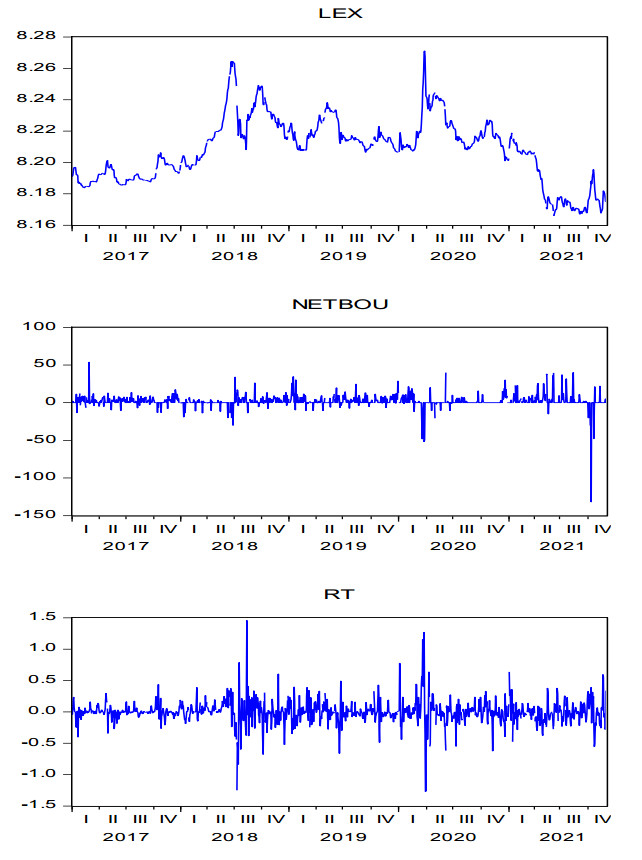

The COVID-19 crisis has not only manifested as a tragic public health crisis but also as an unprecedented economic disruption characterized by economic deterioration, the sharp increase in market volatility and the blinding uncertainty about the impact of the pandemic, especially in the context of developing countries. It is therefore not surprising that central banks seeking to maintain macroeconomic and financial stability, which are critical for sustained economic development, have maintained the practice of central bank intervention, especially in developing countries. This paper empirically examines the effect of central bank foreign exchange interventions on the level and volatility of the Uganda shilling / US dollar exchange rate (UGX/USD). Utilizing daily data spanning the period December 30, 2016, to 1 December 2021, we estimate a foreign exchange intervention model within a GARCH theoretical framework. Empirical results indicate that foreign exchange interventions have had mixed impact on the volatility of the exchange rate. In addition, despite generating significant uncertainty, the COVID 19 pandemic adverse shock results in a 0.03 percent appreciation due to Uganda's policy response to the COVID-19 pandemic.

Citation: Lorna Katusiime. 2023: COVID-19 and the effect of central bank intervention on exchange rate volatility in developing countries: The case of Uganda, National Accounting Review, 5(1): 23-37. doi: 10.3934/NAR.2023002

The COVID-19 crisis has not only manifested as a tragic public health crisis but also as an unprecedented economic disruption characterized by economic deterioration, the sharp increase in market volatility and the blinding uncertainty about the impact of the pandemic, especially in the context of developing countries. It is therefore not surprising that central banks seeking to maintain macroeconomic and financial stability, which are critical for sustained economic development, have maintained the practice of central bank intervention, especially in developing countries. This paper empirically examines the effect of central bank foreign exchange interventions on the level and volatility of the Uganda shilling / US dollar exchange rate (UGX/USD). Utilizing daily data spanning the period December 30, 2016, to 1 December 2021, we estimate a foreign exchange intervention model within a GARCH theoretical framework. Empirical results indicate that foreign exchange interventions have had mixed impact on the volatility of the exchange rate. In addition, despite generating significant uncertainty, the COVID 19 pandemic adverse shock results in a 0.03 percent appreciation due to Uganda's policy response to the COVID-19 pandemic.

| [1] |

Broto C (2013) The effectiveness of forex interventions in four Latin American countries. Emerg Mark Rev 17: 224–240. https://doi.org/http://dx.doi.org/10.1016/j.ememar.2013.03.003 doi: 10.1016/j.ememar.2013.03.003

|

| [2] |

Catalán-Herrera J (2016) Foreign exchange market interventions under inflation targeting: the case of Guatemala. J Int Financial Mark Inst Money 42: 101–114. https://doi.org/10.1016/j.intfin.2016.02.003 doi: 10.1016/j.intfin.2016.02.003

|

| [3] | Chamon M, Hofman D, Lanau S, et al. (2019) The effectiveness of intervention. Chapter 4: 43–61. |

| [4] |

Disyatat P, Galati G (2007) The effectiveness of foreign exchange intervention in emerging market countries: Evidence from the Czech koruna. J Int Money Financ 26: 383–402. https://doi.org/10.1016/j.jimonfin.2007.01.001 doi: 10.1016/j.jimonfin.2007.01.001

|

| [5] | Domaç I, Mendoza A (2004) Is there room for foreign exchange interventions under an inflation targeting framework? Evidence from Mexico and Turkey. https://doi.org/10.1596/1813-9450-3288 |

| [6] |

Dominguez KM (1998) Central bank intervention and exchange rate volatility. J Int Money Financ 17: 161–190. https://doi.org/10.1016/S0261-5606(97)98055-4 doi: 10.1016/S0261-5606(97)98055-4

|

| [7] | Edison HJ (1993) The effectiveness of central-bank intervention: a survey of the literature after 1982. In: International Finance Section, Department of Economics, Princeton University. |

| [8] |

Engle R (2001) GARCH 101: The use of ARCH/GARCH models in applied econometrics. J Econ Perspect 15: 157–168. https://doi.org/10.1257/jep.15.4.157 doi: 10.1257/jep.15.4.157

|

| [9] |

Fratzscher M, Gloede O, Menkhoff L, et al. (2019) When is foreign exchange intervention effective? Evidence from 33 countries. Am Econ J Macroecon 11: 132–156. https://doi.org/10.1257/mac.20150317 doi: 10.1257/mac.20150317

|

| [10] |

Ghosh AR, Ostry JD, Chamon M (2016) Two targets, two instruments: monetary and exchange rate policies in emerging market economies. J Int Money Financ 60: 172–196. https://doi.org/10.1016/j.jimonfin.2015.03.005 doi: 10.1016/j.jimonfin.2015.03.005

|

| [11] |

Goyal A, Arora S (2012) The Indian exchange rate and Central Bank action: An EGARCH analysis. J Asian Econ 23: 60–72. https://doi.org/http://dx.doi.org/10.1016/j.asieco.2011.09.001 doi: 10.1016/j.asieco.2011.09.001

|

| [12] | Guimarães RP, Karacadag C (2004) The empirics of foreign exchange intervention in emerging markets: the cases of Mexico and Turkey. IMF Working Papers No, 04/123. |

| [13] |

Katusiime L, Agbola FW (2018) Modelling the impact of central bank intervention on exchange rate volatility under inflation targeting. Appl Econ 50: 4373–4386. https://doi.org/10.1080/00036846.2018.1450482 doi: 10.1080/00036846.2018.1450482

|

| [14] |

Kearns J, Rigobon R (2005) Identifying the efficacy of central bank interventions: evidence from Australia and Japan. J Int Econ 66: 31–48. https://doi.org/http://dx.doi.org/10.1016/j.jinteco.2004.05.001 doi: 10.1016/j.jinteco.2004.05.001

|

| [15] |

Kim SJ, Kortian T, Sheen J (2000) Central bank intervention and exchange rate volatility—Australian evidence. J Int Financial Mark Inst Money 10: 381–405. https://doi.org/http://dx.doi.org/10.1016/S1042-4431(00)00027-5 doi: 10.1016/S1042-4431(00)00027-5

|

| [16] |

Menkhoff L, Sarno L, Schmeling M, et al. (2016) Information flows in foreign exchange markets: dissecting customer currency trades. J Financ 71: 601–634. https://doi.org/10.1111/jofi.12378 doi: 10.1111/jofi.12378

|

| [17] |

Menkhoff L (2013) Foreign exchange intervention in emerging markets: A survey of empirical studies. World Econ 36: 1187–1208. https://doi.org/10.1111/twec.12027 doi: 10.1111/twec.12027

|

| [18] | Mihaljek D (2005) Survey of central banks' views on effects of intervention. BIS Papers No 24. |

| [19] | Mohanty MS, Berger B (2013) Central bank views on foreign exchange intervention. BIS Papers No 73. |

| [20] |

Neely CJ (2008) Central bank authorities' beliefs about foreign exchange intervention. J Int Money Financ 27: 1–25. https://doi.org/http://dx.doi.org/10.1016/j.jimonfin.2007.04.012 doi: 10.1016/j.jimonfin.2007.04.012

|

| [21] | Nelson DB (1991) Conditional heteroskedasticity in asset returns: A new approach. Econometrica: Journal of the econometric society 59: 347–370. |

| [22] |

Pasquariello P (2007) Informative trading or just costly noise? An analysis of central bank interventions. J Financial Mark 10: 107–143. https://doi.org/10.1016/j.finmar.2006.11.001 doi: 10.1016/j.finmar.2006.11.001

|

| [23] |

Rime D, Sarno L, Sojli E (2010) Exchange rate forecasting, order flow and macroeconomic information. J Int Econ 80: 72–88. https://doi.org/10.1016/j.jinteco.2009.03.005 doi: 10.1016/j.jinteco.2009.03.005

|

| [24] | Sarno L, Taylor MP (2002) The Economics of Exchange Rates. Cambridge University Press. |

| [25] |

Seerattan D, Spagnolo N (2009) Central bank intervention and foreign exchange markets. Appl Financial Econ 19: 1417–1432. https://doi.org/10.1080/00036840902817789 doi: 10.1080/00036840902817789

|

| [26] |

Shah MKA, Hyder Z, Pervaiz MK (2009) Central bank intervention and exchange rate volatility in Pakistan: an analysis using GARCH-X model. Appl Financial Econ 19: 1497–1508. https://doi.org/10.1080/09603100902967553 doi: 10.1080/09603100902967553

|

| [27] | Takagi S (2014) The effectiveness of foreign exchange market intervention: a review of post-2001 studies on Japan. J Rev Global Econ 3: 84–100. |

| [28] |

Tuna G (2011) The effectiveness of Central Bank intervention: evidence from Turkey. Appl Econ 43: 1801–1815. https://doi.org/10.1080/00036840802676228 doi: 10.1080/00036840802676228

|

Figures(1) / Tables(5)

Lorna Katusiime. 2023: COVID-19 and the effect of central bank intervention on exchange rate volatility in developing countries: The case of Uganda, National Accounting Review, 5(1): 23-37. doi: 10.3934/NAR.2023002

DownLoad:

DownLoad: