (2021) Eurosif Report 2021: Fostering Investor Impact Placing it at the Heart of Sustainable Finance. Available from: https://www.eurosif.org/wpcontent/uploads/2021/11/2021-Eurosif-Report-Fostering-investor-impact.pdf. |

| [31] |

Fecht F, Wedow M (2014) The dark and the bright side of liquidity risks: Evidence from open-end real estate funds in Germany. J Financ Intermediation 23: 376–399. https://doi.org/10.1016/j.jfi.2014.02.002 doi: 10.1016/j.jfi.2014.02.002

|

| [32] |

Ferreira MA, Keswani A, Miguel AF, et al. (2012) The flow-performance relationship around the world. J Bank Financ 36: 1759–1780. https://doi.org/10.1016/j.jbankfin.2012.01.019 doi: 10.1016/j.jbankfin.2012.01.019

|

| [33] | Global Impact Investing Network-GIIN (2023) Holistic portfolio construction with an impact lens: a vital approach for institutional asset owners in a changing world. Available from: https://thegiin.org/publication/research/holistic-portfolio-construction-with-an-impact-lens-a-vital-approach-for-institutional-asset-owners-in-a-changing-world/. |

| [34] |

Goetzmann WN, Peles N (1997) Cognitive dissonance and mutual fund investors. J Financ Res 20: 145–158. https://doi.org/10.1111/j.1475-6803.1997.tb00241.x doi: 10.1111/j.1475-6803.1997.tb00241.x

|

| [35] |

Gruber MJ (1996) Another puzzle: The growth in actively managed mutual funds. J Financ 51: 783-810. https://doi.org/10.1111/j.1540-6261.1996.tb02707.x doi: 10.1111/j.1540-6261.1996.tb02707.x

|

| [36] |

Hacıömeroğlu HA, Danışoğlu S, Güner ZN, et al. (2022) The Agency Cost of Investing in Ethical Funds: A Style Analysis Approach. Borsa Istanbul Rev 22: S169–S179. https://doi.org/10.1016/j.bir.2022.11.007 doi: 10.1016/j.bir.2022.11.007

|

| [37] |

Hahn R (2012) Inclusive business, human rights and the dignity of the poor: a glance beyond economic impacts of adapted business models. Bus Ethics: Eur Rev 21: 47–63. https://doi.org/10.1111/j.1467-8608.2011.01640.x doi: 10.1111/j.1467-8608.2011.01640.x

|

| [38] |

Hassan MK, Alshater MM, Hasan R, et al. (2021) Islamic microfinance: A bibliometric review. Glob Fin J 49: 100651. https://doi.org/10.1016/j.gfj.2021.100651 doi: 10.1016/j.gfj.2021.100651

|

| [39] |

Hermes N, Hudon M (2019) Determinants of the performance of microfinance institutions: A systematic review, Contemporary Topics in Finance: A Collection of Literature Surveys, 297–330. https://doi.org/10.1002/9781119565178.ch10 doi: 10.1002/9781119565178.ch10

|

| [40] |

Hoechle D (2007) Robust standard errors for panel regressions with cross-sectional dependence. Stata J 7: 281–312. https://doi.org/10.1177/1536867X0700700301 doi: 10.1177/1536867X0700700301

|

| [41] |

Jackson ET (2013) Interrogating the theory of change: evaluating impact investing where it matters most. J Sustain Finance Invest 3: 95–110. https://doi.org/10.1080/20430795.2013.776257 doi: 10.1080/20430795.2013.776257

|

| [42] |

Jain BA, Jayaraman N, Kini O (2008) The path-to-profitability of Internet IPO firms. J Bus Ventur 23: 165–194. https://doi.org/10.1016/j.jbusvent.2007.02.004 doi: 10.1016/j.jbusvent.2007.02.004

|

| [43] |

Janda K, Rausser G, Svárovská B (2014) Can investment in microfinance funds improve risk-return characteristics of a portfolio? Technol Econ Dev Econ 20: 673–695. https://doi.org/10.3846/20294913.2014.869514 doi: 10.3846/20294913.2014.869514

|

| [44] |

Janda K, Svárovská B (2010) Investing into microfinance. J Bus Econ Manag 11: 483–510. https://doi.org/10.3846/jbem.2010.24 doi: 10.3846/jbem.2010.24

|

| [45] |

Jiang GJ, Yüksel HZ (2019) Sentimental mutual fund flows. Financ Rev 54: 709–738. https://doi.org/10.1111/fire.12201 doi: 10.1111/fire.12201

|

| [46] |

Lapanan N (2018) The investment behavior of socially responsible individual investors. Q Rev Econ Fin 70: 214–226. https://doi.org/10.1016/j.qref.2018.05.014 doi: 10.1016/j.qref.2018.05.014

|

| [47] | Le Saout E, Daher L (2016) Microfinance Performance in Financial Markets: The Case of Microfinance Investment Vehicles, In: Accountability and Social Responsibility: International Perspectives (Developments in Corporate Governance and Responsibility, Bingley: Emerald Group Publishing Limited, Bingley, 101–123. https://doi.org/10.1108/S2043-052320160000009005 |

| [48] |

Lei H, Xue M, Liu H, et al. (2023) Precious metal as a safe haven for global ESG stocks: Portfolio implications for socially responsible investing. Resour Policy 80: 103170. https://doi.org/10.1016/j.resourpol.2022.103170 doi: 10.1016/j.resourpol.2022.103170

|

| [49] |

Lynch AW, Musto DK (2003) How investors interpret past fund returns. J Financ 58: 2033–2058. https://doi.org/10.1111/1540-6261.00596 doi: 10.1111/1540-6261.00596

|

| [50] |

Malik K, Meki M, Morduch J, et al. (2020) COVID-19 and the Future of Microfinance: Evidence and Insights from Pakistan. Oxf Rev Econ Policy 36: S138–S168. https://doi.org/10.1093/oxrep/graa014 doi: 10.1093/oxrep/graa014

|

| [51] |

Markowitz H (1952) Portfolio selection. J Financ 7: 77–91. https://doi.org/10.1111/j.1540-6261.1952.tb01525.x doi: 10.1111/j.1540-6261.1952.tb01525.x

|

| [52] |

Martí-Ballester CP (2020) Examining the behavior of renewable‐energy fund investors. Bus Strategy Environ 29: 2624–2634. https://doi.org/10.1002/bse.2525 doi: 10.1002/bse.2525

|

| [53] | Martí-Ballester CP (2024). Analysing the financial performance of microfinance mutual funds, In: Duarte, F., Gama, A.P.M., Augusto, M., Emanuel-Correia, R. Microfinance: intervention in challenging contexts, 1 Eds., Singapore: Springer Nature Singapore, 13–35. https://doi.org/10.1007/978-981-97-5388-8_2 |

| [54] | Mermod AY (2013) Microfinance, In: Idowu, S.O., Capaldi, N., Zu, L., Gupta, A.D. (eds), Encyclopedia of Corporate Social Responsibility, Berlin: Springer, 1674–1682. https://doi.org/10.1007/978-3-642-28036-8_85 |

| [55] | Meyer J, Krauss A, Bachmann K (2019) Drivers of investor motivations for impact investments: The case of microfinance. Available at SSRN 3395275. |

| [56] |

Mia MA (2022) Social Purpose, Commercialisation, and Innovations in Microfinance. Singapore: Springer Nature Singapore. https://doi.org/10.1007/978-981-19-0217-8 doi: 10.1007/978-981-19-0217-8

|

| [57] |

Muñoz F, Vargas M, Vicente R (2014) Fund flow bias in market timing skill. Evidence of the clientele effect. Int Rev Econ Fin 33: 257–269. https://doi.org/10.1016/j.iref.2014.05.006 doi: 10.1016/j.iref.2014.05.006

|

| [58] |

Newey WK, West KD (1987) Hypothesis testing with efficient method of moments estimation. Int Econ Rev 28: 777-787. https://doi.org/10.2307/2526578 doi: 10.2307/2526578

|

| [59] |

Noor A (2020) The flow-performance relationship: evidence from Pakistani mutual funds. J Account Financ Emerg Econ 6: 145–154. https://doi.org/10.26710/jafee.v6i1.1050 doi: 10.26710/jafee.v6i1.1050

|

| [60] |

Ozdemir M, Savasan F, Ulev S (2023) Leveraging financial inclusion through Islamic microfinance: A new model proposal for participation banks in Turkiye. Borsa Istanbul Rev 23: 709–722. https://doi.org/10.1016/j.bir.2023.01.011 doi: 10.1016/j.bir.2023.01.011

|

| [61] | Parvin GA, Shaw R (2014) Microfinance: Role of NGOs in DRR, In: Shaw, R., Izumi, T. Civil Society Organization and Disaster Risk Reduction. Disaster Risk Reduction. Tokyo: Springer, 177–201 https://doi.org/10.1007/978-4-431-54877-5_10 |

| [62] |

Pérez-Gladish B, Benson K, Faff R (2012) Profiling socially responsible investors: Australian evidence. Aust J Manag 37: 189–209. https://doi.org/10.1177/0312896211429158 doi: 10.1177/0312896211429158

|

| [63] |

Petersen MA (2009) Estimating standard errors in finance panel data sets: Comparing approaches. Rev Financ Stud 22: 435–480. https://doi.org/10.1093/rfs/hhn053 doi: 10.1093/rfs/hhn053

|

| [64] | Porter ME, Kramer MR (2006) The link between competitive advantage and corporate social responsibility. Hav Bus Rev 84: 78–92. |

| [65] | Rao ZUR, Tauni MZ (2016) Asymmetric Flow-performance Relationship: Case of Chinese Equity Funds. Int J Econ Financ Issues 6: 492–496 |

| [66] |

Reboredo JC, Otero LA (2021) Are investors aware of climate-related transition risks? Evidence from mutual fund flows. Ecol Econ 189: 107148. https://doi.org/10.1016/j.ecolecon.2021.107148 doi: 10.1016/j.ecolecon.2021.107148

|

| [67] |

Reboredo JC, Otero González LA (2022) Low carbon transition risk in mutual fund portfolios: Managerial involvement and performance effects. Bus Strategy Environ 31: 950–968. https://doi.org/10.1002/bse.2928 doi: 10.1002/bse.2928

|

| [68] |

Renneboog L, Ter Horst J, Zhang C (2011) Is ethical money financially smart? Non-financial attributes and money flows of socially responsible investment funds. J Financ Intermediation 20: 562–588. https://doi.org/10.1016/j.jfi.2010.12.003 doi: 10.1016/j.jfi.2010.12.003

|

| [69] |

Ribeiro JPC, Duarte F, Gama APM (2022) Does microfinance foster the development of its clients? A bibliometric analysis and systematic literature review. Financ Innov 8: 1–35. https://doi.org/10.1186/s40854-022-00340-x doi: 10.1186/s40854-022-00340-x

|

| [70] |

Riedl A, Smeets P (2017) Why do investors hold socially responsible mutual funds?. J Financ 72: 2505-2550. https://doi.org/10.1111/jofi.12547 doi: 10.1111/jofi.12547

|

| [71] |

Sangwan S, Nayak NC, Sangwan V, et al. (2021) Covid‐19 pandemic: Challenges and ways forward for the Indian microfinance institutions. J Public Aff 21: e2667. https://doi.org/10.1002/pa.2667 doi: 10.1002/pa.2667

|

| [72] |

Simo C, Tchuigoua HT, Nzongang J (2023) Does corporate social responsibility pay? Evidence from social ratings in microfinance institutions. Technol Forecast Soc Change 187: 122180. https://doi.org/10.1016/j.techfore.2022.122180 doi: 10.1016/j.techfore.2022.122180

|

| [73] |

Sirri ER, Tufano P (1998) Costly search and mutual fund flows. J Financ 53: 1589–1622. https://doi.org/10.1111/0022-1082.00066 doi: 10.1111/0022-1082.00066

|

| [74] |

Tchuigoua HT, Soumaré I, Hessou HT (2020) Lending and business cycle: Evidence from microfinance institutions. J Bus Res 119: 1–12. https://doi.org/10.1016/j.jbusres.2020.07.022 doi: 10.1016/j.jbusres.2020.07.022

|

| [75] |

Ullah S, Akhtar P, Zaefarian G (2018) Dealing with endogeneity bias: The generalized method of moments (GMM) for panel data. Ind Mark Manag 71: 69–78. https://doi.org/10.1016/j.indmarman.2017.11.010 doi: 10.1016/j.indmarman.2017.11.010

|

| [76] | United Nations (2015) Transforming our world: The 2030 agenda for sustainable development. Resolution adopted by the general assembly on 25 September 2015. Available from: https://sustainabledevelopment.un.org/post2015/transformingourworld. |

| [77] |

Wagner C (2012) From Boom to Bust: How different has microfinance been from traditional banking? Dev Policy Rev 30: 187–210. https://doi.org/10.1111/j.1467-7679.2012.00571.x doi: 10.1111/j.1467-7679.2012.00571.x

|

| [78] |

Wagner C, Winkler A (2013) The vulnerability of microfinance to financial turmoil–evidence from the global financial crisis. World Dev 51: 71–90. https://doi.org/10.1016/j.worlddev.2013.05.008 doi: 10.1016/j.worlddev.2013.05.008

|

| [79] |

Wahid AN (1994) The Grameen Bank and Poverty alleviation in Bangladesh: Theory, Evidence and Limitations Theory, Evidence and Limitations. Am J Econ Sociol 53: 1–15. https://doi.org/10.1111/j.1536-7150.1994.tb02666.x doi: 10.1111/j.1536-7150.1994.tb02666.x

|

| [80] |

Xiao Y, Qiao H, Xie T (2019) Open-end funds for sustainable economic growth in China: the relationship between load fees, performance, and flows. Sustainability 11: 6514. https://doi.org/10.3390/su11226514 doi: 10.3390/su11226514

|

| [81] |

Zheng C, Zhang J (2021) The impact of COVID-19 on the efficiency of microfinance institutions. Int Rev Econ & Fin 71: 407–423. https://doi.org/10.1016/j.iref.2020.09.016 doi: 10.1016/j.iref.2020.09.016

|

Figures(1) / Tables(8)

Carmen-Pilar Martí-Ballester, Buket Erden. Fund performance—flow relationship for microfinance mutual funds[J]. Quantitative Finance and Economics, 2025, 9(3): 573-601. doi: 10.3934/QFE.2025020

DownLoad:

DownLoad: